Termination With Severance In Montgomery

Description

Form popularity

FAQ

Lump sum severance package cons Lump sum payments may push you into a higher tax bracket for that year. You need to manage your finances more carefully to ensure the lump sum lasts until you secure another source of income. Finally, you forfeit any negotiation power for future benefits or assistance.

If you did not earn enough wages, you will not be eligible for benefits. The decision regarding whether you earned enough wages during your base period is call a monetary determination.

Severance payments are deductible from UI benefits (based on the number of weeks of your regular wage the payments cover). Once your severance payments are exhausted, you may receive UI benefits, if you are eligible.

What is the downside to severance? The downside to severance includes financial drawbacks such as loss of steady income, potential loss of benefits, and uncertainty about future job prospects, as well as the impact on retirement savings and benefits.

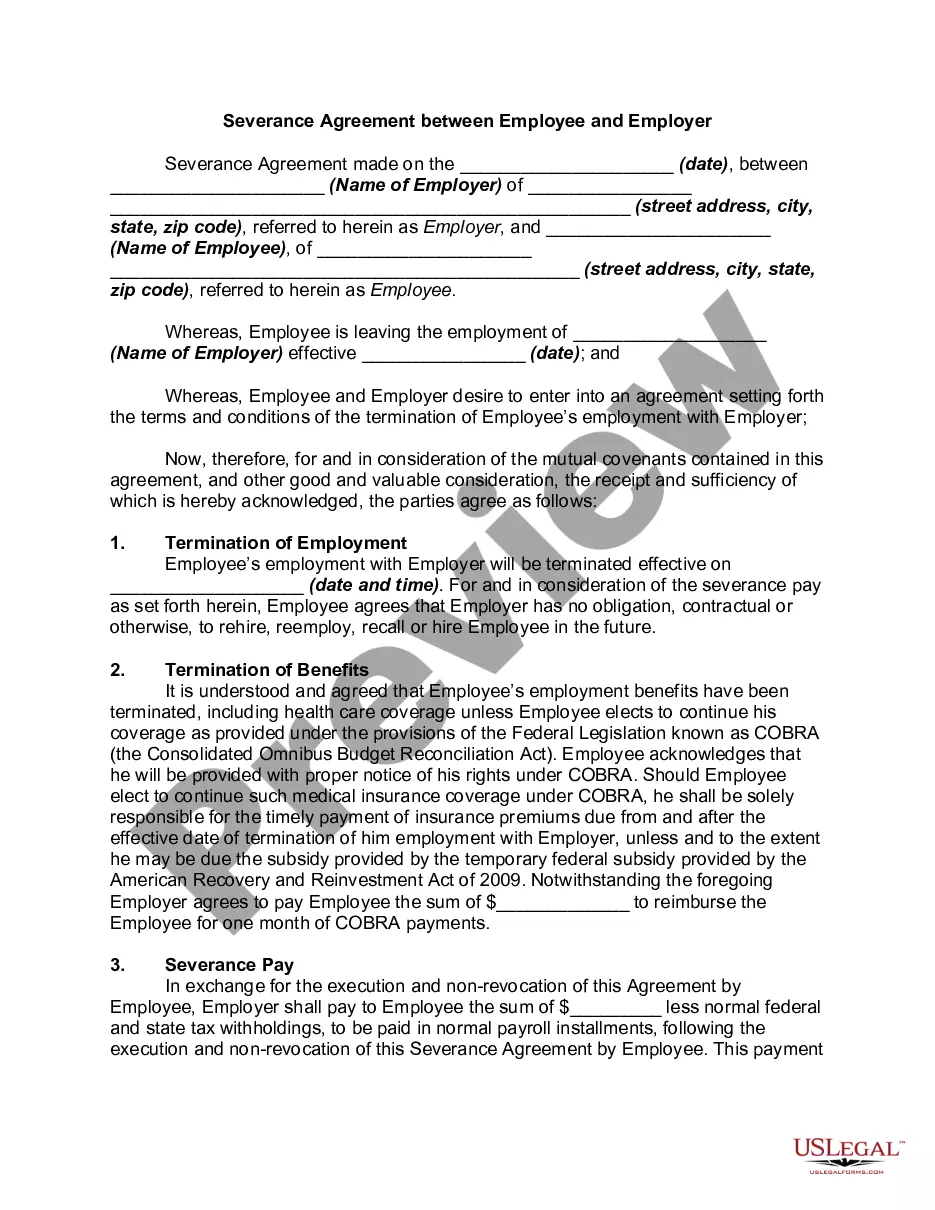

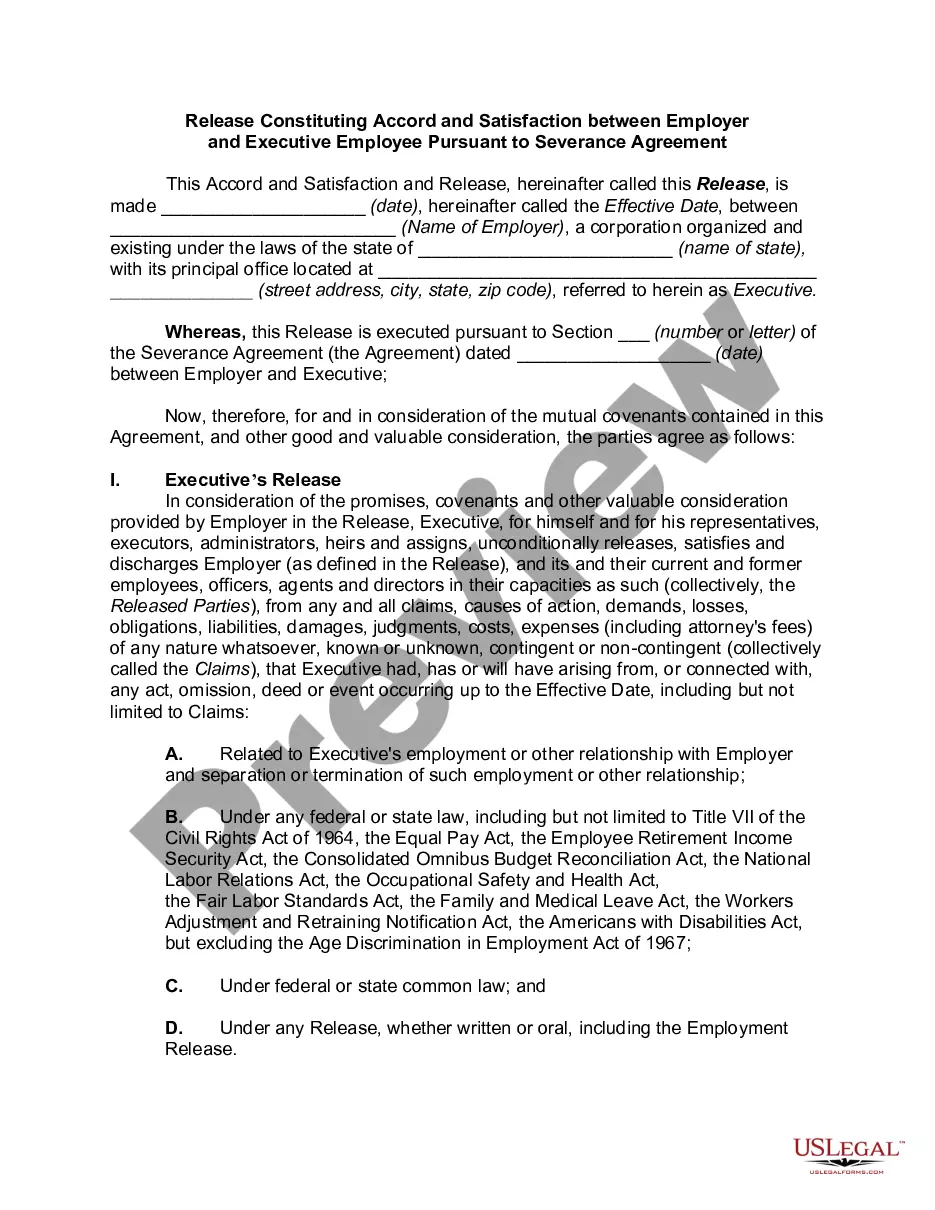

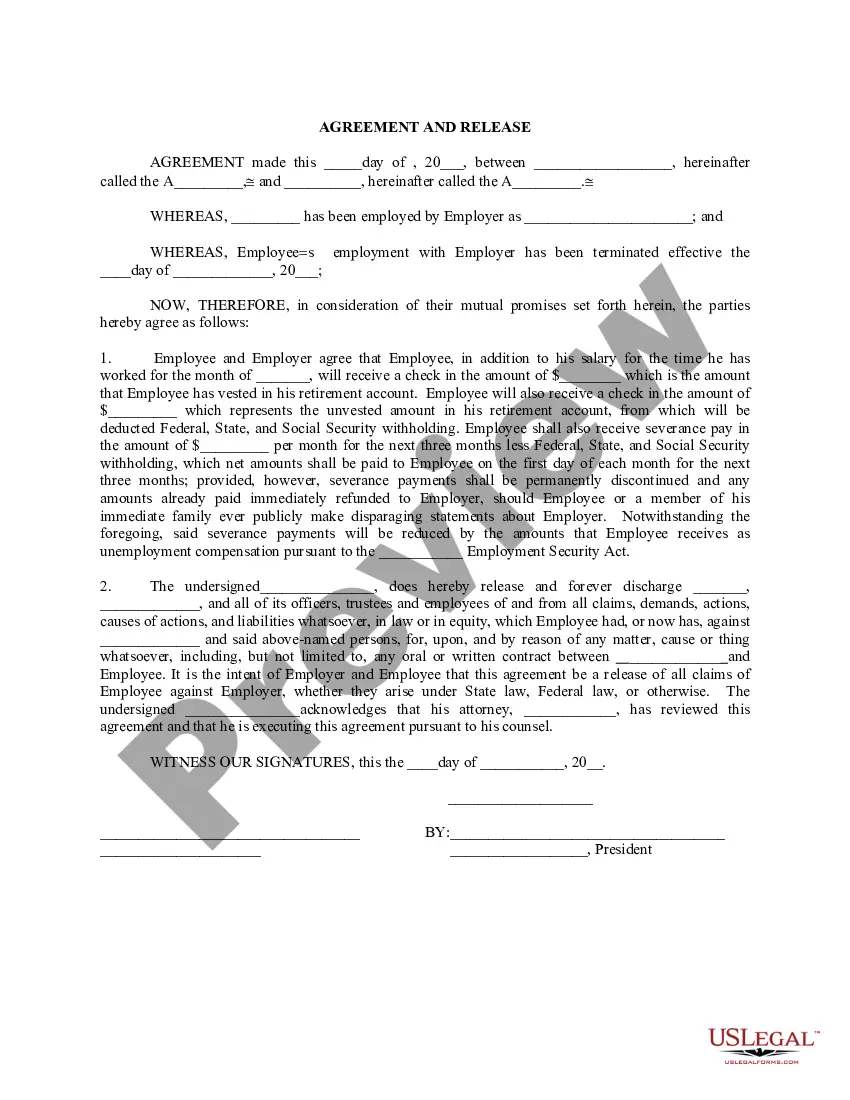

Basically, a severance agreement is a waiver or release of liability that the outgoing employee signs, protecting the business from lawsuits. These agreements are usually part of a larger severance package that includes compensation, outplacement services, and other benefits in exchange for the employee's signature.

Extension of Benefits Under Rule of 70 To be eligible to retire, you must be at least age 55 with 10 years of service or age 65. Years of service for the “Rule of 70” eligibility purposes, means total years of employment from date of hire to date of termination.

Eligibility for Retiree Health and Life Insurance Benefits Rule of 70: the employee's age plus years of continuous, full-time service equal 70 or more, and the employee is at least age 55, with at least ten years of continuous, full-time service.