Meeting Annual Consider For S Corp In Wake

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

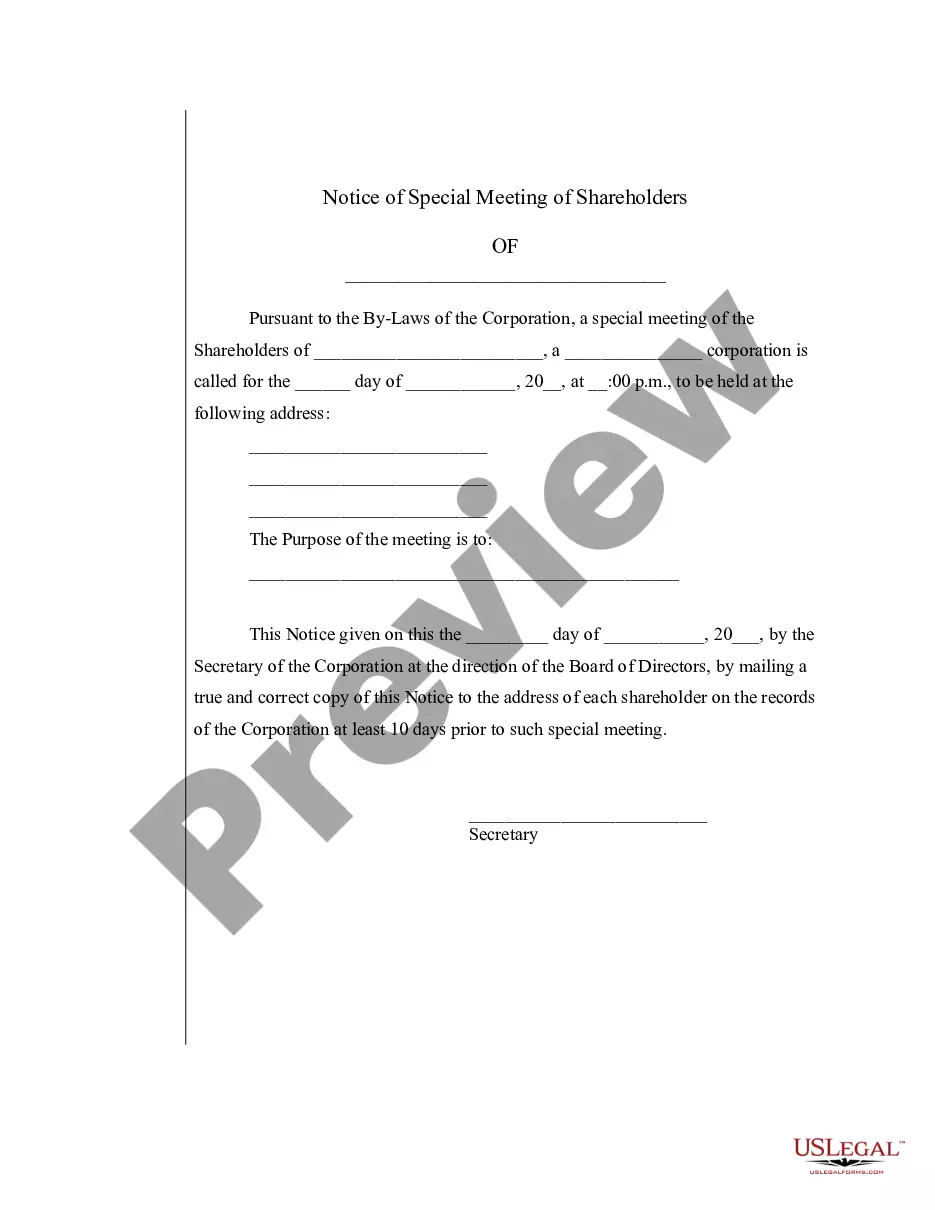

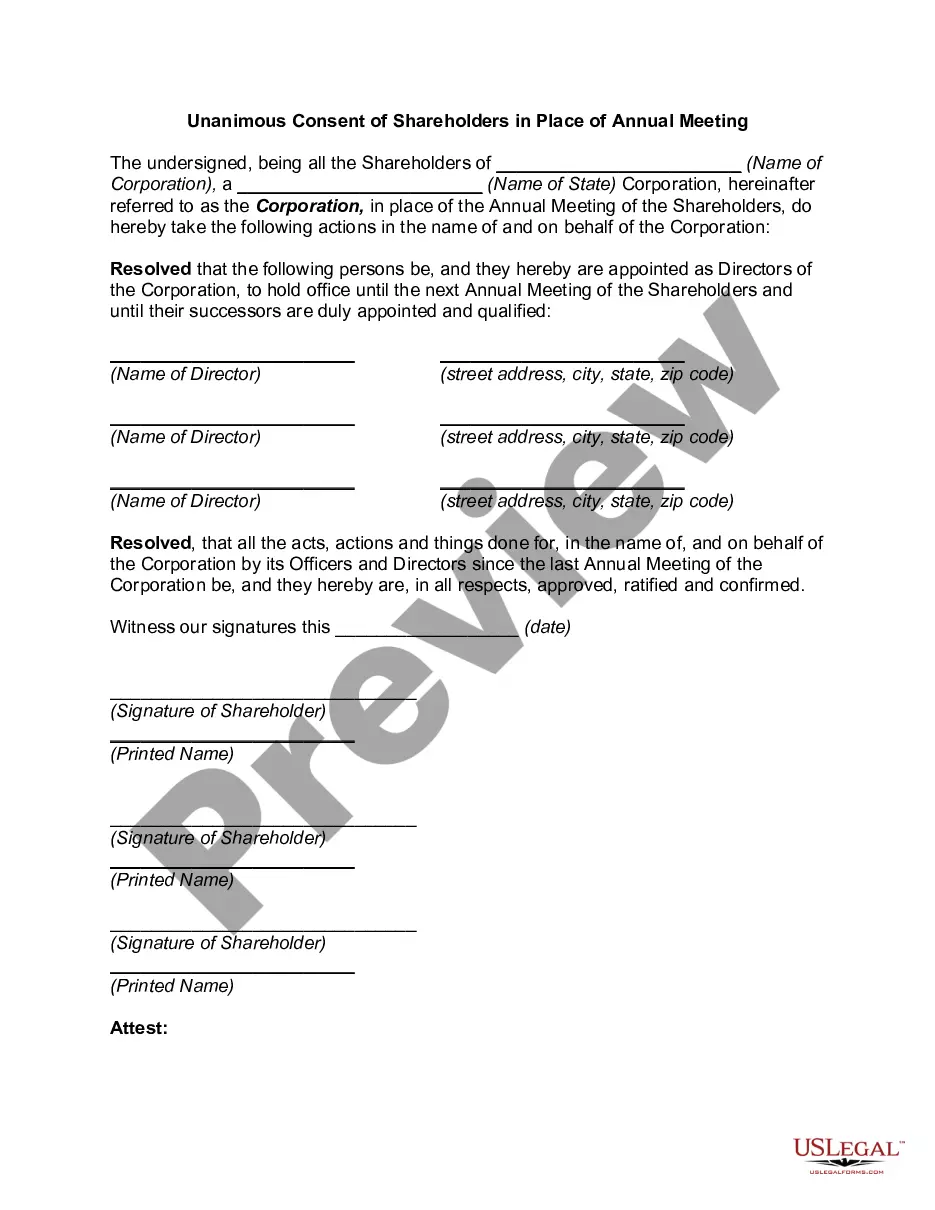

Here is Your 'To-Do-List' of 7 things to be Aware of if You Want to PROPERLY Maintain Your S-Corporation: Corporate Documents. Annual Minutes and Board Meetings. Annual State Secretary of State Filings. Regular Operations and 'Using the Name' ... Quarterly Payroll. Tax Return Filing. State Tax Filing Requirements.

An S-corp annual report details an S-corporation's activities during the previous year. S-corporations and other companies must file an annual report each year on the state level, typically through the Secretary of State's office in their state.

Both California Corporations and California S-Corps are required to hold an annual meeting for shareholders. These meetings are pivotal for fostering transparency, discussing business strategy, and making essential corporate decisions.

California law requires that corporations update their records with the Secretary of State's office. Every year, your California Corporation must file an Annual Statement of Information which discloses the corporation's addresses, officers, directors and registered agent.

Instead, the company's owners report that income (or loss) on their own personal income tax returns. You do, however, still have to file a tax return: Form 1120-S, the income tax return for S corporations, and which is due on March 15, 2025 if you're a calendar year corporation.

S Corps that lose their “S” status must typically wait five years before being able to re-elect it. As mentioned, deliberately violating one of the rules, such as transferring stock to an ineligible shareholder, is not a good thing.

The Corporate Transparency Act requires certain newly formed or registered entities to report specific information about their beneficial owners to the U.S. Department of the Treasury's Financial Crimes Enforcement Network (FinCEN). This act aims to prevent misuse of corporations and LLCs for illicit activities.

Built-in gains (BIG) tax can apply when a C corp elects to become an S corp, and for a five-year period following the conversion, starting on the first day of the first tax year after making the S corp election.