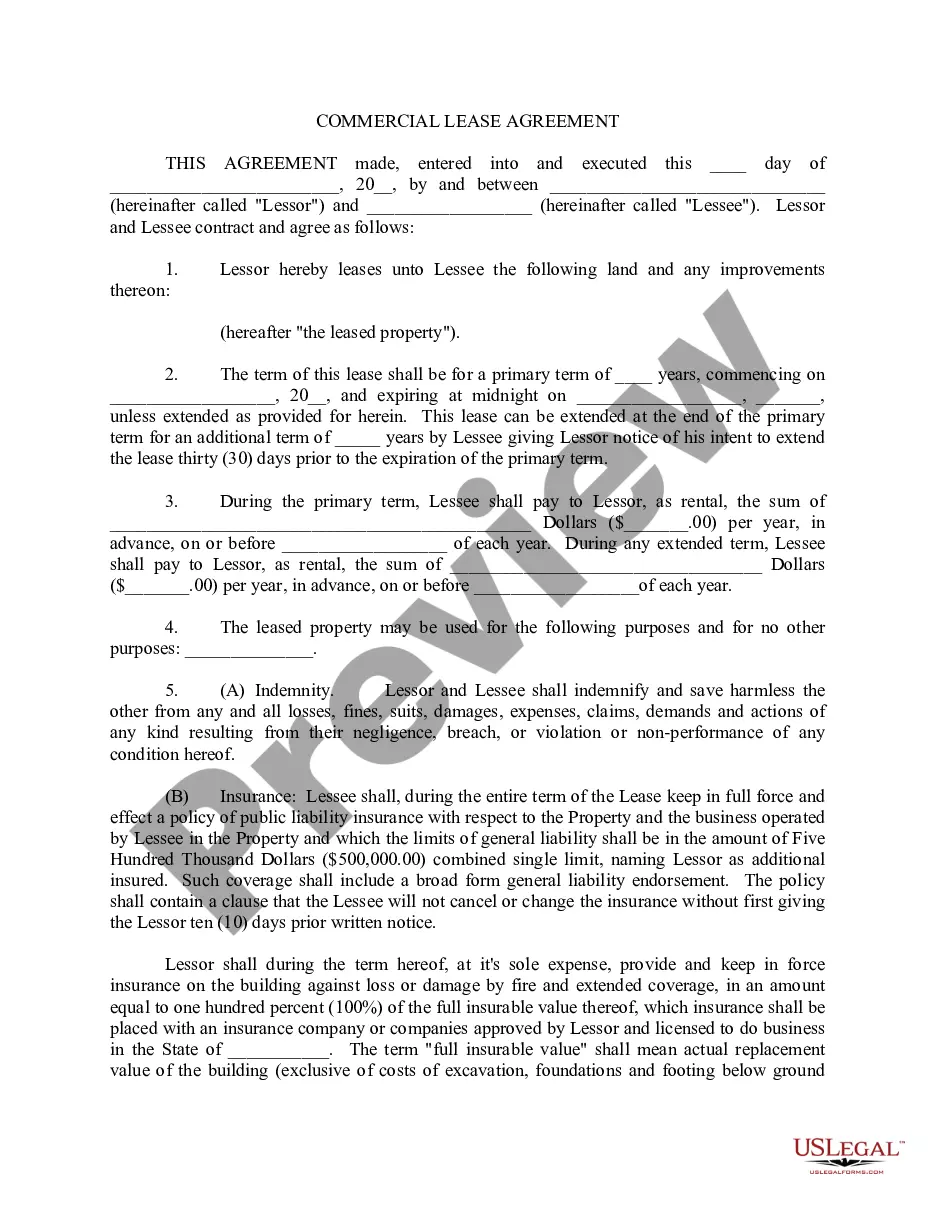

Lease Incentive Vs Tenant Improvement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Tenant Improvement Lease?

Finding a reliable source for the latest and pertinent legal documents is a significant part of navigating bureaucracy.

Identifying the appropriate legal forms necessitates precision and meticulousness, which is why it is crucial to obtain samples of Lease Incentive Vs Tenant Improvement solely from dependable providers, such as US Legal Forms. An incorrect template will squander your time and prolong the issue at hand. With US Legal Forms, you have minimal concerns. You can access and review all the information regarding the document’s applicability and significance for your situation and in your state or area.

Once you possess the form on your device, you can alter it using the editor or print it and fill it out manually. Eliminate the stress associated with your legal documentation. Explore the extensive US Legal Forms catalog where you can discover legal templates, verify their relevance to your needs, and download them immediately.

- Use the catalog navigation or search box to locate your template.

- Review the form’s details to ensure it meets the requirements of your state and area.

- View the form preview, if available, to confirm that it is the one you need.

- Return to the search and find the correct template if the Lease Incentive Vs Tenant Improvement does not satisfy your needs.

- Once you are confident about the form’s relevance, download it.

- If you are a registered user, click Log in to verify and access your selected templates in My documents.

- If you do not yet have an account, click Buy now to obtain the template.

- Choose the pricing plan that aligns with your preferences.

- Proceed to the registration to complete your transaction.

- Finalize your transaction by selecting a payment method (credit card or PayPal).

- Choose the document format for downloading Lease Incentive Vs Tenant Improvement.

Form popularity

FAQ

Accounting Considerations under ASC 842 The standard requires the proper identification and classification of lease incentives within the lease agreement. Lease incentives should be measured and recognized separately from other components of the lease, ensuring transparency and compliance with the accounting standard.

Lease Incentive: That number represents the lessee's lease liability at commencement. The present value calculation is the first step in accounting for lease incentives. To note, this calculation looks at the future payment of the lease asset at the lease inception.

Under ASC 842, tenant improvements (lease incentives) should be recorded as a reduction of fixed payments and, in turn, reduce the Right of Use asset from the time it is capitalized at lease commencement.

Leasehold improvement allowances qualify as Lease Incentives if the assets obtained through the allowance are considered to be owned by the lessee. Leasehold improvements qualify as Lease Incentives if: Lessee has discretion on use of cash incentives.

When you pay for leasehold improvements, capitalize them if they exceed the corporate capitalization limit. If not, charge them to expense in the period incurred. If you capitalize these expenditures, then amortize them over the shorter of their useful life or the remaining term of the lease.