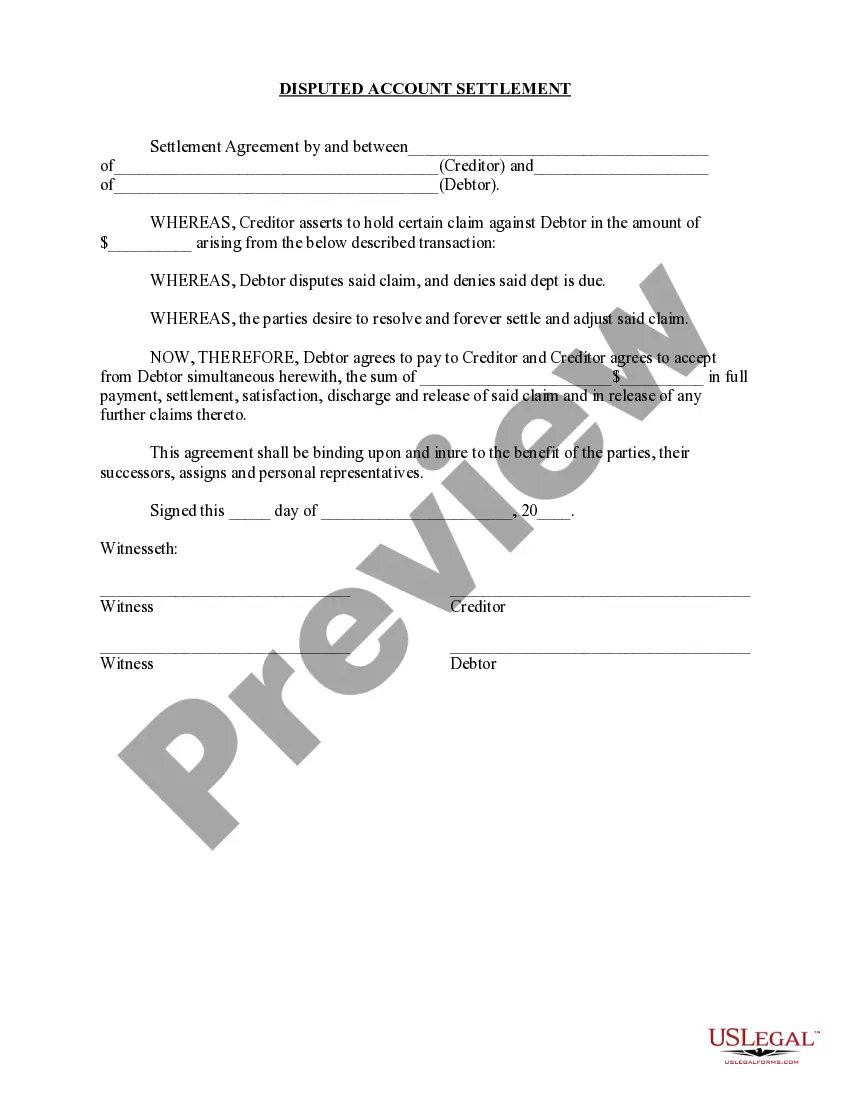

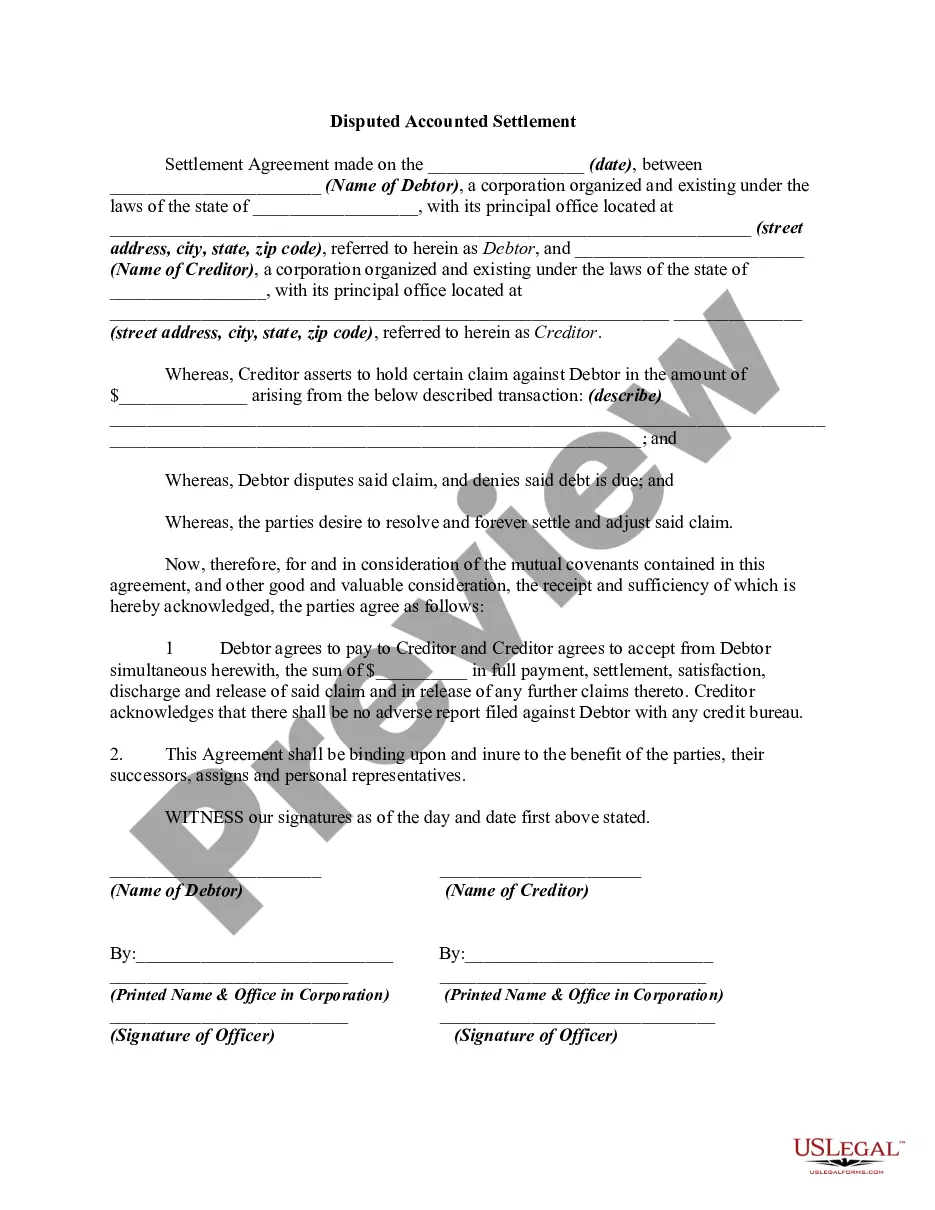

Disputed Accounted Settlement

Understanding this form

The Disputed Account Settlement form is a legal document used to formally settle a disagreement between a debtor and creditor regarding a claimed debt. Through this agreement, both parties acknowledge a bona fide dispute and agree to a mutually acceptable resolution. This form ensures that the original obligation is discharged once the settlement is performed, distinguishing it from mere debt acknowledgment. It is essential for parties who wish to resolve financial disputes without extending the conflict further.

Main sections of this form

- Date of the agreement

- Name and details of the debtor and creditor

- Description of the disputed claim

- Amount being settled

- Agreement on no adverse credit reporting

- Signatures of the parties involved and acknowledgment by a notary

When to use this form

This form is used when a debtor wishes to settle a claim made by a creditor that they dispute. Common scenarios include disagreements over the amount owed, service quality issues, or disputes arising from contracts. This settlement method benefits both parties by reducing potential litigation costs and clearing up financial misunderstandings.

Who this form is for

- Debtors who are disputing a claim from a creditor

- Creditors seeking a formal resolution to outstanding claims

- Businesses and individuals involved in financial transactions with unresolved debts

- Legal and financial representatives advising clients on debt settlements

Completing this form step by step

- Identify and enter the date of the settlement agreement.

- Fill in the names and addresses of both the debtor and the creditor.

- Describe the details of the disputed claim clearly.

- Specify the amount agreed upon for settlement.

- Obtain signatures from both the debtor and creditor, along with printed names and titles.

- Have the document notarized if required by local law.

Is notarization required?

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately describe the disputed claim.

- Neglecting to include required signatures from all parties.

- Not having the document notarized when local laws require it.

- Leaving out the acknowledgment of no adverse credit reporting.

Benefits of using this form online

