Request for Information from Credit Reporting Agency

About this form

The Request for Information from Credit Reporting Agency form is a legal document that allows consumers to formally request details regarding adverse information presented on their credit report. Under the Fair Credit Reporting Act, this form ensures that consumers can clarify and understand negative entries on their credit history, making it distinct from other credit-related forms that may not specifically address the request for information about adverse data.

Key parts of this document

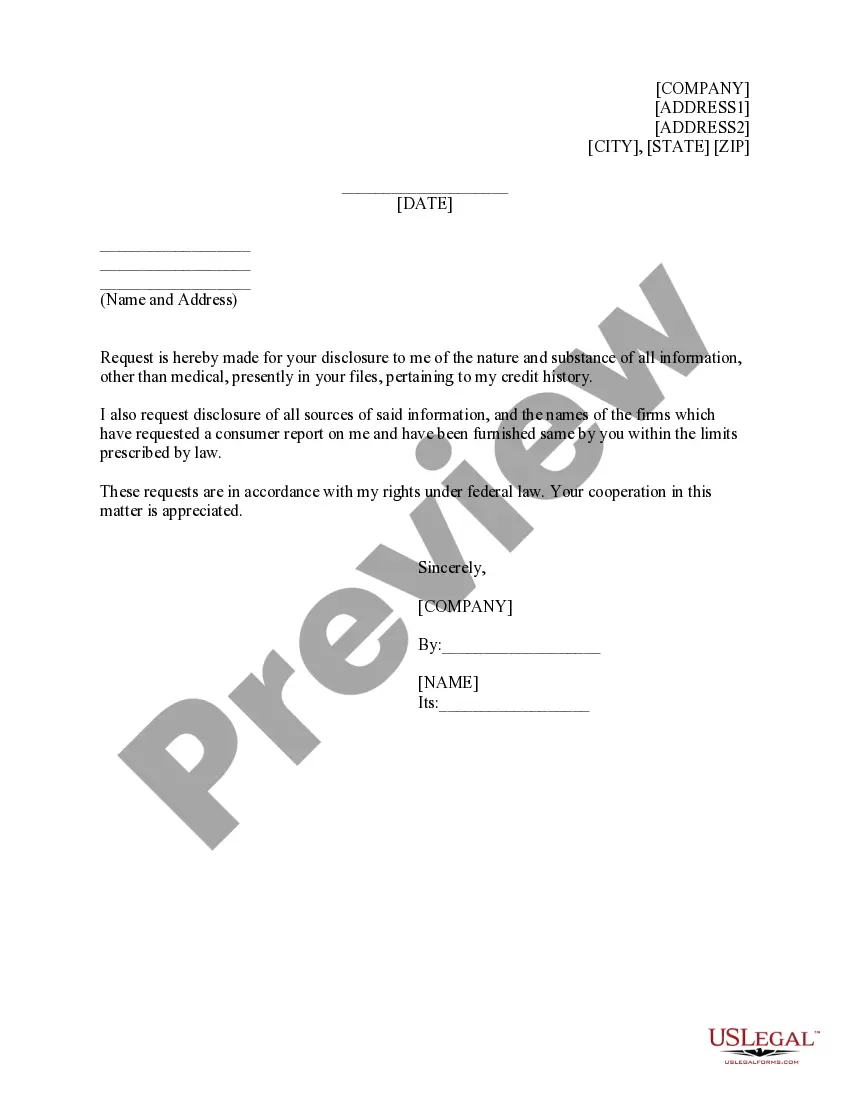

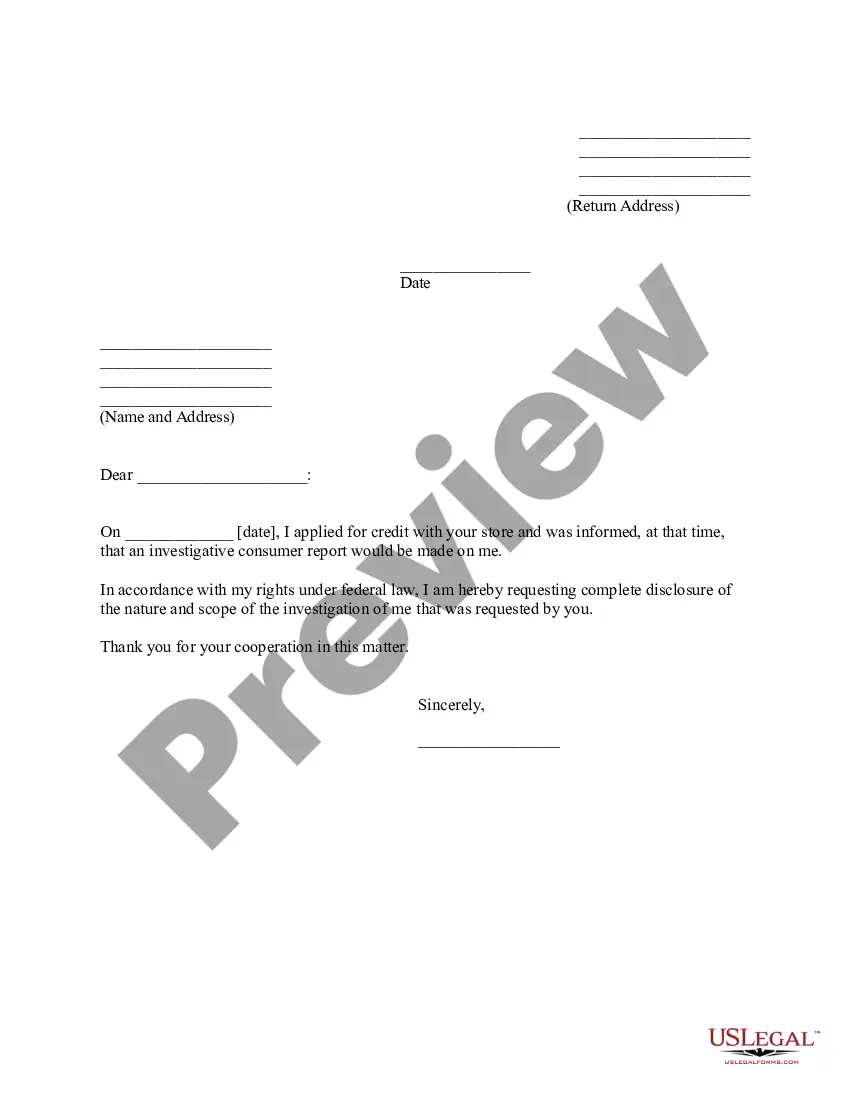

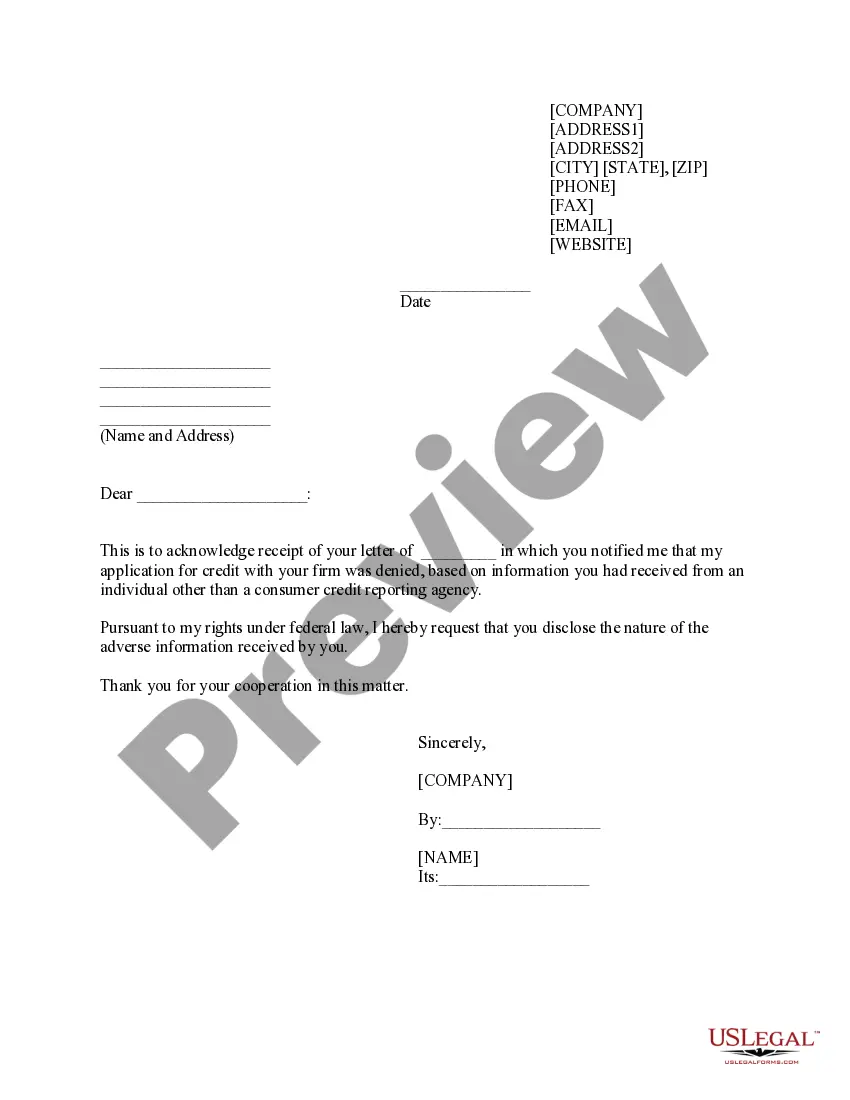

- Return address: Where the request will be sent.

- Date field: When the request is made.

- Name and address: The individual making the request.

- Address of the credit reporting agency: Where the request is directed.

- Statement of request: Providing a clear outline of the information being sought.

- Signature line: To authenticate the requester's identity.

When to use this document

This form is useful in situations where a consumer notices negative information on their credit report and wishes to understand its origin or validity. It can be used if a consumer has been denied credit, or if they simply want clarity on how certain adverse information may be impacting their credit score.

Who should use this form

Eligibility for using this form typically includes:

- Consumers who have received a notice regarding adverse information from a credit reporting agency.

- Individuals seeking to clarify specific negative entries on their credit report.

