Foreclosure Letter For Car Loan In King

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Yes, foreclosing a Car Loan can help you save on significant future EMIs and reduce the interest burden. However, it is essential to consider the foreclosure charges before making a decision.

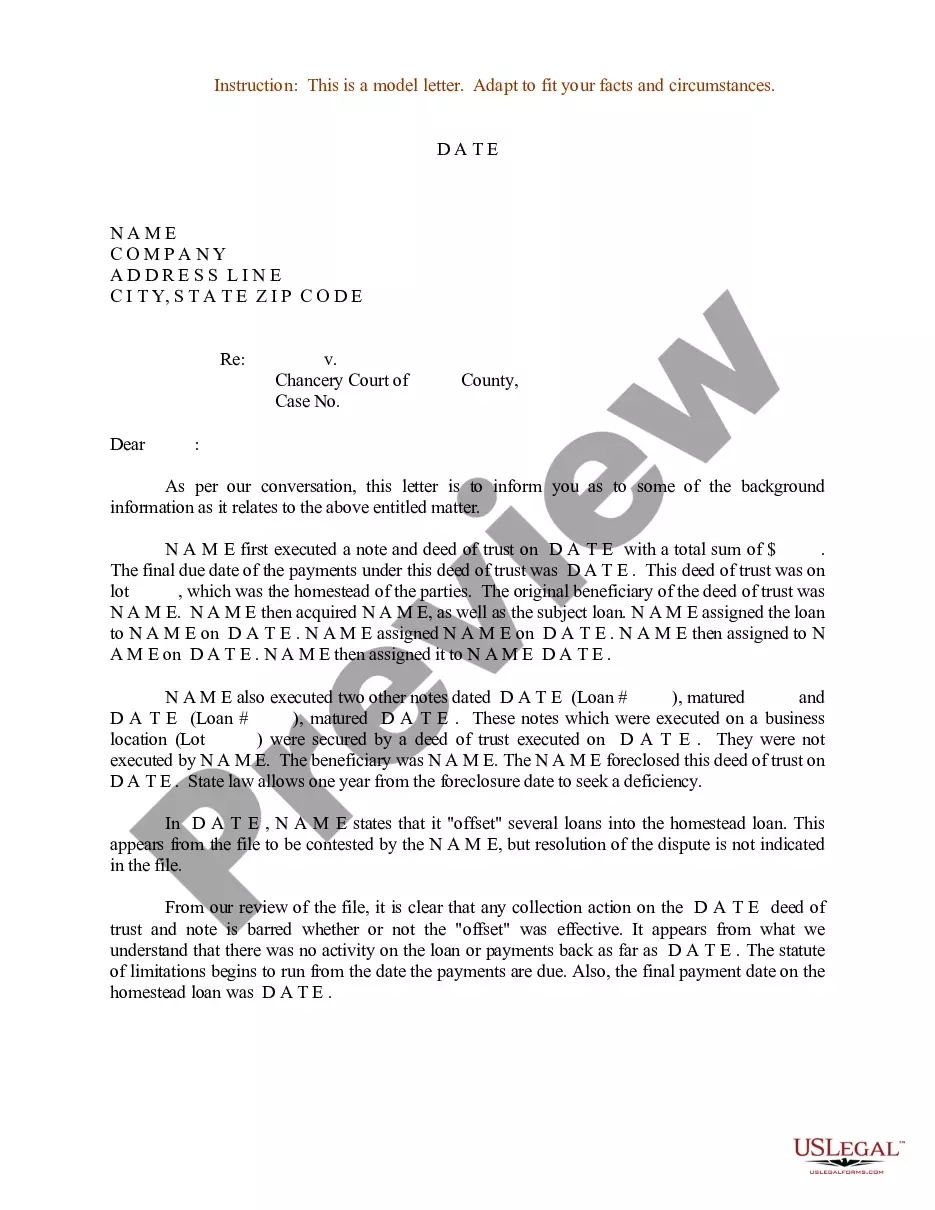

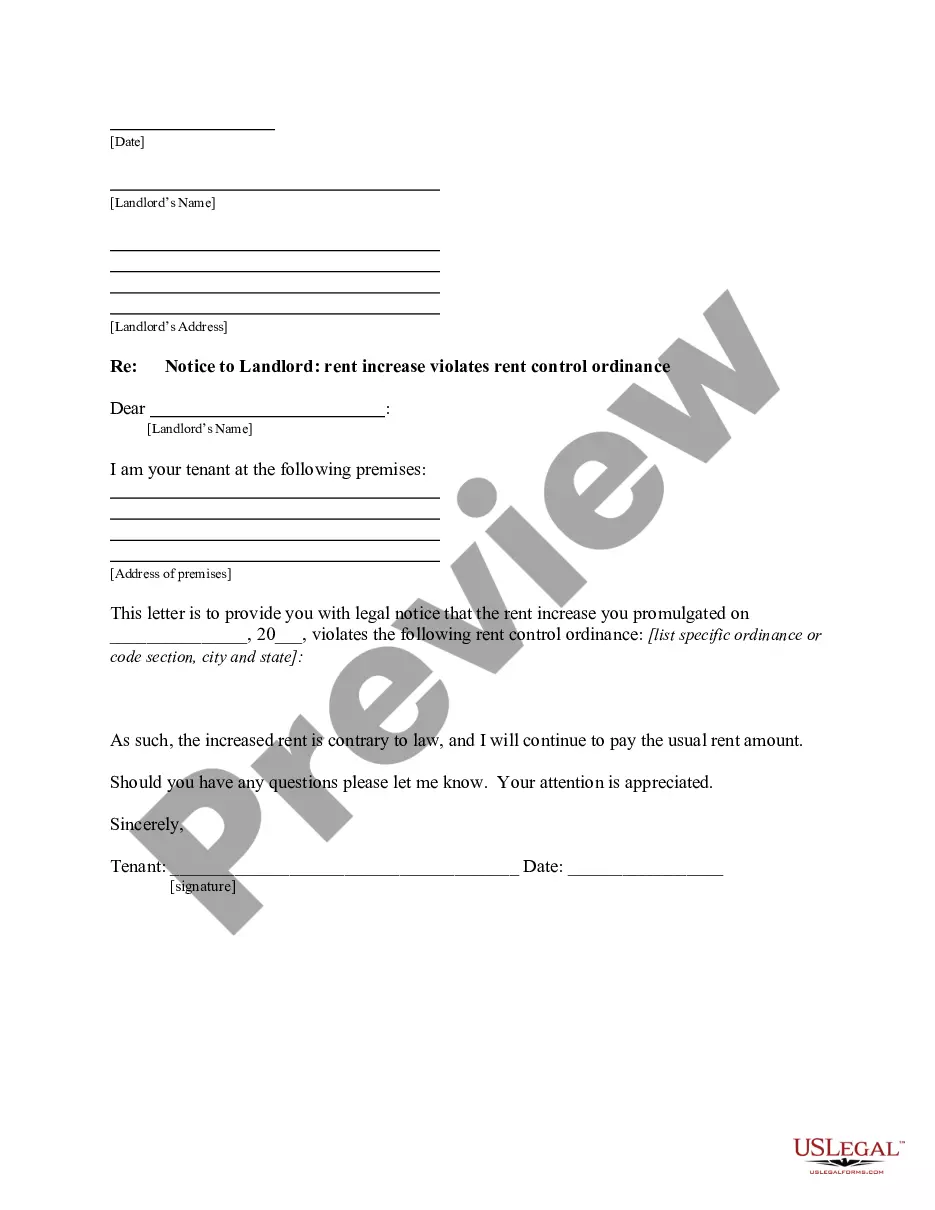

Dear RECIPIENT'S NAME, I am writing about a loan that I currently hold under the account number ACC/ LOAN NUMBER. This correspondence serves as a formal notice of my intention to fully liquidate this credit balance before the predetermined schedule.

Just go to your nearest home loan branch and ask them to apply for foreclosure letter which they will provide to after 7--8 days. Then you can see the outstanding amount in foreclosure letter and give the cheque of same amount to them.

While the content of the letter will change depending on your situation, there are a few important aspects to include: Provide all details the best you can, including correct dates and dollar amounts. Explain how and when all situations were resolved. Detail why problems won't happen again.

Even if you don't contest the foreclosure action, the sale usually won't occur until around a month after the judge issues a foreclosure order. So you'll probably have a couple of months from the first notice of the case to the date the court orders the sale.

Generally, federal law prohibits a lender from starting foreclosure until the borrower is more than 120 days past due.

It takes at least 6 to 8 months for a fore- closure lawsuit to go from summons and complaint to auction — even if you ignore the court case. In reality, however, the process is taking much longer. If you file an Answer and appear at the mandatory settlement conference, it is taking lenders 1 to 3 years to foreclose.

The actual amount of time that it takes for a foreclosure to start is up to the lender, but most lenders are going to wait at least 90 days -— or the time it takes for three missed payments to add up -— before they start the lawsuit.