Annual Meeting Shareholders With Ird In Minnesota

Description

Form popularity

FAQ

When should I hold a shareholder meeting? An annual shareholder meeting is typically scheduled just after the end of the fiscal year. This allows for the previous year's financial performance to be fully assessed and discussed.

At an annual general meeting (AGM), directors of the company present the company's financial performance and shareholders vote on the issues at hand. Shareholders who do not attend the meeting in person may usually vote by proxy, which can be done online or by mail.

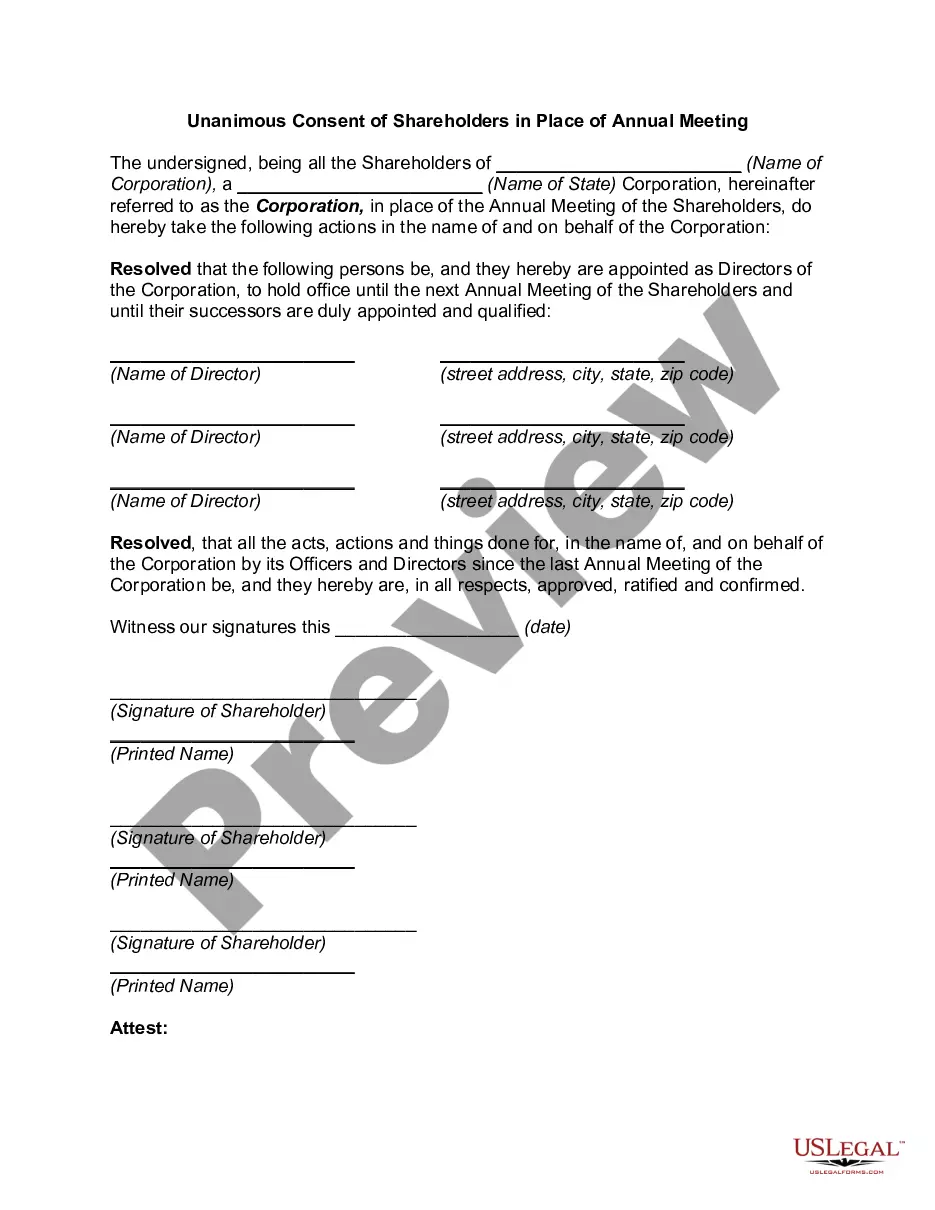

Scheduled meetings – Your business should hold at least one annual shareholders' meeting. You can have more than one per year, but one per year is often the required minimum. An annual board of directors meeting is often also held in conjunction with the shareholders' meeting as well.

But to keep the liability shield in place, corporations must follow certain formalities—such as holding and documenting an annual meeting. Failure to hold annual meetings could allow creditors to “pierce the corporate veil” to pursue shareholders' personal assets to satisfy the business's debts.

