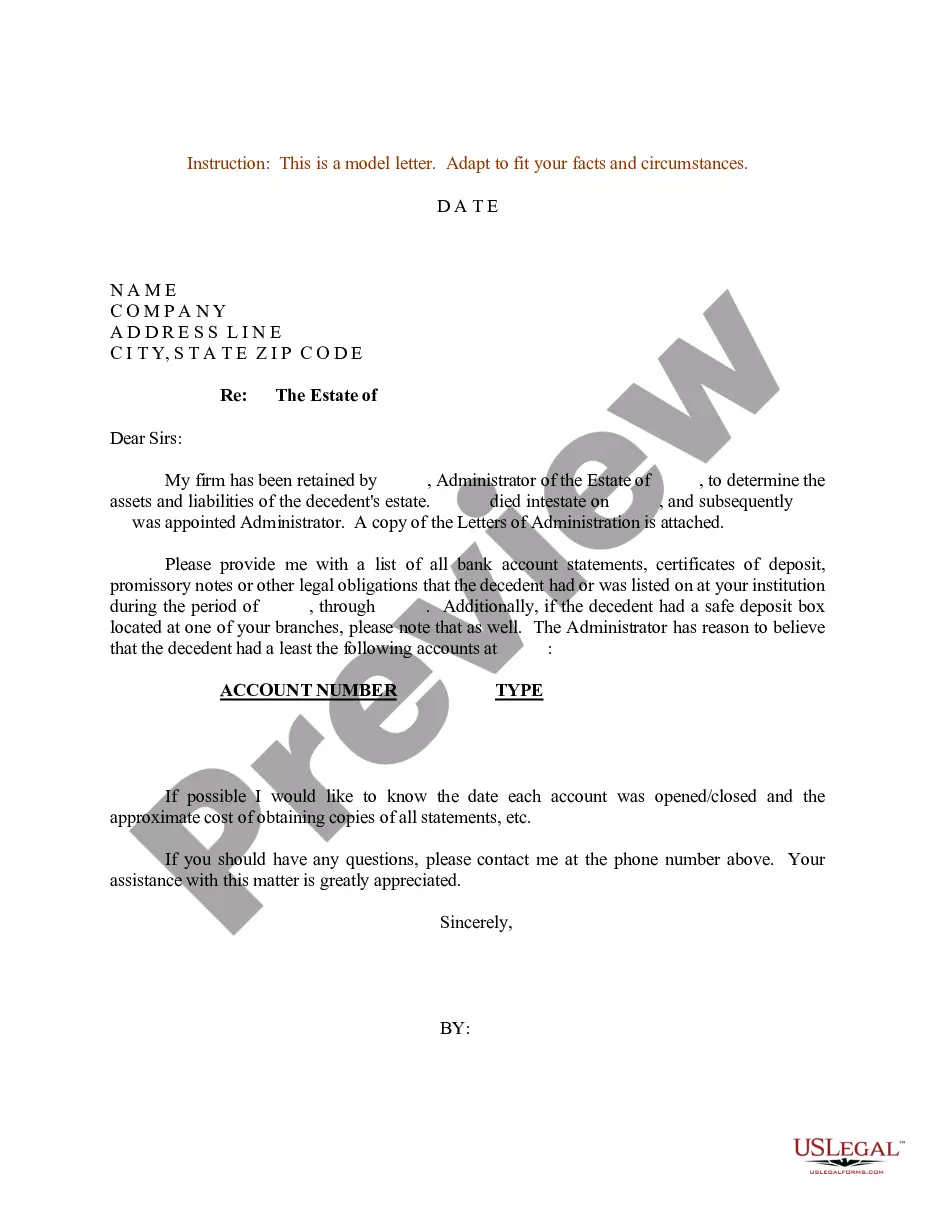

Decedent Account Bank Withdrawal In Wayne

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Bottom Line. Beneficiaries are named people who take ownership of a financial account after you die. If you die without naming a beneficiary, your bank account will transfer through your will and through probate law, as appropriate.

What Not to Do When Someone Dies: 10 Common Mistakes Not Obtaining Multiple Copies of the Death Certificate. 2- Delaying Notification of Death. 3- Not Knowing About a Preplan for Funeral Expenses. 4- Not Understanding the Crucial Role a Funeral Director Plays. 5- Letting Others Pressure You Into Bad Decisions.

After someone dies, a sole-owned bank account may go to a named beneficiary or be handled by the executor of the estate. Joint accounts typically have automatic rights of survivorship, but it's still important to check with your bank to ensure smooth access to funds.

A deceased person's bank account is inaccessible unless you're a joint owner, a beneficiary of the account or the estate executor.

If you are named as the successor trustee (the person who assumes control of the trust after the initial trustee dies), you should notify the bank that the initial trustee has died. You will also need to provide a certified copy of the death certificate.

The bank is likely to ask for two forms of your identification (usually a passport or driver's licence, or a proof of address with a utility bill) and a copy of the will. If there's no will, the bank could ask for evidence of your relationship to the deceased. You'll also need the death certificate.

Banks generally cannot close a deceased account until after the person's estate has gone through probate or has otherwise settled. Joint accounts that are held together with a surviving owner are not considered deceased accounts. Ownership of these accounts reverts to the surviving owner.

The Federal Deposit Insurance Corp. continues to insure accounts for six months after an account holder dies, allowing the surviving account holder to redistribute funds to other accounts to keep them insured. Once the period elapses, FDIC coverage stops.