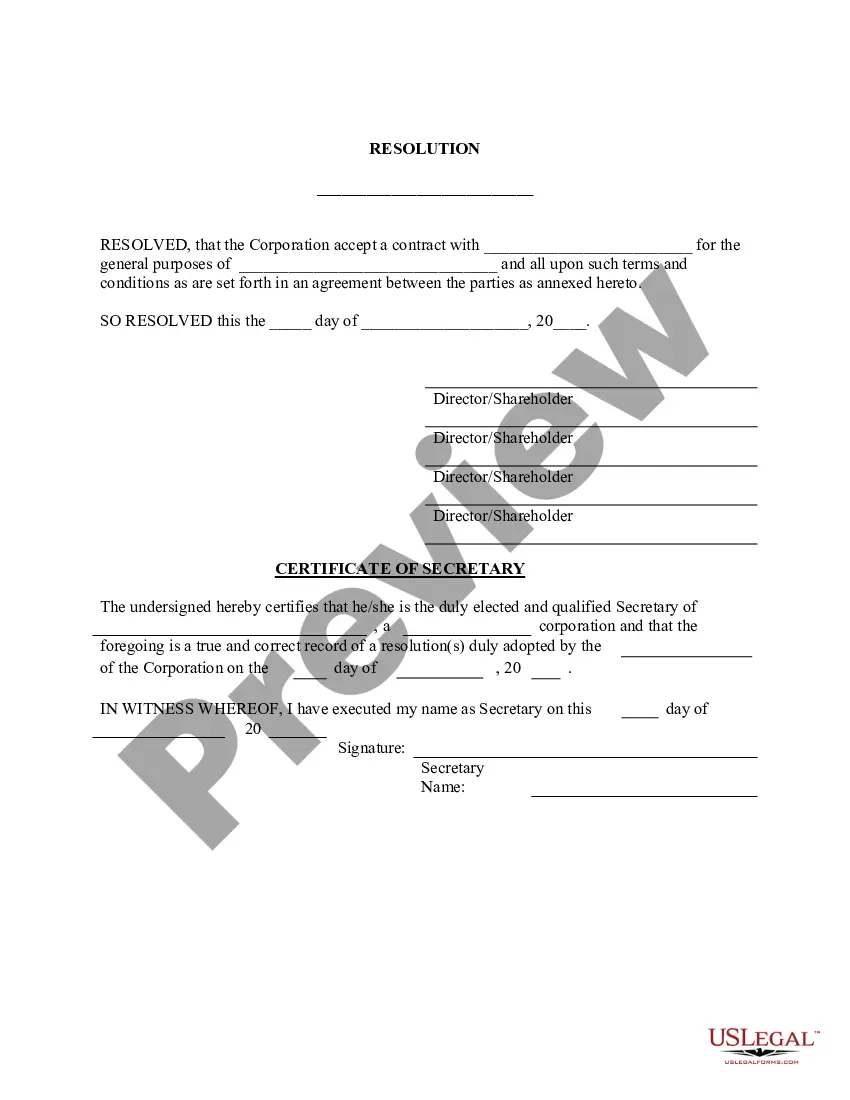

Auditor Appointment Resolution Format In Washington

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

An Audit Resolution Letter also known as a Management Decision Letter should clearly state whether or not the audit finding is sustained, the reasons for the decision, and the expected action to repay disallowed costs, make financial adjustments or take other action.

The Audit Resolution Report summarizes the status of corrective actions taken by state agencies to resolve exceptions to specific expenditures or financial transactions reported in audits conducted by the State Auditor's Office.

The most effective way to resolve an audit finding is by implementing a Corrective Action Plan (CAP) which address the underlying risk(s) associated with the audit finding.

Audit Resolution. An agreement between the primary organization (auditee) and the auditor on corrective actions to be taken for audit findings and recommendations (i.e., management concurs with the findings and recommendations, or a management decision is issued indicating concurrence and expected completion dates).

The Five C's of Internal Audits and Expert Recommendations 101 The Five C's of Internal Audits For ISO Certifications. C 1 – Criteria. The first step begins with criteria. C 2- Condition. C 3 – Cause. C 4 – Consequences. C 5 – Corrective Actions. Concluding Thoughts.

How do you resolve audit findings? Review each audit finding. Identify key deadlines for resolution. Seek clarification where necessary. Develop and implement a corrective action plan. Document your actions. Communicate with auditors. Test, review, and improve your process. Leverage audit insights for team upskilling.

An audit report structure should include a title page, table of contents, and executive summary. The introduction should explain the audit objectives, description of the scope, and methodology used to conduct the audit.

To appoint a subsequent auditor, certain documents must be submitted, including a certified resolution from the AGM, a written consent letter from the auditor, and a certificate confirming that the auditor is not disqualified under Section 141 of the Companies Act, 2013.