Judgment Paid Within 30 Days In Montgomery

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Here are four ways to avoid paying a judgment: 1) Use asset protection tools such as an asset protection trust, 2) use legal exemptions, 3) negotiate with the creditor, 4) file for bankruptcy.

You may be able to undo, or set aside, this judgment if you didn't know about it or in a few other situations. You will not go to jail for having a judgment against you.

Statute of Limitations in Maryland The statute of limitations allows a creditor three years to collect on debts.

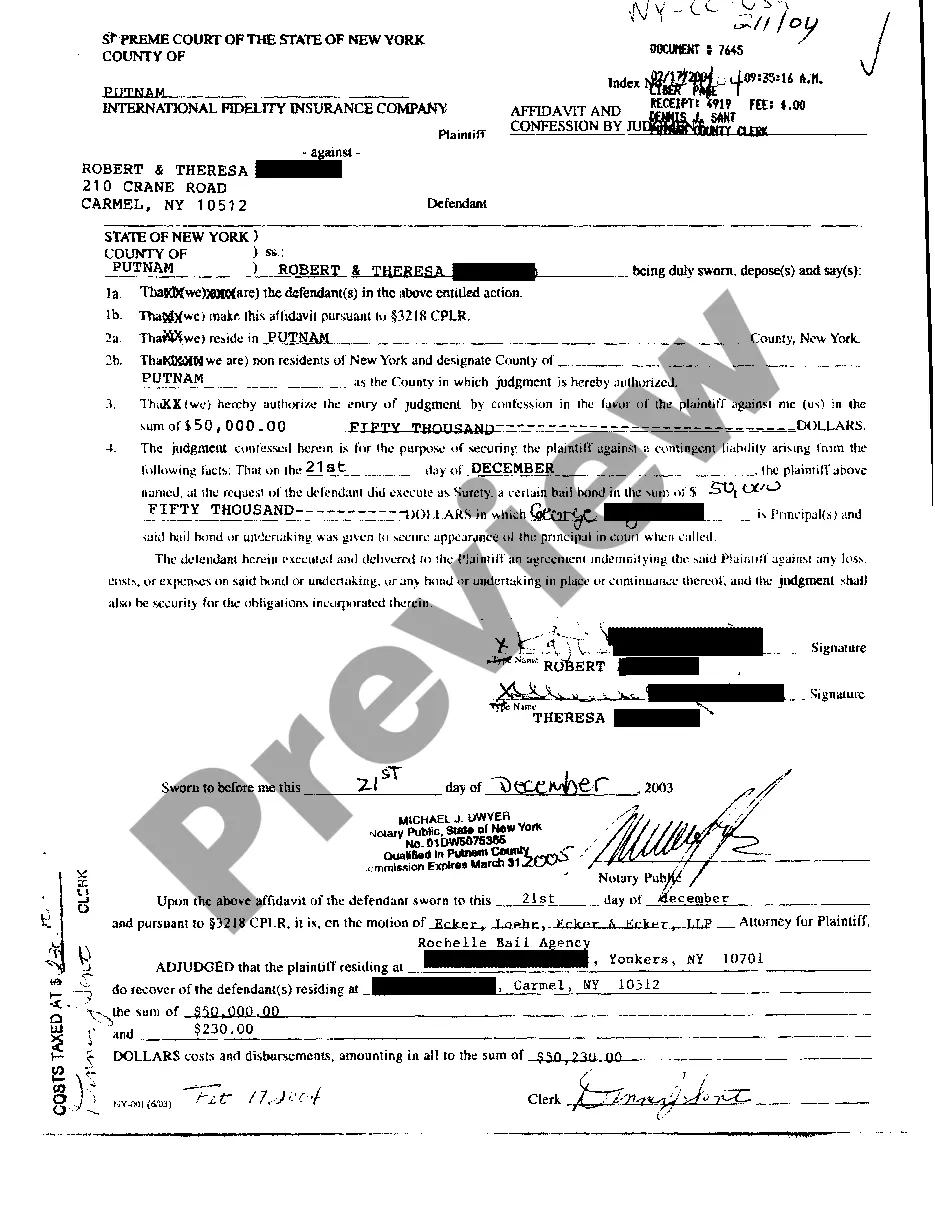

A creditor who obtains a judgment against you is the "judgment creditor." You are the "judgment debtor" in the case. A judgment lasts for 12 years and the plaintiff can renew the judgment for another 12 years.

Under Maryland's Consumer Debt Collection Act debt collectors may not... Use or threaten force or violence. Threaten criminal prosecution unless a violation of criminal law is involved. Disclose, or threaten to disclose, information affecting your reputation for creditworthiness if they know the information is false.

