Annual Meeting Shareholders With Ird In New York

Description

Form popularity

FAQ

This decision expressly invalidates the FTB's guidance on the application of P.L. 86-272 to certain transactions conducted over the internet. California was the first state to publicly react to the MTC's new statement on P.L. 86-272 when it released the TAM in February 2022.

Public Law 86-272 prevents California from assessing income taxes on out-of-state businesses whose operations within the state are limited to “protected activities” (selling tangible personal property and soliciting sales) and who have no physical presence in the state.

New York receipts ofFixed dollar minimum tax equals: Not more than $100,000 $19 More than $100,000 but not over $250,000 $38 More than $250,000 but not over $500,000 $131 More than $500,000 but not over $1,000,000 $2253 more rows •

The apportionment factor is a fraction, determined by including only those receipts, net income, net gains, and other items described in this section that are included in the computation of the taxpayer's business income (determined without regard to the modification provided in subparagraph nineteen of paragraph (a) ...

P.L. 86-272 is a 1962 federal law that protects corporations involved in interstate commerce from taxation in a state where their only activities are the solicitation of sales for tangible personal property, provided that orders are sent outside the state for approval and fulfilment.

Public Law 86-272 potentially applies to companies located outside of California whose only in-state activity is the solicitation of sale of tangible personal property to California customers. Businesses that qualify for the protections of Public Law 86-272 are exempt from state taxes that are based on your net income.

The New York State CT-3-A is a combined franchise tax return for general business corporations. This form must be used for tax periods beginning on or after January 1, 2023. It's essential for compliance with New York tax laws.

If one of you was a New York State resident and the other was a nonresident or part-year resident, you must each file a separate New York return. The resident must use Form IT-201. The nonresident or part-year resident, if required to file a New York State return, must use Form IT-203.

