Form Assignment Accounts Receivable With Credit Card In Arizona

Description

Form popularity

FAQ

If the assignment of the contract is done with the consent of the counterparty, that amounts to a novation – that is, partial re-writing of the terms of the original contract. benefit under a contract, then such receivables/benefit are not assignable, or not assignable without the consent of the counterparty.

Credit Cards as Liabilities The balance owed on a credit card can be treated either as a negative asset, known as a “contra” asset, or as a liability. In this article we'll explore the optional method of using liability accounts, however, there are several advantages to using the Contra Asset Approach.

Therefore, when a journal entry is made for an accounts receivable transaction, the value of the sale will be recorded as a credit to sales. The amount that is receivable will be recorded as a debit to the assets. These entries balance each other out.

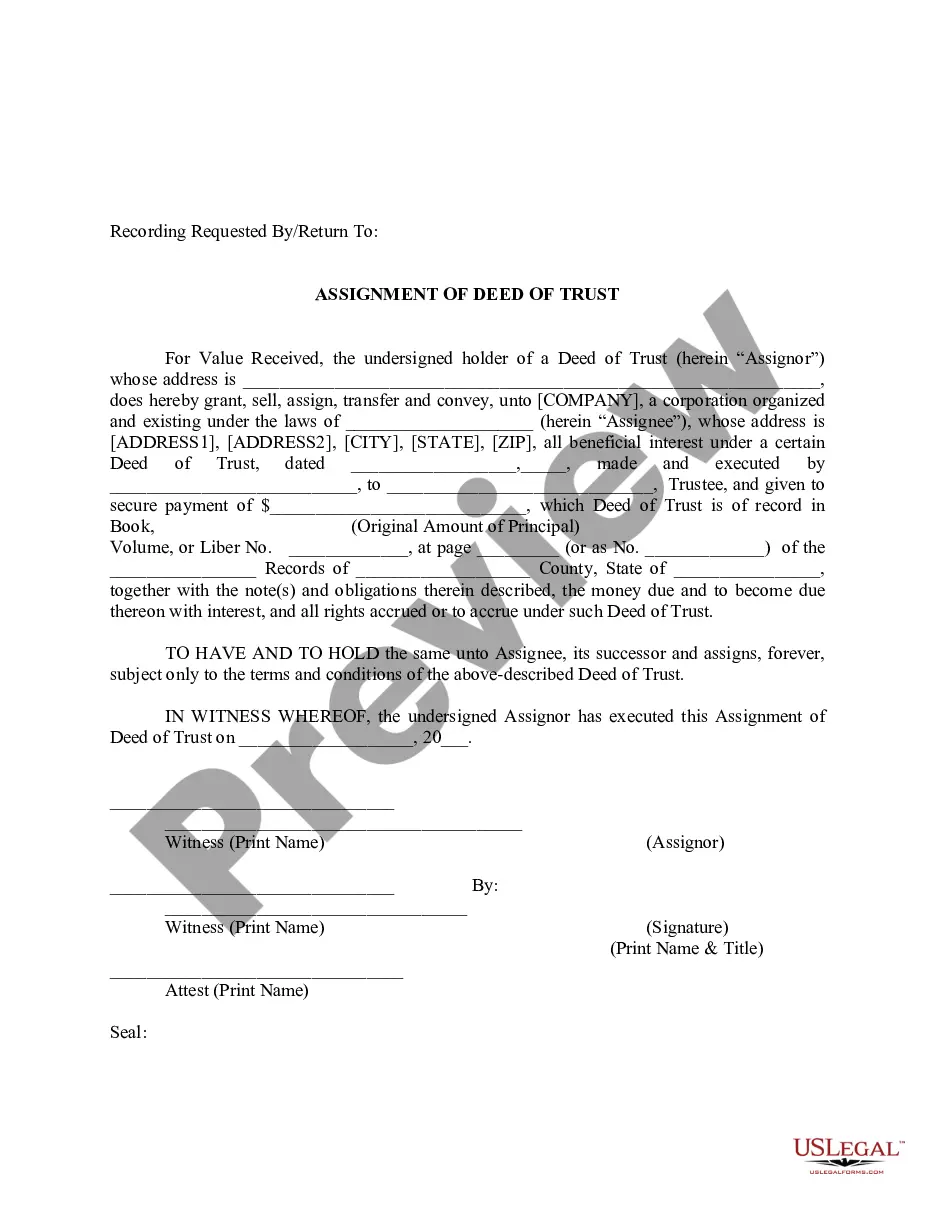

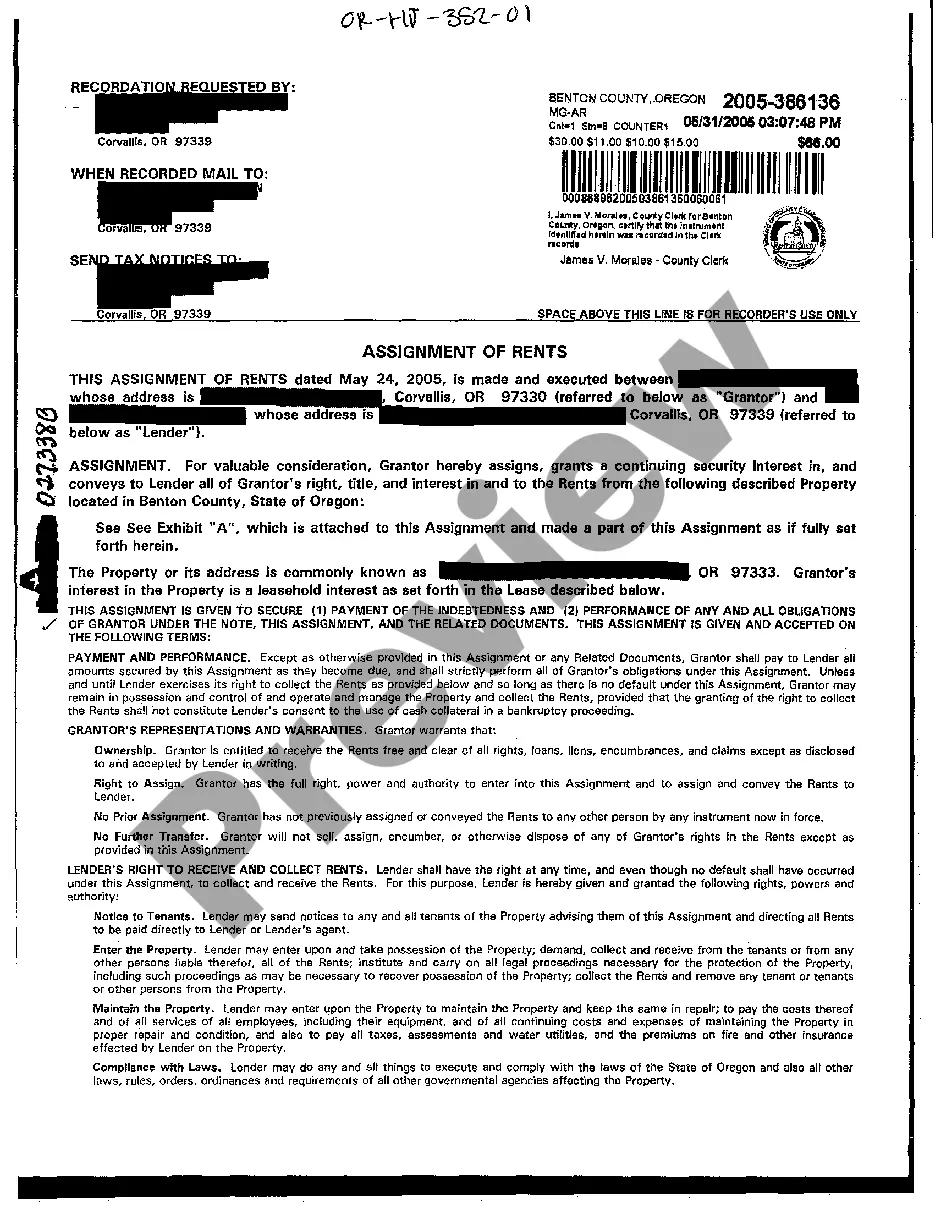

A receivable assignment agreement is an agreement by which a creditor – the “assignor” – assigns to another person – the “assignee” – a receivable it holds against a third person – the “assigned debtor”. The assigned debtor is not a party to the assignment agreement.

Assignment in the context of a receivable means the transfer of rights related to it to another person or entity. For this purpose, an appropriate contract is usually concluded (although this is not a necessary condition).

Assignment of receivables would mean sale of the lease rentals, not the asset. In that case, the leased asset still remains the property of the assignor – that is, the assignor has retained the residual interest in the asset. However, it would be different if the lessor sells the asset that has been leased out.

Therefore, when a journal entry is made for an accounts receivable transaction, the value of the sale will be recorded as a credit to sales. The amount that is receivable will be recorded as a debit to the assets. These entries balance each other out.

To report accounts receivable, gather information about outstanding amounts owed by customers, create an accounts receivable ledger, categorize the accounts by age, prepare a report that summarizes the outstanding amounts, analyze the report, and take action to collect payments and manage the balance.

Average accounts receivable is calculated as the sum of starting and ending receivables over a set period of time (generally monthly, quarterly or annually), divided by two.