- Easy access to downloadable templates drafted by licensed attorneys.

- The ability to edit and customize the form to fit specific needs.

- Convenience of completing the form at your pace and convenience.

- Secure storage of your completed forms online for future reference.

Looking for another form?

Form popularity

FAQ

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

1) Write the name and account number of the creditor in question under the Item in Dispute section. 2) Write in the reason for your dispute in the Reason for Dispute section. 3) Sign and mail to the appropriate credit bureau. Mail/call the appropriate credit bureau.

Credit scores can be affected by outstanding debt, even if it no longer exists. Navigating debt negotiations can be tricky, especially if you settled with a company for less than you owe. But a company can and will remove a settled debt from your credit history, if you know how to ask.

Dispute the error with the credit bureau. Report the collections account and ask to have it removed from your credit report. 2feff Provide copies of any evidence you have proving the debt doesn't belong to you. Even if the debt belongs to you, that doesn't mean the collector is legally able to collect from you.

If you believe any account information is incorrect, you should dispute the information to have it either removed or corrected. If, for example, you have a collection or multiple collections appearing on your credit reports and those debts do not belong to you, you can dispute them and have them removed.

Payments reported late that were actually on time. Accounts that aren't yours. Inaccurate credit limit/loan amount or account balance. Inaccurate creditor. Inaccurate account status, for example, an account status reported as past due when the account is actually current.

The Federal Trade Commission advises that you be as specific as possible in the letter about the reason why you think you do not owe this debt (or owe all of it, if you're disputing the amount), but you should give as little personal information as possible in the letter.

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

Your letter should identify each item you dispute, state the facts and explain why you dispute the information, and ask that the information provider take action to have it removed or corrected. You may want to enclose a copy of your report with the item(s) in question circled.