Auditor Appointment Resolution Format In California

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

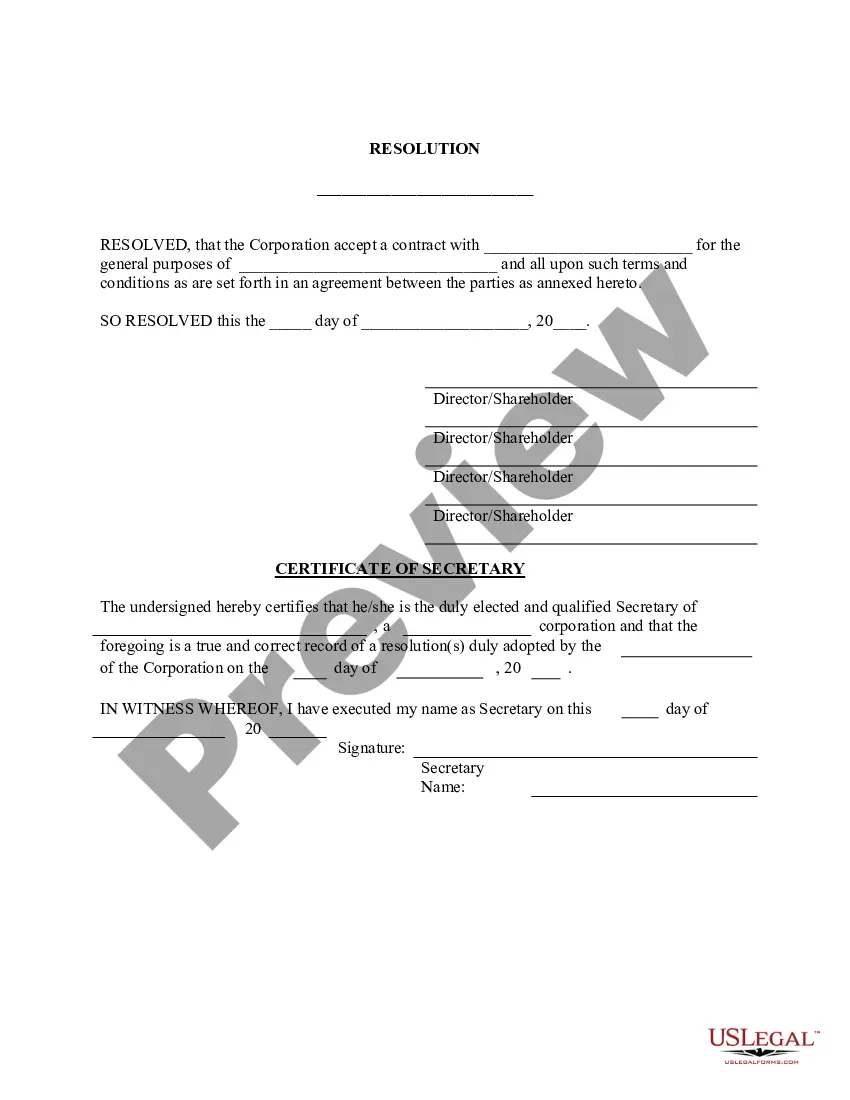

To appoint or re-appoint an auditor the members of a company must pass an Ordinary Resolution, subject to the provisions of the articles of association.

In most organisations, Board resolutions are typically required for actions with significant financial consequences; a change in procedures, or a change in governance authority. Board resolutions are important for an organisation to keep a record of these crucial decisions made by the Board of directors.

Form ADT-1 is an intimation filed by companies with the Registrar of Companies about the appointment of an auditor after the conclusion of the Annual General Meeting (AGM) under Section 139 (1) of the Companies Act, 2013.

The Companies Act 2006 allows you to appoint an auditor in three ways: by directors' resolution, in members' general meeting or by way of written resolution.

Ing to Section 139(8) of the Companies Act 2013, read in conjunction with the Companies (Audit and Auditor) Rules, 2014, a company can appoint a statutory auditor with a special resolution. If a special resolution is not passed, an ordinary resolution can also be considered for the appointment.

“RESOLVED THAT Consent of the Board is to be and is hereby given for appointment of AUDITOR FIRM NAME, Chartered Accountants as statutory Auditor of the Company and Directors of the Company be and is hereby authorized to fix the remuneration from time to time.

“RESOLVED THAT under the provisions of Section 138 of the Companies Act 2013 read with Rule 13 of the Companies (Accounts) Rules, 2014 and other applicable provisions if any of the Companies Act, 2013, the consent of the Board of Directors be and is hereby ed for the appointment of Mr ________, Resident of ...

Form ADT-1 is an intimation filed by companies with the Registrar of Companies about the appointment of an auditor after the conclusion of the Annual General Meeting (AGM) under Section 139 (1) of the Companies Act, 2013.

The following are the companies are mandatorily required to appoint an internal auditor: Any listed companies. Any unlisted public company having- Paid-up share capital of Rs. 50 crore or above during the preceding financial year. In case of any private companies having- Annual turnover of income of Rs.