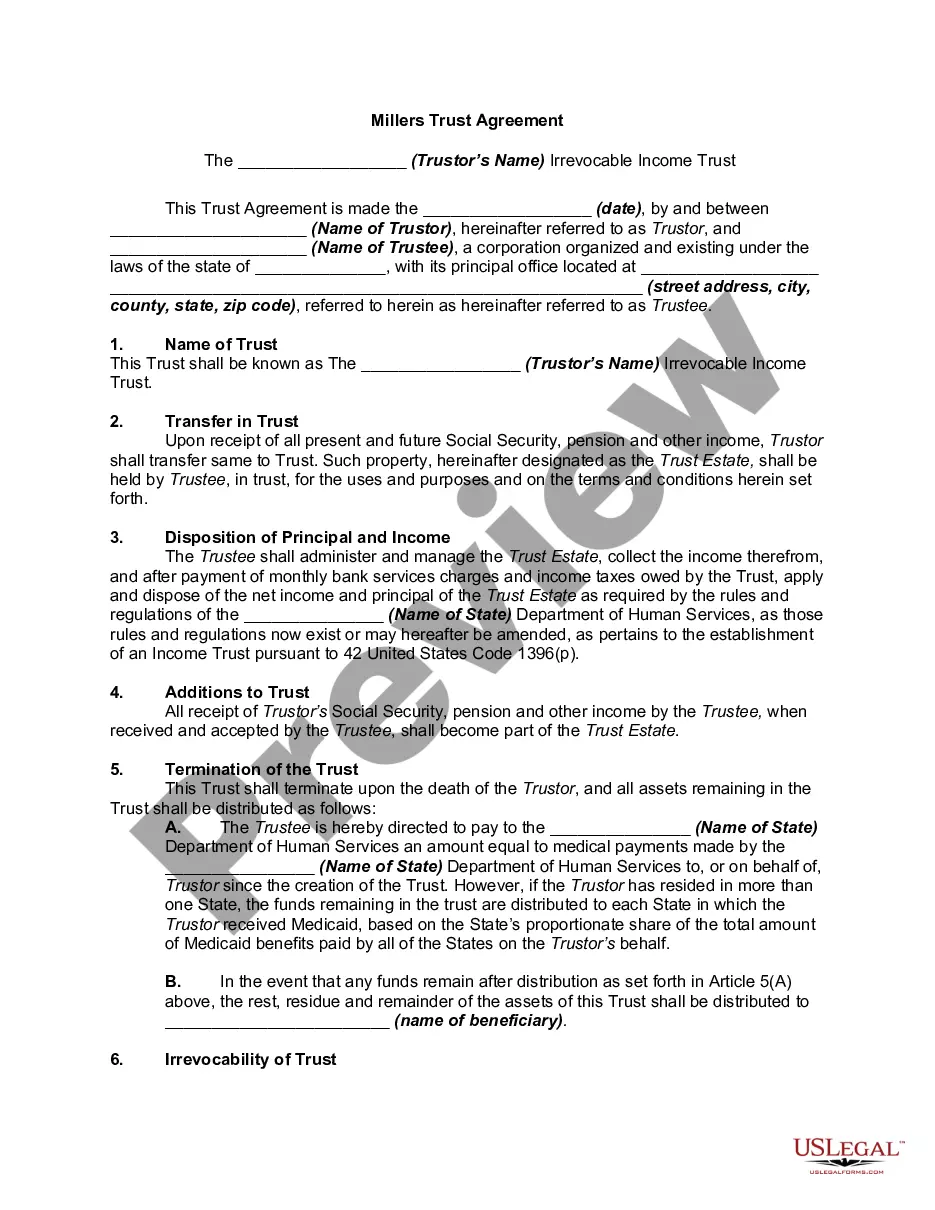

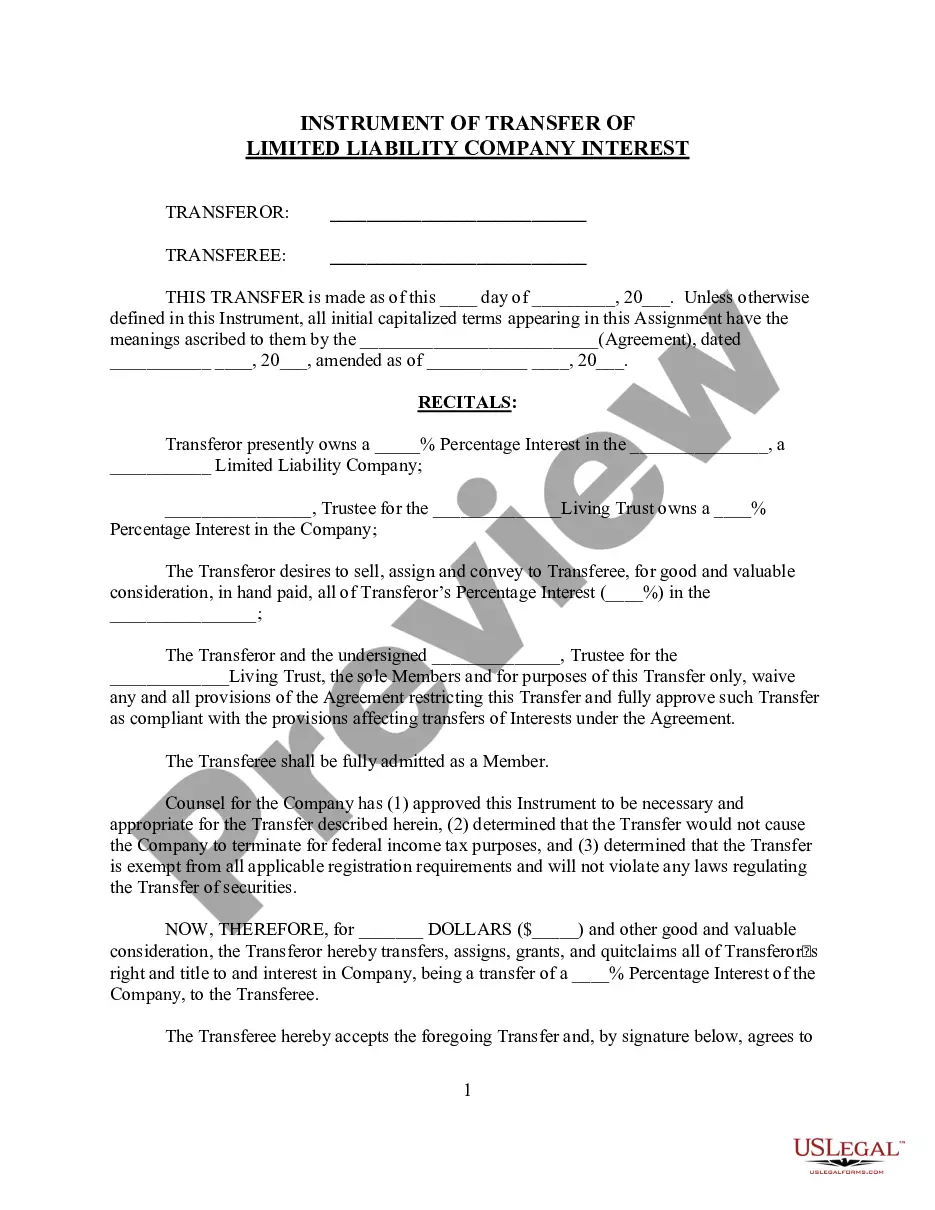

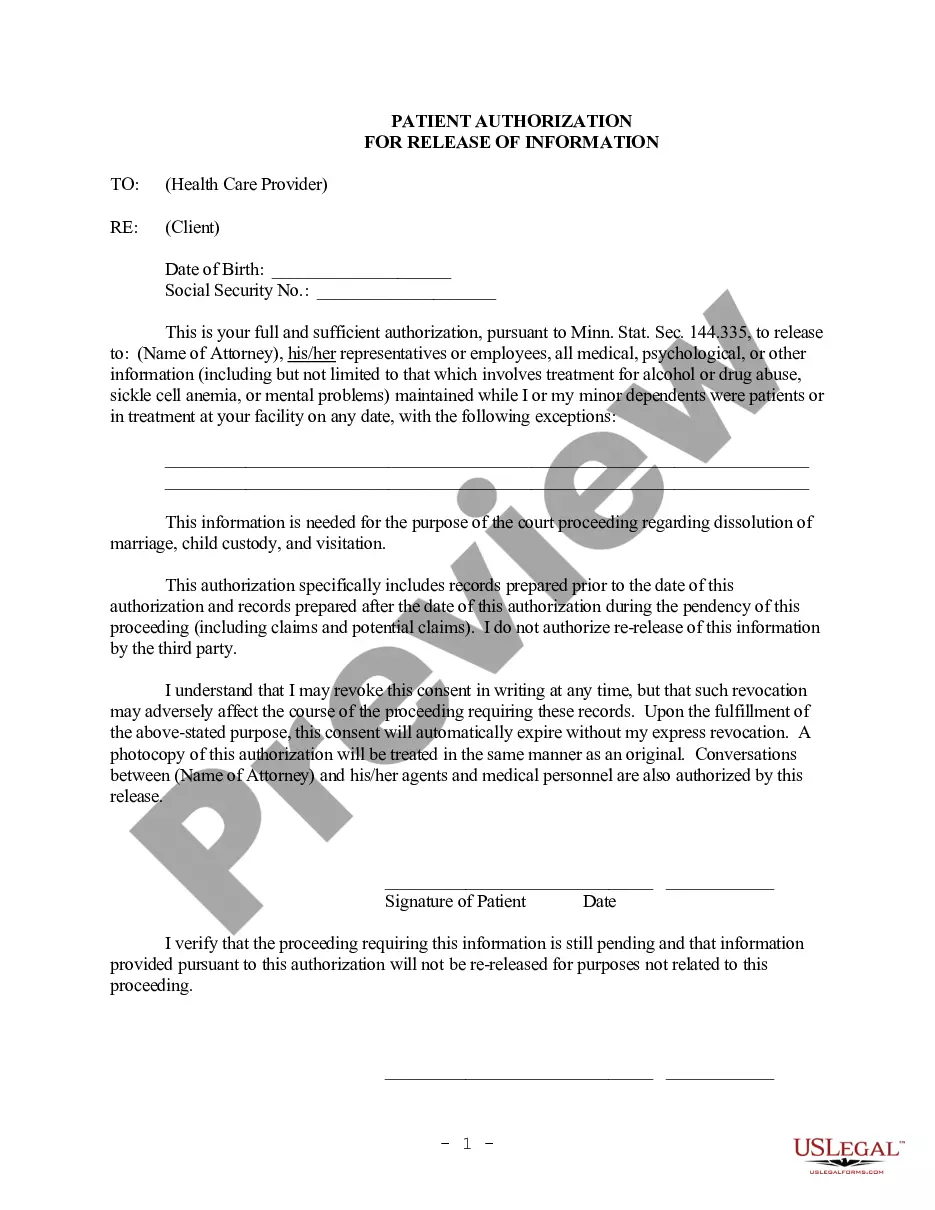

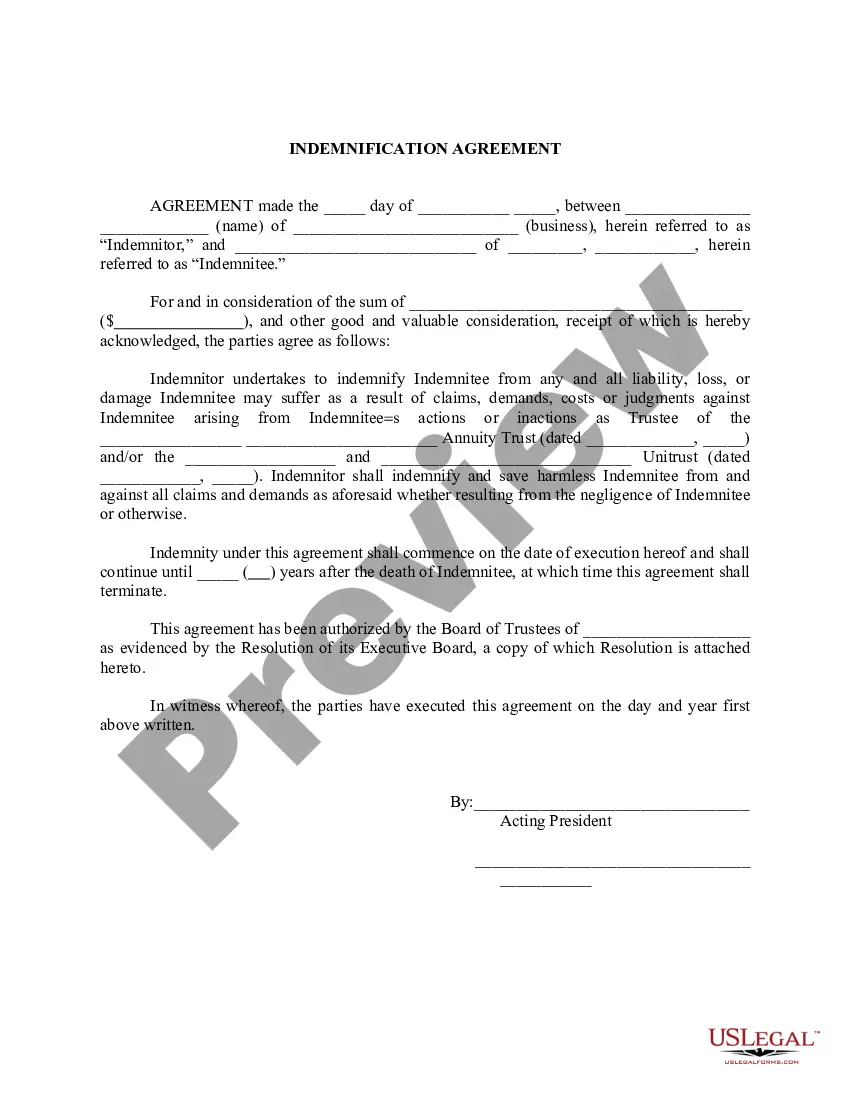

Surviving Spouse Requirements In Minnesota

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

N Owners have survivorship rights. If one joint-owner dies, that owner's interest in the property passes to the other joint owners. For example if one of two joint owners dies, the survivor becomes the sole owner of the property.

Section 524.6-204 - RIGHT OF SURVIVORSHIP (a) Sums remaining on deposit at the death of a party to a joint account belong to the surviving party or parties as against the estate of the decedent unless: (1) there is clear and convincing evidence of a different intention; or (2) there is a different disposition made by a ...

