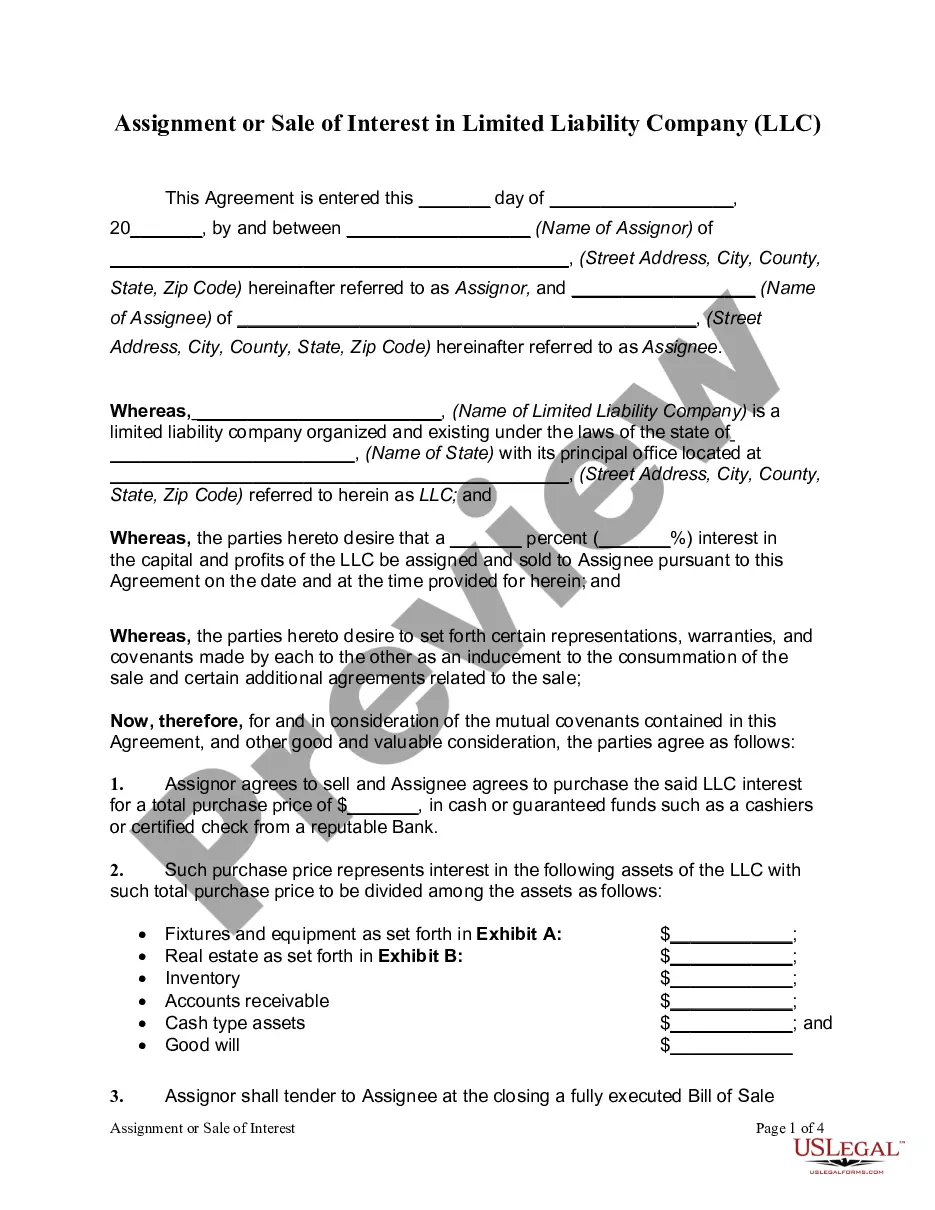

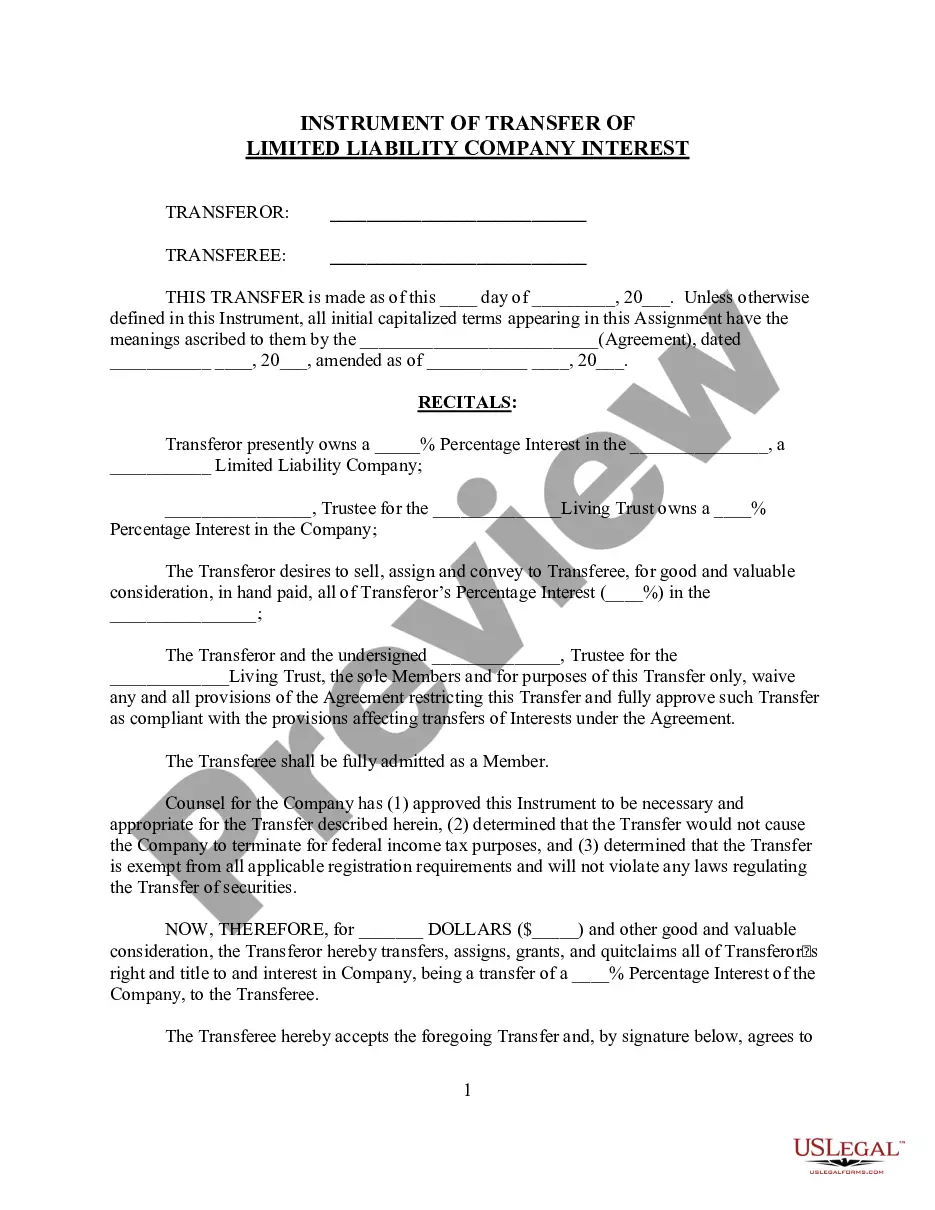

Llc Transfer Of Interest Form With Negative Capital Account

Description

How to fill out Assignment Of Member Interest In Limited Liability Company - LLC?

Regardless of whether for commercial aims or personal matters, everyone must handle legal scenarios at some point in their lives.

Filling out legal documents requires meticulous attention, starting with choosing the correct form template.

With an extensive catalog from US Legal Forms at your disposal, you don't have to waste time searching for the appropriate template online. Take advantage of the library’s user-friendly navigation to find the correct template for any occasion.

- For instance, selecting an incorrect version of the LLC Transfer of Interest Form With Negative Capital Account will result in its rejection upon submission.

- Thus, it is crucial to have a trustworthy source of legal documents like US Legal Forms.

- If you require a sample of the LLC Transfer of Interest Form With Negative Capital Account, follow these straightforward steps.

- Search for the template you need by using the search bar or catalog browsing.

- Review the form’s description to confirm it corresponds with your situation, state, and area.

- Click on the form’s preview to inspect it.

- If it is the wrong form, return to the search feature to find the LLC Transfer of Interest Form With Negative Capital Account sample you require.

- Obtain the document if it fulfills your criteria.

- If you possess a US Legal Forms account, simply click Log in to access previously saved templates in My documents.

- If you do not yet have an account, you can acquire the form by clicking Buy now.

- Choose the appropriate pricing option.