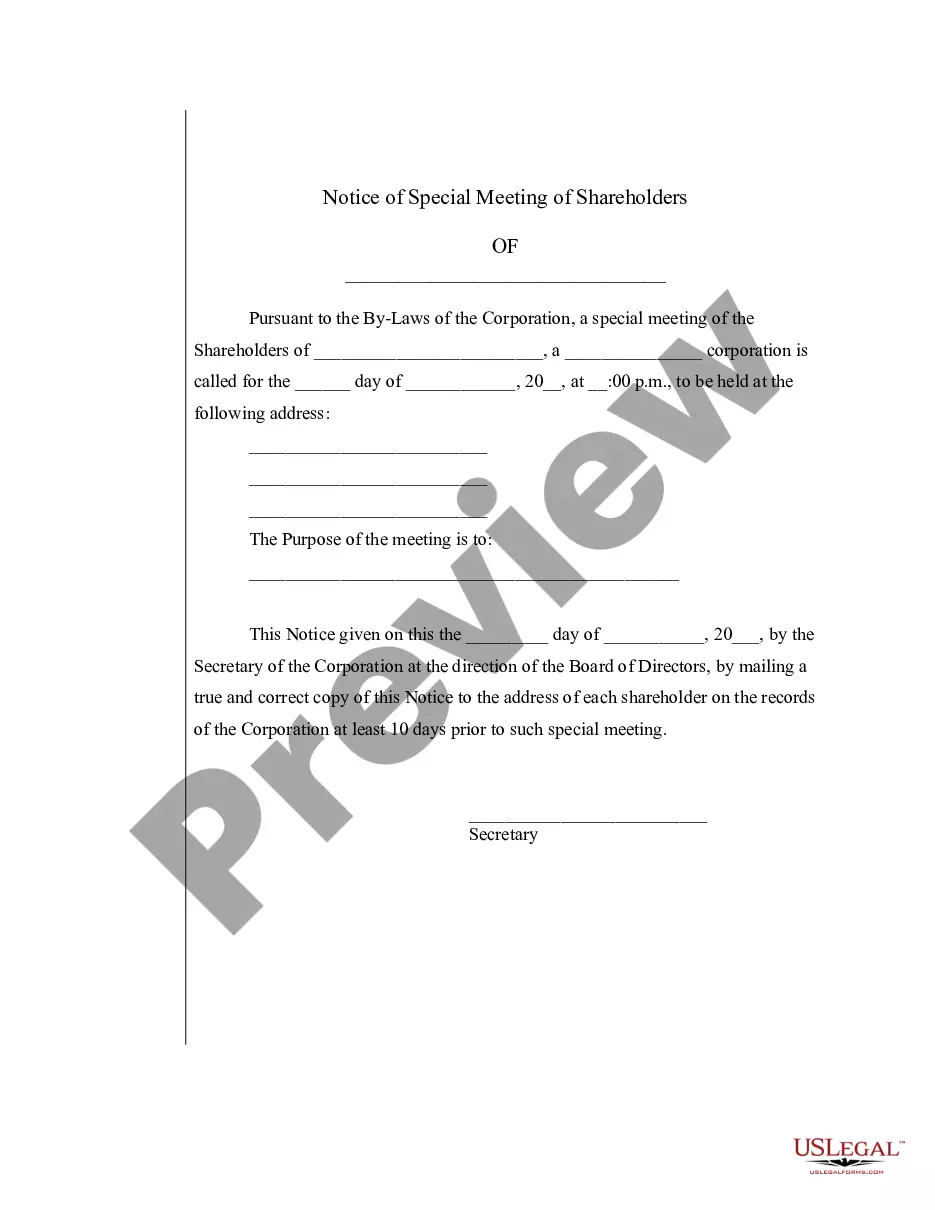

Section 601 - Notice of shareholders' meeting or report (a) Whenever shareholders are required or permitted to take any action at a meeting a written notice of the meeting shall be given not less than 10 (or, if sent by third-class mail, 30) nor more than 60 days before the date of the meeting to each shareholder ...

If your business is set up and registered as a Corporation, you're required by law to hold an annual shareholder meeting and to document the meeting with minutes.

A company other than OPC must conduct at least one Annual General Meeting (AGM) in a financial year. The first AGM of the company, i.e. a newly incorporated company, should be held within nine months from the closing of the first financial year.

Yes, it is possible to establish an S-corp as a one-person business. While traditionally S corporations are formed with multiple shareholders, the IRS allows a single individual to set up an S corporation. As an individual, you can be the sole shareholder, director, and employee of the S-corp.

Yes, one person can form an S corporation and serve as its sole board member and employee. Note, however, that you'll still need to hold annual board of directors meetings and take minutes at those meetings, even if you're the only attendee.

Corporations doing business in Minnesota that have elected to be taxed as S corporations under IRC section 1362 must file Form M8. The entire share of an entity's income is taxed to the shareholder, whether or not it is actually distributed. Each shareholder must include their share of income on their tax return.