Personal Property With Replacement Cost In Clark

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

200% rule: This rule says that the taxpayer can identify any number of replacement properties, as long as the total fair market value of what they identify is not greater than 200% of the fair market value of what was sold as relinquished property.

After filing the original affidavit, the County Assessor will mail you an Exemption Renewal Post Card each year. To continue your exemption, simply sign and return this post card to the Assessor's Office.

Property taxes are calculated by multiplying your municipality's effective tax rate by the most recent assessment of your property's value. Understanding Your Tax Bill. Ask for Your Property Tax Card. Don't Build. Limit Curb Appeal. Research Neighboring Homes. Allow the Assessor Access to Your Home.

Overall limit. As an individual, your deduction for state and local taxes (SALT) (lines 5a, 5b and 5c on Schedule A of Form 1040) is limited to a combined total deduction of $10,000 ($5,000 if married filing separately). You may be subject to a limit on some of your other itemized deductions also.

You can claim an exemption from LPT as part of your LPT Return. If you have already submitted an LPT Return and did not claim an exemption that you were entitled to, you should contact the LPT branch.

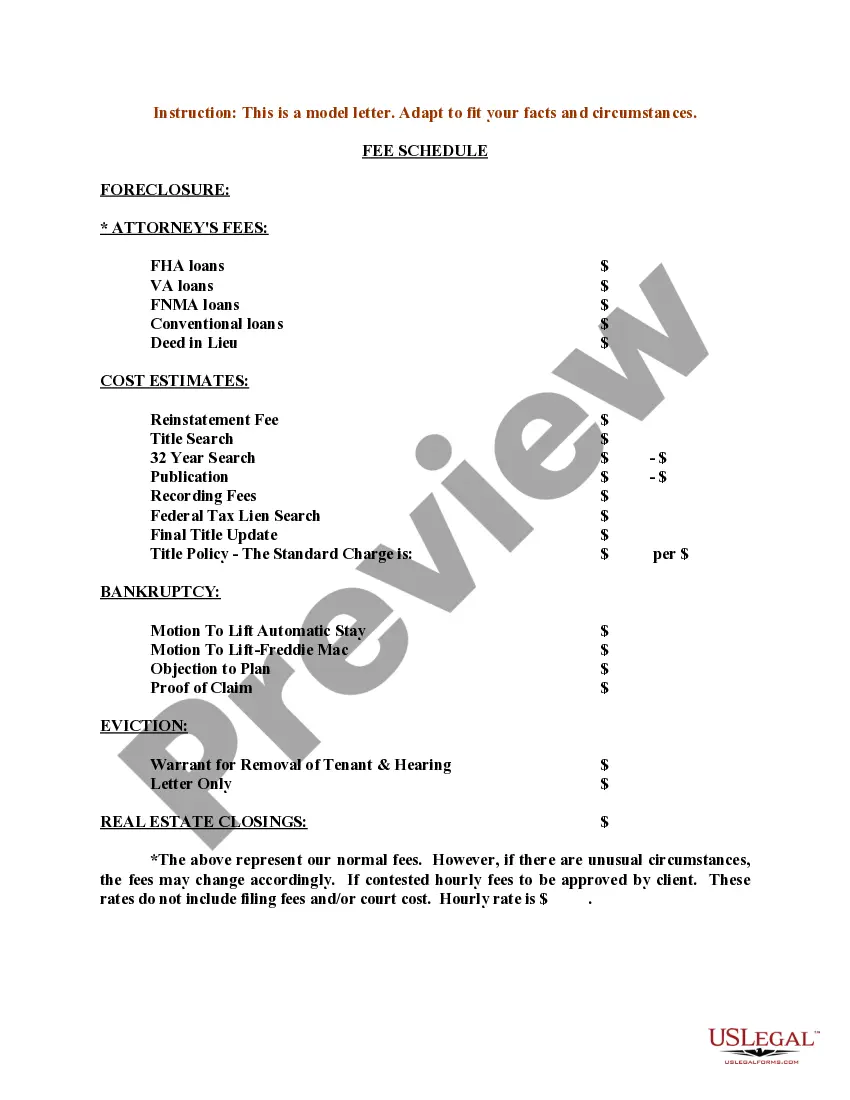

The personal property declaration is a list of all personal property owned, rented, leased, or controlled, as of July 1st. The declaration must be filed annually no later than July 31st. If the notice was mailed after July 15th , the owner has 15 days to file the declaration.

Motor vehicles required to be registered with the Nevada Department of Motor Vehicles and Public Safety are exempt from the property tax, though subject to a governmental service tax.

Ing to Nevada Revised Statutes, all property that is not defined or taxed as "real estate" or "real property" is considered to be "personal property." Taxable personal property includes manufactured homes, aircraft, and all property used in conjunction with a business.