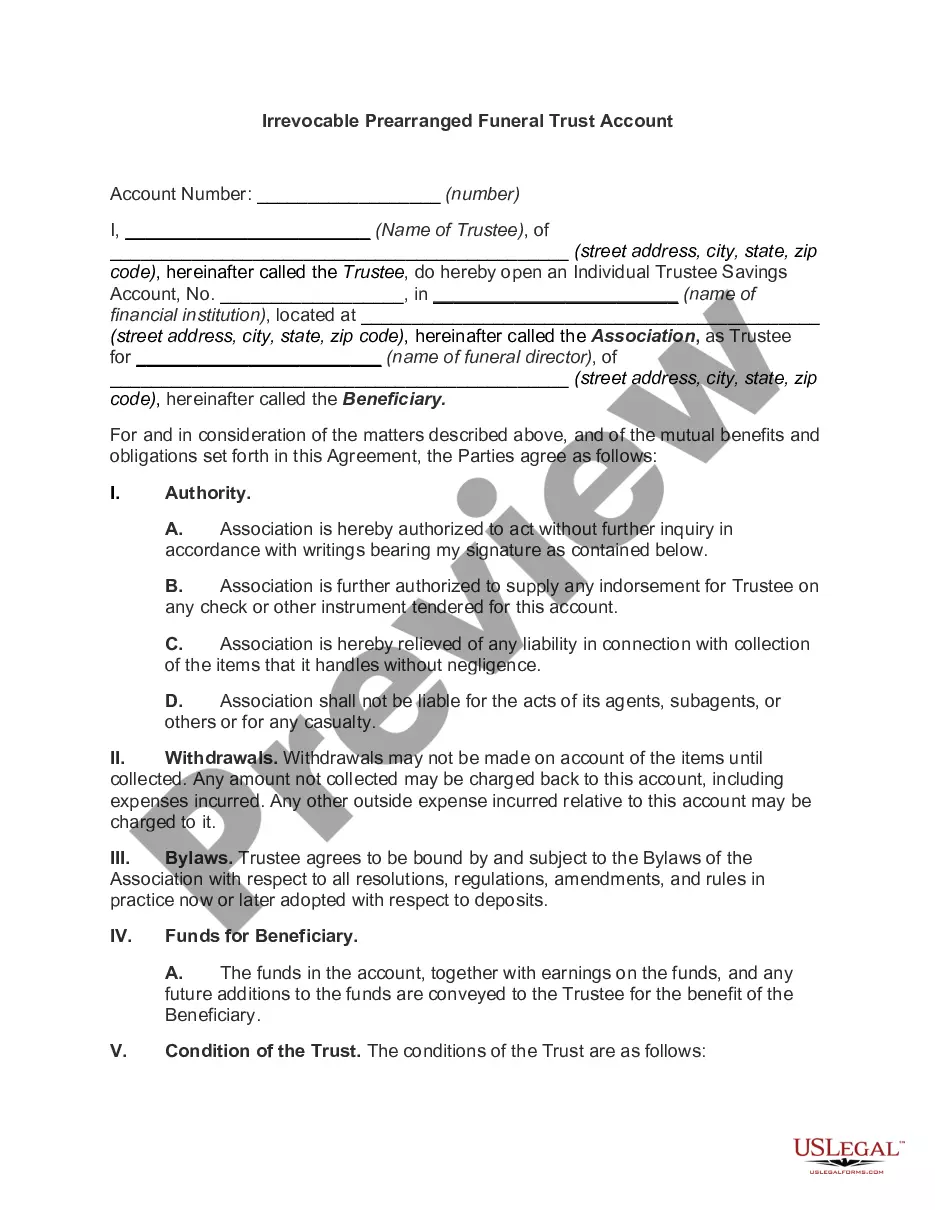

Account For Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Nevada Financial Account Transfer To Living Trust?

- If you are an existing user, log in to your account and verify your subscription status. If necessary, renew it based on your payment plan.

- For first-time users, preview available forms and descriptions to ensure you select the correct document for your needs and jurisdiction.

- If needed, utilize the Search tab to locate specific templates that may better suit your requirements.

- Select your desired document and click 'Buy Now', choosing your preferred subscription plan as you register for an account to access all resources.

- Submit your payment via credit card or PayPal to complete the transaction.

- Once your purchase is finalized, download the form to your device and find it in the My Forms section of your profile for future access.

With US Legal Forms, you gain access to a vast collection of legal documents that empower both individuals and attorneys to create precise and legally sound paperwork with ease.

Start simplifying your legal needs today! Visit US Legal Forms to explore the extensive library and streamline your document preparation.

Form popularity

FAQ

The main purpose of a trust account is to safeguard funds and ensure they are used appropriately for the benefit of a designated individual or organization. These accounts prevent misuse by keeping funds separate from a trustee’s personal finances. They also help in maintaining clear records of transactions, fostering accountability. Establishing an account for trust is essential for legal compliance and trust integrity.

Generally, personal checking or savings accounts cannot be used for a trust, as they do not meet the necessary legal requirements for managing trust assets. Additionally, commercial accounts that lack specific provisions for trust management may not offer the benefits essential for proper trust administration. It is crucial to set up a dedicated account for trust to ensure compliance and effective management.

An account in trust is specifically designed to hold and manage assets for beneficiaries as specified in a trust agreement. This type of account serves various purposes, such as protecting assets, ensuring streamlined disbursements, and providing tax advantages. A well-structured account for trust directly supports the intentions outlined by the grantor.

Yes, a trust should have its own bank account to separate its assets from personal funds, which helps avoid legal complications and simplifies accounting. Opening a dedicated account for trust ensures transparency and proper management of the trust's finances. Additionally, it allows for easier tracking of income and distributions to beneficiaries.

When determining the best account for trust, consider options like interest-bearing trust accounts that provide returns while maintaining liquidity for the trust's needs. These accounts cater specifically to trusts, offering better rates and fewer restrictions than regular accounts. Always ensure that the account aligns with the goals outlined in your trust document.

The best type of account for a trust is typically a dedicated trust account, which is designed to hold assets for beneficiaries while ensuring compliance with legal requirements. These accounts often come with additional features like asset management and investment opportunities. A dedicated account for trust helps streamline the administration process and safeguards the trust's assets.

Choosing the right bank for a trust account involves considering several factors, such as fees, services, and reputation. Look for banks that specialize in trust services and offer tailored options for trust management. A strong choice will provide flexibility and allow for easy management of the assets held in the account for trust.

The biggest mistake parents make when setting up a trust fund is not clearly communicating their intentions to beneficiaries. Without clear guidance, family members may misinterpret the trust's provisions, leading to disputes. Additionally, inadequate accounting for trust assets can cause financial mismanagement, so detailed planning and open discussions are crucial.

To set up a bank account for a trust, you will need a copy of the trust document, identification for the trustee, and possibly a tax identification number for the trust. Most banks require this documentation to verify the trust's legitimacy. Once you have these items, visit a bank that offers trust accounts to kick-start the process.

Whether your parents should put their assets in a trust depends on their financial goals and circumstances. Trusts can provide benefits like asset protection and streamlined estate planning. However, it's essential to weigh these advantages against the responsibilities and costs involved in managing the accounting for trust assets.