Debt Collector Information Withdraw

Description

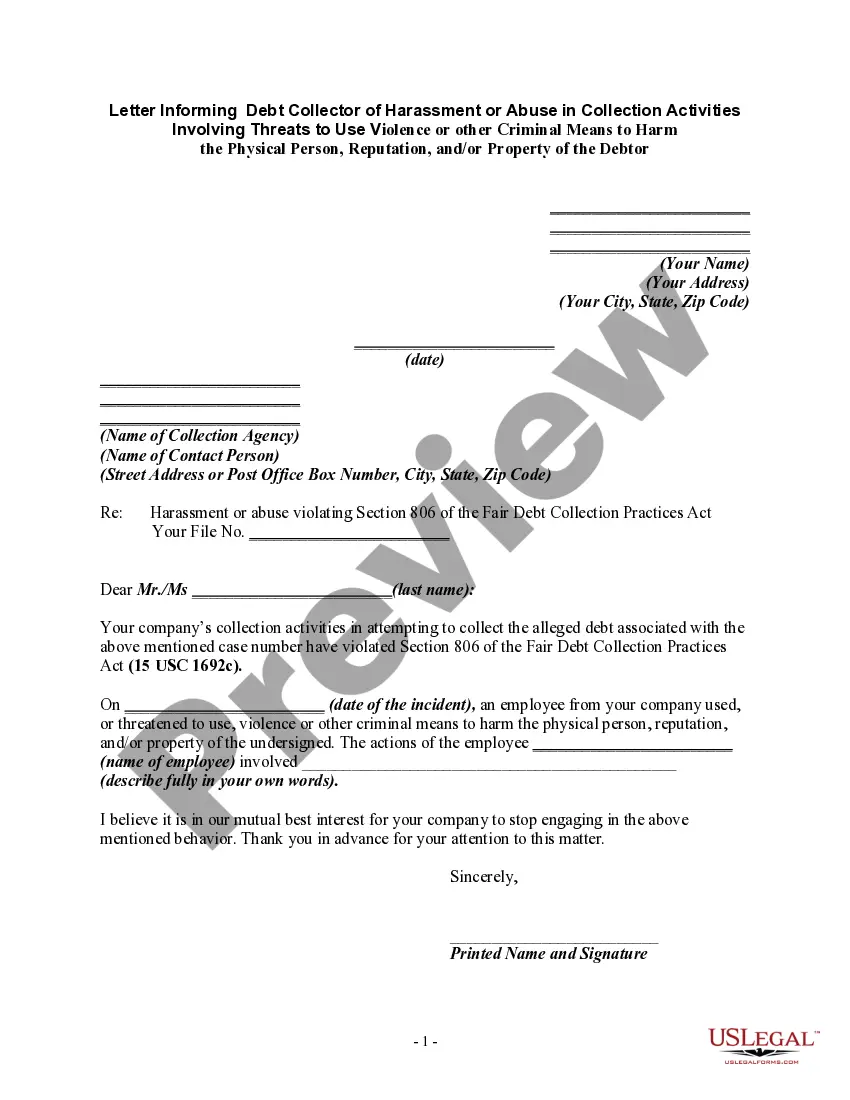

How to fill out Letter Informing Debt Collector Of False Or Misleading Misrepresentations In Collection Activities - Communicating Or Threatening To Communicate To Any Person False Credit Information, Including The Failure To Communicate That A Debt Is Disputed?

Obtaining samples of legal documents that comply with federal and state regulations is essential, and the web provides numerous choices to select from.

However, why squander time looking for the properly drafted Debt Collector Information Withdraw template online when the US Legal Forms digital library already compiles such documents in one location.

US Legal Forms is the largest online legal repository with more than 85,000 fillable templates created by attorneys for any professional or personal situation.

Review the template using the Preview option or through the text description to ensure it satisfies your needs.

- They are easy to navigate with all documents organized by state and intended use.

- Our experts stay updated on legislative changes, ensuring that your form is always current and compliant when obtaining a Debt Collector Information Withdraw from our site.

- Acquiring a Debt Collector Information Withdraw is straightforward and rapid for both existing and new users.

- If you possess an account with an active subscription, Log In and download the document sample you need in the appropriate format.

- If you are a newcomer to our website, follow the steps below.

Form popularity

FAQ

This validation information includes the name of the creditor, the amount you owe, and how to dispute the debt. If the debt collector doesn't or can't provide this information, it could be a scam. Never give sensitive financial information to the caller, at least not until you've confirmed they're legitimate.

Can a debt collector access my bank account? Yes, a debt collector can take money that you owe them directly from your bank account, but they have to win a lawsuit first. This is known as garnishing. The debt collector would warn you before they begin a lawsuit.

If you choose not to verify your identity by providing information, like your Social Security number, the debt collector will generally ask you for another form of identification, including: Account number for the debt in question, if you know it. Other contact information, such as your current or previous address.

This is where we get our "7-in-7" concept. You can attempt to contact a consumer about 1 debt 7 times in 7 days. And it's the "1 debt" that's key here. Phone numbers do not matter; how many debts your agency has for the consumer does.

You can write a letter asking the creditor or collector to remove this information as a goodwill deletion. Your goodwill letter doesn't need to have a lot of information or details. Simply identify the debt, and point out that it has been paid and that you'd like them to remove it.