A surviving spouse is a husband or wife who outlives their partner. This includes both widows and widowers. The term is often used in legal contexts such as estate taxation, probate, and estate administration. Example 1: John and Jane were married for 30 years. When John passed away, Jane became his surviving spouse.

The right of survivorship does override any wills that are in place. That's because this kind of arrangement avoids probate. 5 But if the last surviving party in a JTWROS dies, the agreement no longer applies, which means the asset or property is included in their will and goes to their heirs.

To qualify for the Qualifying Surviving Spouse filing status, you must meet these four requirements: You qualified for Married Filing Jointly with your spouse for the year they died. You didn't remarry. You have a child, stepchild, or adopted child you claim as your tax dependent.

Under the right of survivorship, each tenant possesses an undivided interest in the whole estate. When one tenant dies, the tenant's interest disappears and the others tenants' shares increase proportionally and obtain the rights to the entire estate.

Your property will go to your spouse or closest relatives. If you have a spouse and children, the property will go to them by a set formula. If not, the property will descend in the following order: grandchildren, parents, brothers and sisters, or more distant relatives if there are no closer ones.

Minnesota Surviving Spouses – The Homestead A surviving spouse has a statutory right – for a limited period of time after the decedent's death – to elect to receive certain rights in the decedent's homestead, including a manufactured home which is the family residence.

Qualifying Surviving Spouse Filing Status Taxpayers who do not remarry in the year their spouse dies can file jointly with the deceased spouse. For the two years following the year of death, the surviving spouse may be able to use the Qualifying Surviving Spouse filing status.

Form 56, which notifies the IRS that the surviving spouse or executor has taken over the decedent's affairs. Or, a copy of a letter from the court that grants the personal representative of the deceased the authority to manage his or her affairs, called the Letters Testamentary.