Letter For Recovery Debt In Miami-Dade

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

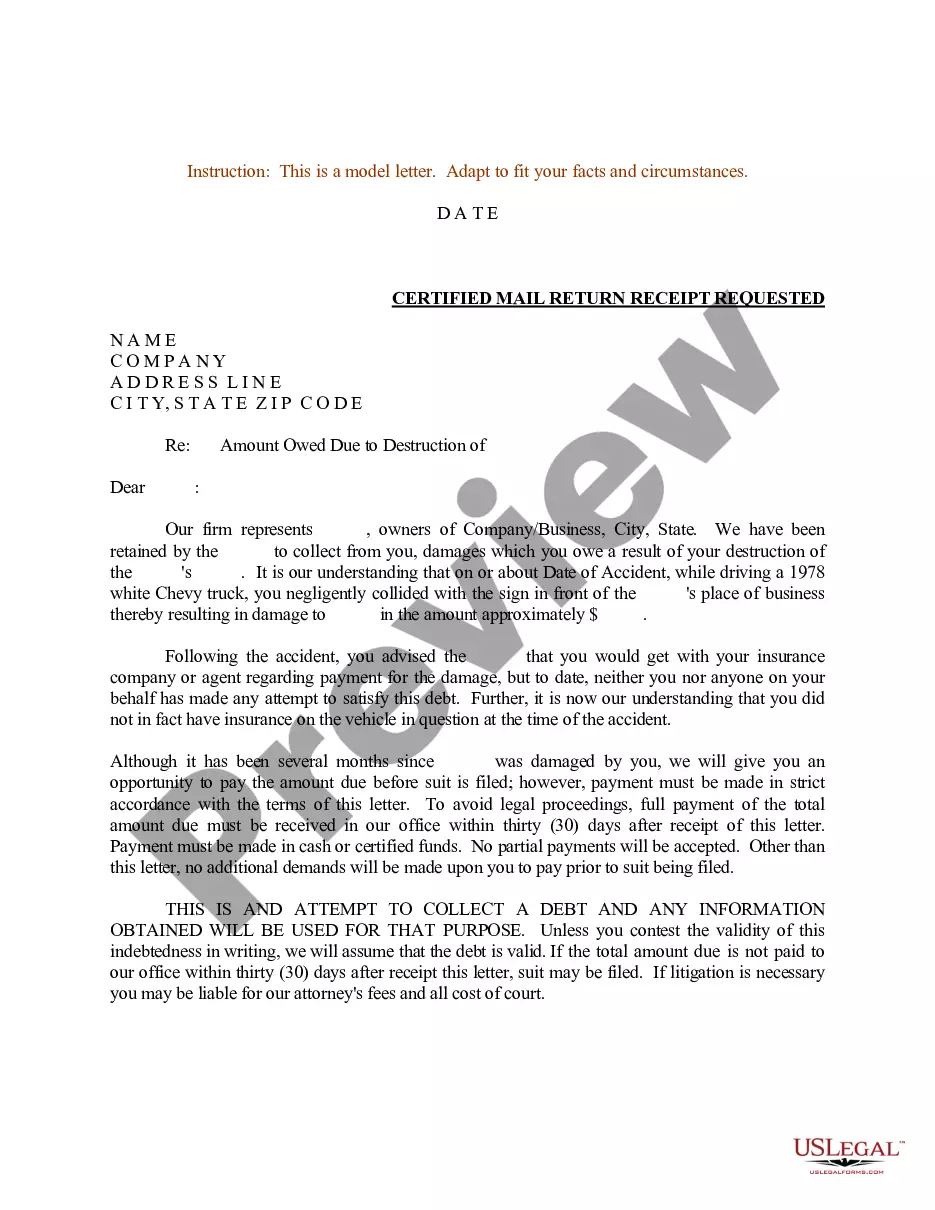

Use certified mail. If you are sending a debt collection letter for the purpose of informing debtors that legal action will soon be taken, you must be able to prove they received your communication. That means sending it by certified mail.

Here's a step-by-step guide that outlines the actions a business should take before moving forward with a collection agency. Contact the Debtor. Send a Demand Letter. Consider Negotiation. Hire a Collection Agency. Provide Documentation. Monitor Progress. Consider Legal Action.

Use certified mail. If you are sending a debt collection letter for the purpose of informing debtors that legal action will soon be taken, you must be able to prove they received your communication. That means sending it by certified mail.

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

The 11-word phrase often cited to stop debt collectors is: ``I do not acknowledge this debt and request verification of it.'' This phrase requests that the debt collector provide verification of the debt, which they are legally obligated to do under the Fair Debt Collection Practices Act (FDCPA) in the United States.

If you do not respond, you will lose certain rights, but it is not a legal admission, usable in court, that you owe the debt. If there is no response, or if the letter goes back to the collection agency undelivered or marked moved, deceased, in jail, etc., the collection agency can still due you.

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.