(a) Except as provided in § 11-106 of this subtitle, the legal rate of interest on a judgment shall be at the rate of 10 percent per annum on the amount of judgment.

A creditor who obtains a judgment against you is the "judgment creditor." You are the "judgment debtor" in the case. A judgment lasts for 12 years and the plaintiff can renew the judgment for another 12 years.

Once the waiting period passes, there are three different ways you can collect on the judgment: Garnishing the other person's wages; Garnishing the other person's bank account; or. Seizing the other person's personal property or real estate.

In Alabama, a creditor can place a judgment lien on your real property (or your personal property or vehicle) in order to collect the judgment, and it will remain attached to your real property for 10 years, even if you sell the property.

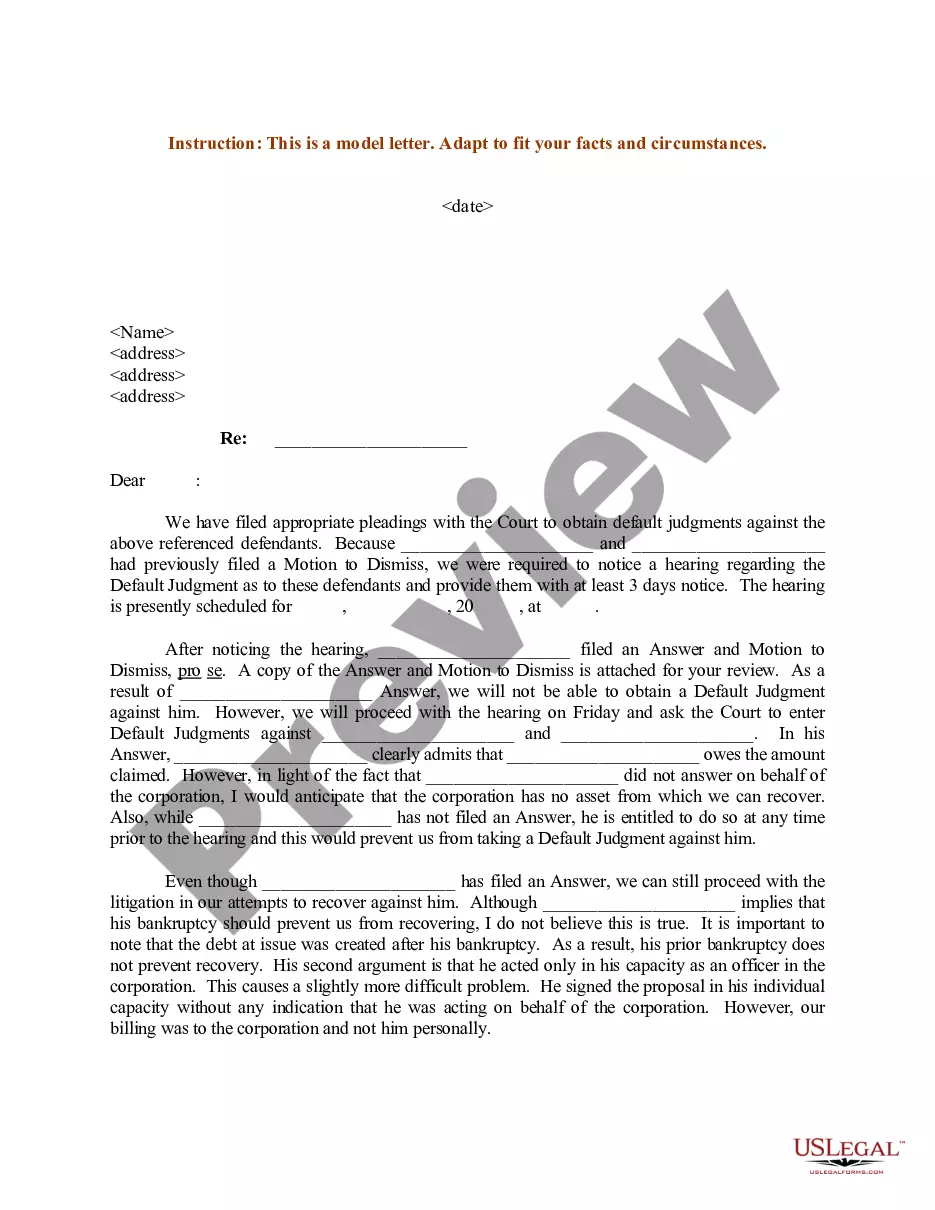

If the defendant responds to the lawsuit, then it can take months or even years, to finally get to a judgment – depending on how hard the defendant fights. If the defendant does not answer the lawsuit and we secure a default judgment, we must wait an additional 30 days before taking further actions.