Joint Tenancy California Tax Implications

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

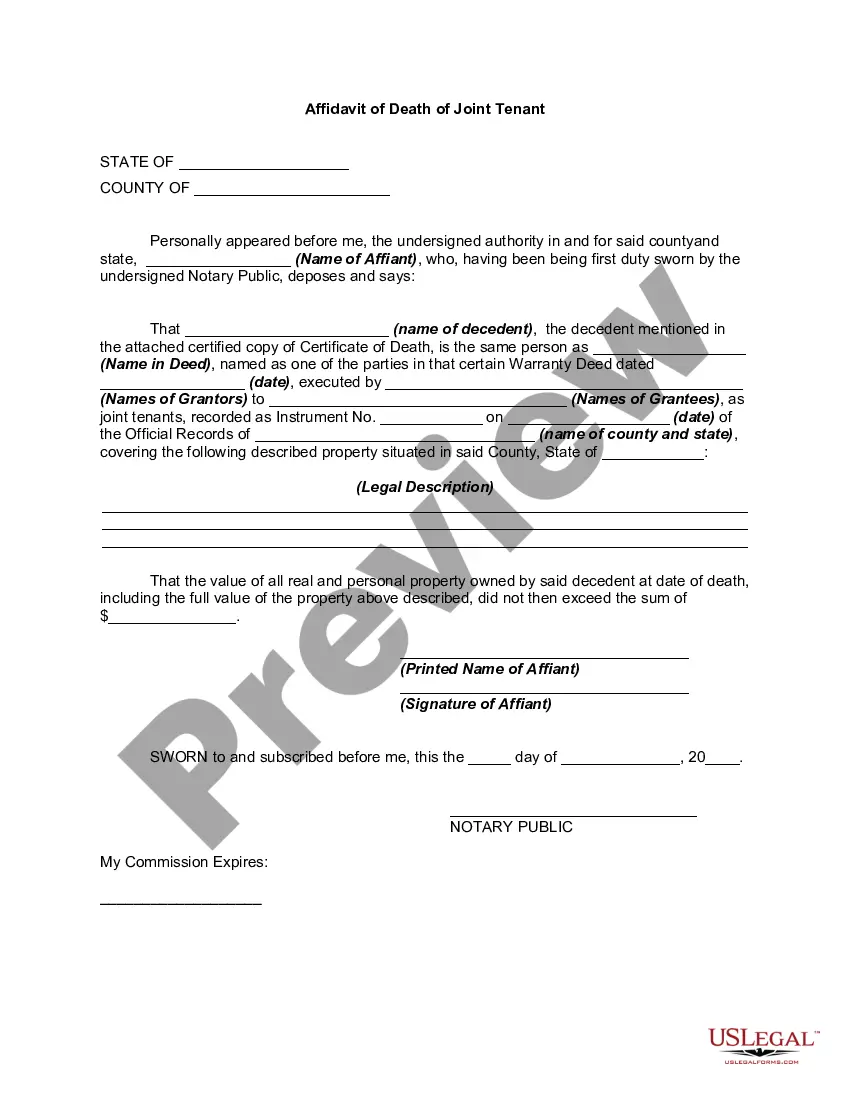

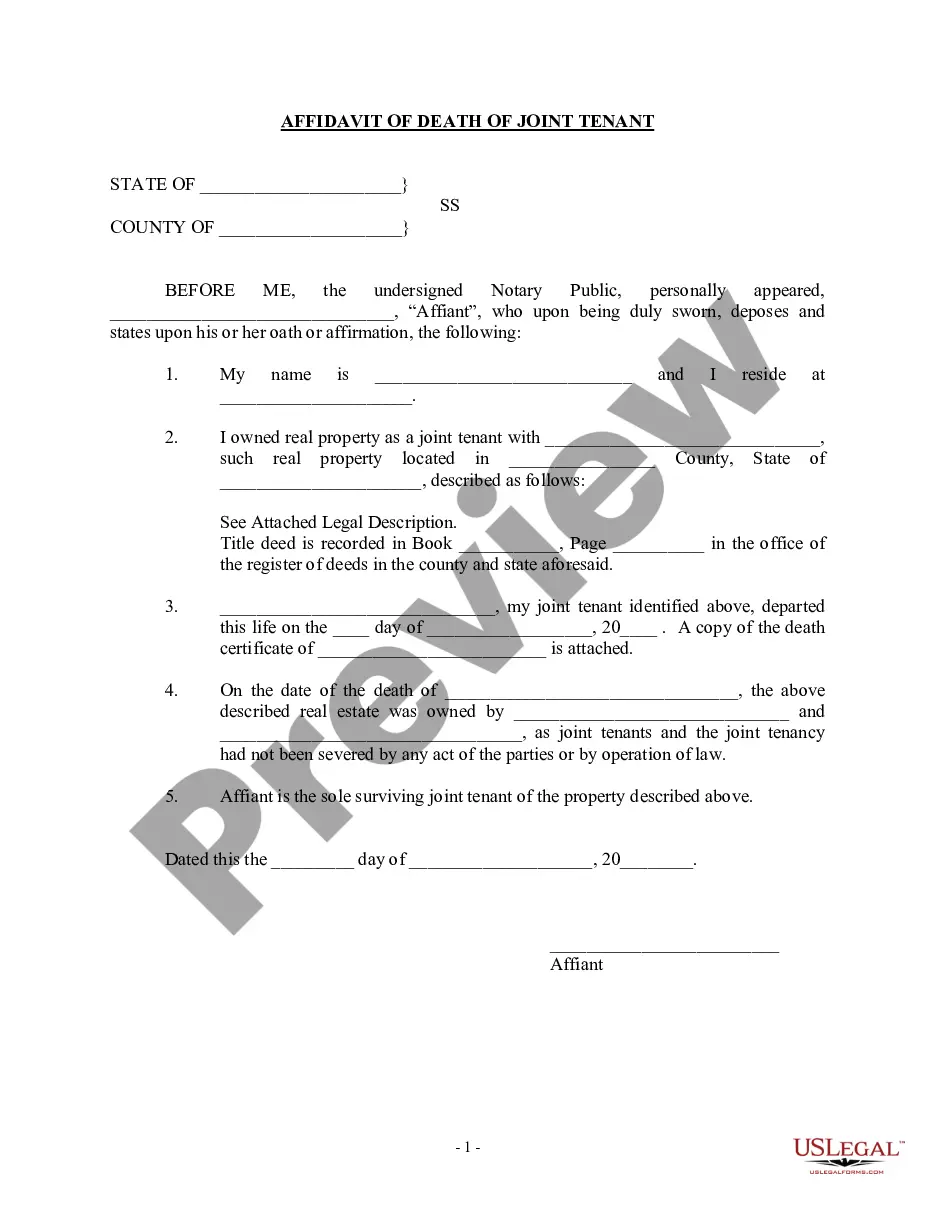

How to fill out California Affidavit Of Death Of Joint Tenant?

Managing legal documents can be exasperating, even for the most seasoned professionals.

When you are looking for Joint Tenancy California Tax Implications and lack the time to search for the correct and current version, the process can be overwhelming.

US Legal Forms accommodates any needs you may have, from personal to business documents, all in one location.

Leverage advanced tools to complete and manage your Joint Tenancy California Tax Implications.

Here are the steps to follow after finding the form you need: Confirm it is the right form by previewing it and reviewing its description. Ensure the template is recognized in your state or county. Click Buy Now when you are ready. Choose a subscription plan. Select the format you prefer, and Download, fill out, eSign, print, and submit your documents. Take full advantage of the US Legal Forms web library, backed by 25 years of experience and reliability. Streamline your daily document management into a simple and intuitive process today.

- Utilize a valuable resource library of articles, guides, and handbooks related to your situation and requirements.

- Save time and effort in locating the documents you need, and utilize US Legal Forms’ enhanced search and Preview feature to find Joint Tenancy California Tax Implications and download it.

- If you have a subscription, Log In to your US Legal Forms account, search for the form, and download it.

- Check your My documents section to view the documents you previously saved and manage your folders as you wish.