- Anyone looking to ensure their credit report is accurate and comprehensive.

How to complete this form

- Identify the return address where the request will be sent.

- Enter the current date to indicate when the request is made.

- Provide your name and address to identify yourself as the requester.

- Specify the name and address of the credit reporting agency you are addressing.

- Clearly articulate your request for information regarding adverse data on your credit report.

- Sign the form to validate your request.

Is notarization required?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include the correct address of the credit reporting agency.

- Not signing the form, which is necessary for validation.

- Leaving out important identifying information, such as full name or address.

- Completing the form without a clear statement of the information requested.

Benefits of using this form online

- Convenient access allows you to complete the form from anywhere at your convenience.

- Editability confirms that you can ensure all fields are accurately filled before submission.

- Reliable templates drafted by licensed attorneys protect your legal rights.

Summary of main points

- The Request for Information from Credit Reporting Agency helps consumers understand adverse information on their credit reports.

- It is crucial to complete the form accurately and provide all requested information.

- Using this form can facilitate communication with credit reporting agencies, helping to clarify any discrepancies.

Looking for another form?

Form popularity

FAQ

A business uses a 623 credit dispute letter when all other attempts to remove dispute information have failed. It refers to Section 623 of the Fair Credit Reporting Act and contacts the data furnisher to prove that a debt belongs to the company.

A 609 Dispute Letter is often billed as a credit repair secret or legal loophole that forces the credit reporting agencies to remove certain negative information from your credit reports.

No one should request your credit report without a valid purpose allowed by the law. Anyone who uses or obtains a copy of your credit report under false pretenses may be subject to civil and criminal penalties.

A 609 letter is a credit repair method that requests credit bureaus to remove erroneous negative entries from your credit report. It's named after section 609 of the Fair Credit Reporting Act (FCRA), a federal law that protects consumers from unfair credit and collection practices. Written by Natasha Wiebusch, J.D..

Your name, address, full or partial Social Security number, date of birth, and possibly employment information. Your existing credit. Information about credit that you have, such as your credit card accounts, mortgages, car loans, and student loans.

You have the right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

There's no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit report?it's just another method of gathering information and seeking verification of the accuracy of the report. If disputes are successful, the credit bureaus may remove the negative item.

Does the 609 letter really work? If your argument is valid, the credit agency will delete the item from your credit report. However, if the credit agency can provide you with information that proves the item recorded is accurate, it will not be removed from your credit report.