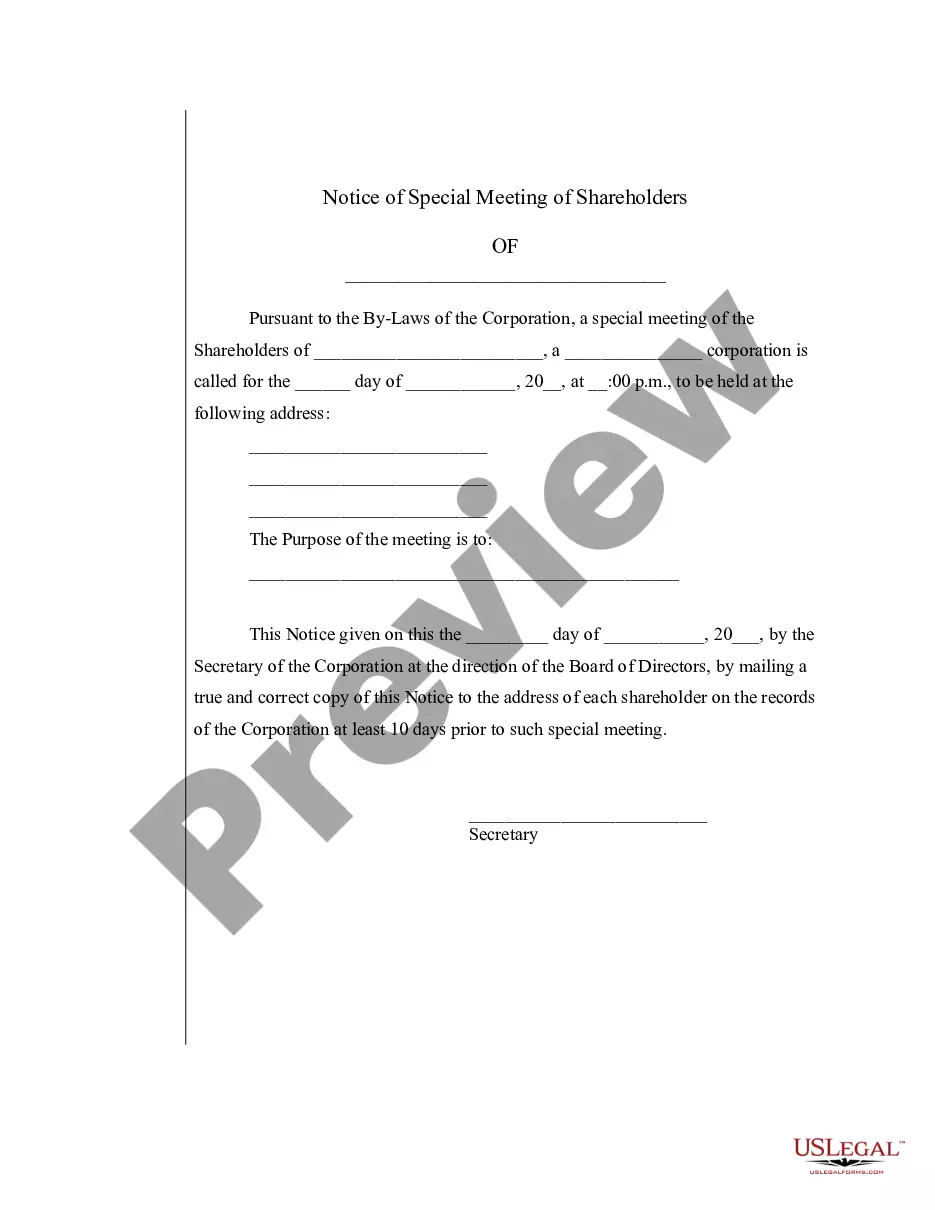

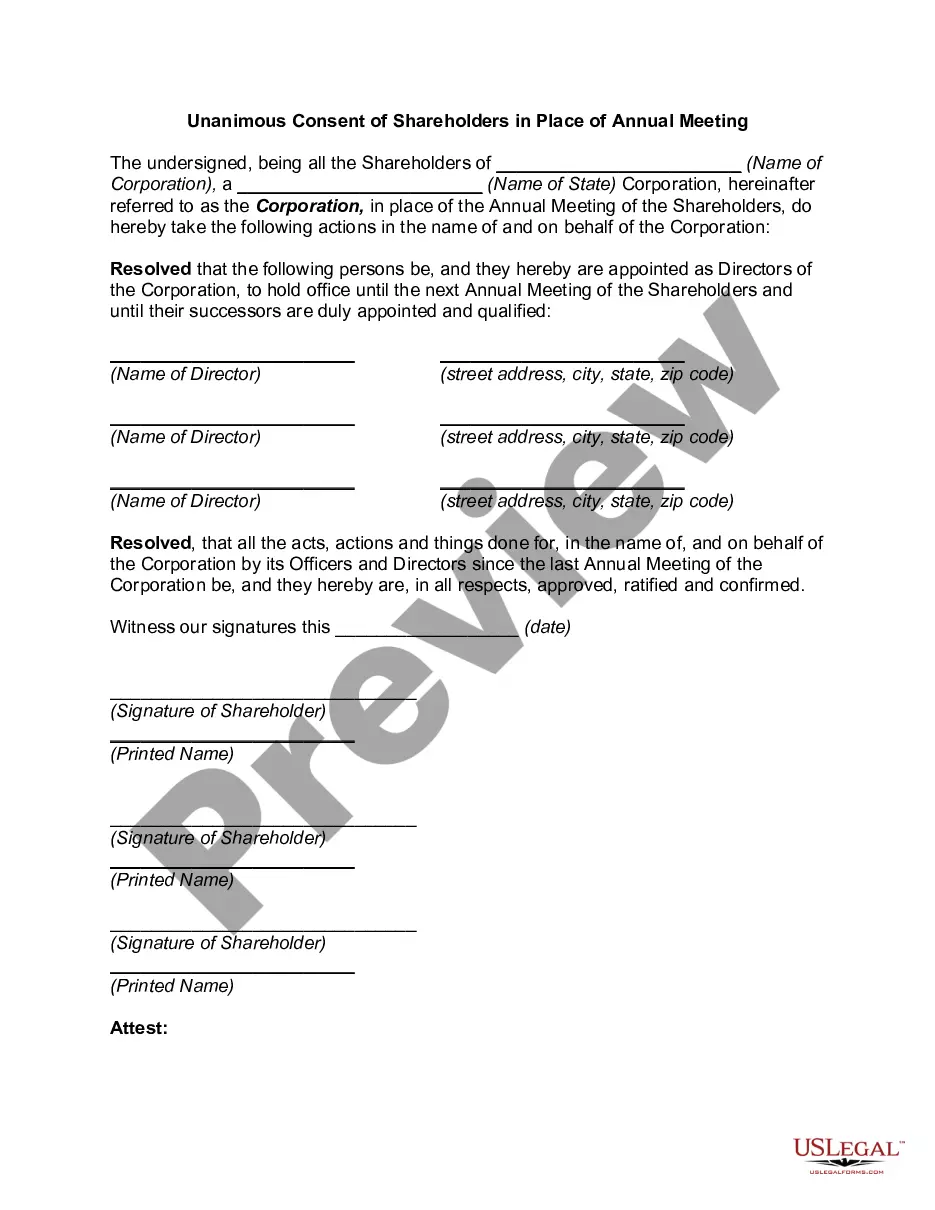

All shareholders must be notified of the format, date, time, and place of the meeting. How far in advance notices should be distributed may depend on your state, but generally, they should be sent out more than 10 days prior to the meeting, but less than 60 days.

Annual General Meeting (AGM) During these meetings, corporate board members present annual financial reports and accounts to be ratified by shareholders. Shareholders can also question board decisions and vote on the appointment, election, or removal of company directors.