- If this is your first experience with US Legal Forms, create an account and gain unlimited access to all the platform's advantages.

- A robust online form library can significantly aid anyone wanting to handle these matters efficiently.

- US Legal Forms is a leading provider of online legal forms, offering over 85,000 state-specific legal documents available at your convenience.

- With US Legal Forms, you can access state- or county-specific legal and business forms.

Form popularity

FAQ

Joint Tenancy is a way of holding title to a property in California, where two or more individuals own the property together with equal rights of ownership. When one owner passes away, their share of the property automatically transfers to the surviving owners.

In the case of joint owners, each owner generally has the right to lease out property that is jointly owned. This means that one owner can enter into a lease agreement with a tenant without the permission of the other co-owner(s).

Joint Tenancy is a way of holding title to a property in California, where two or more individuals own the property together with equal rights of ownership. When one owner passes away, their share of the property automatically transfers to the surviving owners.

So long as the individuals and the legal entity have the same proportional ownership interests, the real property will not be reassessed when transferred to or from the entity or the individual. A and B can transfer property owned by them 50/50 to an LLC owned by them 50/50 without reassessment.

Adding a family member to the deed as a joint owner for no consideration is considered a gift of 50% of the property's fair market value for tax purposes. If the value of the gift exceeds the annual exclusion limit ($16,000 for 2022) the donor will need to file a gift tax return (via Form 709) to report the transfer.