- Fill out the profile registration form.

- Select your payment method: you can utilize a credit card or PayPal account.

- Pick the file format you wish and download the LLC Transfer of Interest Form With Negative Capital Account.

- Once it is saved, you can complete the form with the assistance of editing applications or print it out and finish it manually.

Form popularity

FAQ

Different business actions have varying effects on their members' capital account balances. Sometimes, these balances can be negative. If the LLC's losses plus expenses add up to more than the balances of the capital accounts, those accounts will likely be in the negative.

The tax implications depend a great deal on the ending capital account that is reflected on the K-1. If the capital account is negative, then there is recapture tax associated with a sale. In most circumstances, we can provide an amount in terms of an offering price that will more than cover these associated taxes.

However, a partner's capital account can be negative. This generally happens when the partnership allocates losses or receives a distribution funded by debt incurred by the partnership. These actions can result in a taxable event for partners, so proactive steps need to be taken to avoid a negative balance.

A negative capital account balance indicates a predominantly outward money flow from a country to other countries. The implication of a negative capital account balance is that ownership of assets in foreign countries is increasing.

If a partnership is liquidated where a partner has a negative capital account, the partner with the negative capital account is expected to pay back the amount owed to the partnership within 90 days of the partnership termination or by the end of the year, whichever comes first.