Rate Commercial Real Estate Withholding

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

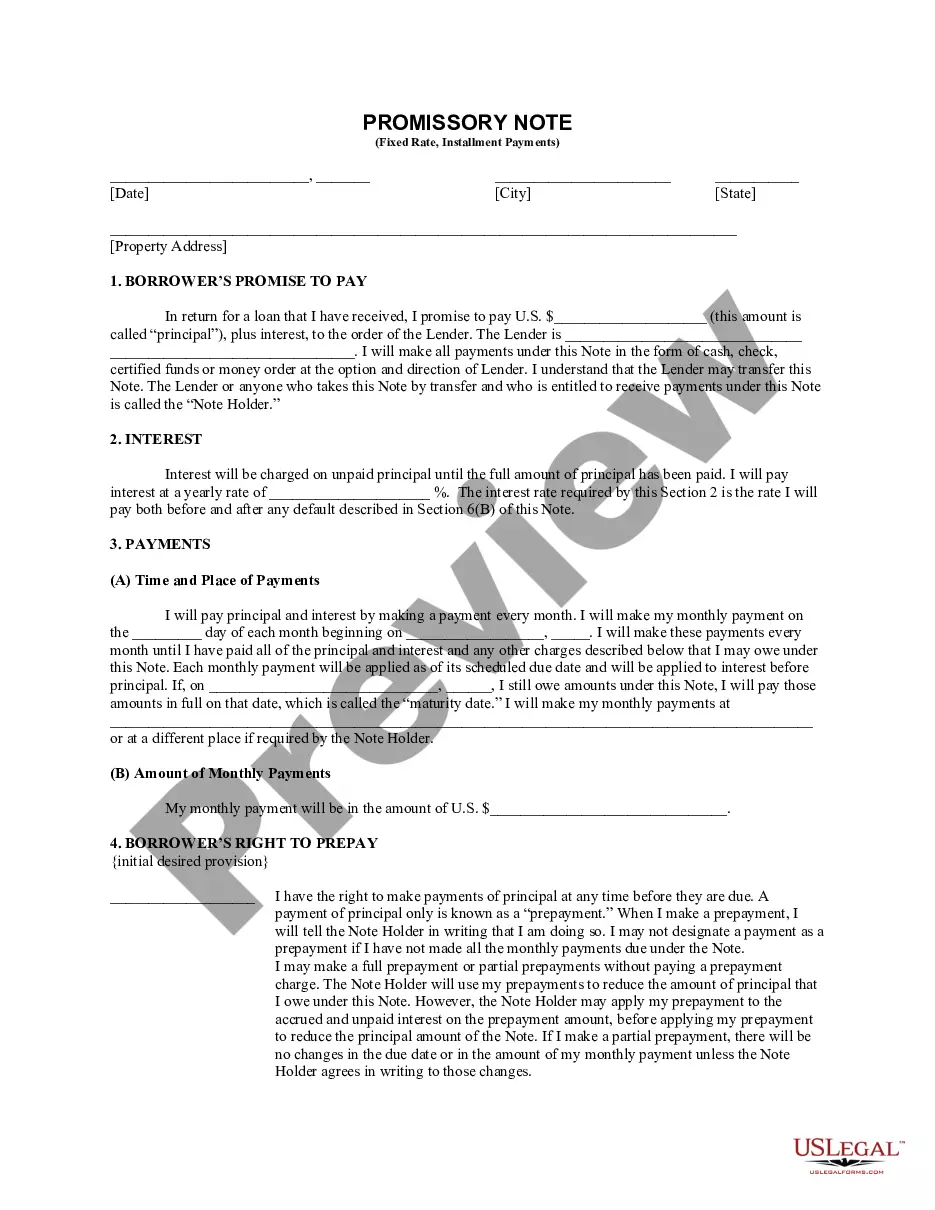

How to fill out California Installments Fixed Rate Promissory Note Secured By Commercial Real Estate?

It’s clear that you cannot transform into a legal expert instantaneously, nor can you determine how to swiftly prepare Rate Commercial Real Estate Withholding without a specialized skill set.

Drafting legal documents is a prolonged process that necessitates specific training and abilities. So why not entrust the preparation of the Rate Commercial Real Estate Withholding to the experts.

With US Legal Forms, one of the most comprehensive legal template collections, you can find everything from court documents to templates for internal communication.

You can access your documents again from the My documents section at any time. If you are an existing customer, you can simply Log In, and locate and download the template from the same section.

Regardless of the aim of your forms—be it financial, legal, or personal—our website has you covered. Give US Legal Forms a try now!

- Identify the document you require using the search bar at the top of the page.

- View it (if this option is available) and read the accompanying description to determine if Rate Commercial Real Estate Withholding meets your needs.

- Start your search anew if you require another form.

- Create a free account and select a subscription plan to acquire the document.

- Click Buy now. After the purchase is finalized, you can obtain the Rate Commercial Real Estate Withholding, complete it, print it, and send or deliver it to the appropriate individuals or organizations.

Form popularity

FAQ

California withholding is reported on Form 540/540NR either as real estate and other withholding (Form 540, line 73 or Form 540NR, line 83), representing withholding reported via Forms 593 or 592-B or as California income tax withheld (Form 540, line 71 or Form 540NR, line 81), representing all other sources of ...

Real estate withholding is a prepayment of income tax due from the selling of California land or anything on it (real property). Examples of real property: Vacant land. Buildings.

The withholding is 3 1/3% (. 0333) of the down payment during escrow. Buyers/Transferees are required to withhold on the principal portion of all payments made following the close of the real estate transaction unless an approval letter for the elect-out method is received.

Any person who withheld on the sale or transfer of California real property during the calendar month must file Form 593 to report, and Form 593-V to remit the amount withheld. Normally, this will be the title company, escrow company, intermediary, or accommodator.

Real estate withholding is a prepayment of taxes. It is not an additional tax. Who is responsible for withholding? The law holds the buyer (called the transferee) responsible for withholding. In most real estate transactions, the escrow holder transmits the tax to the Franchise Tax Board.