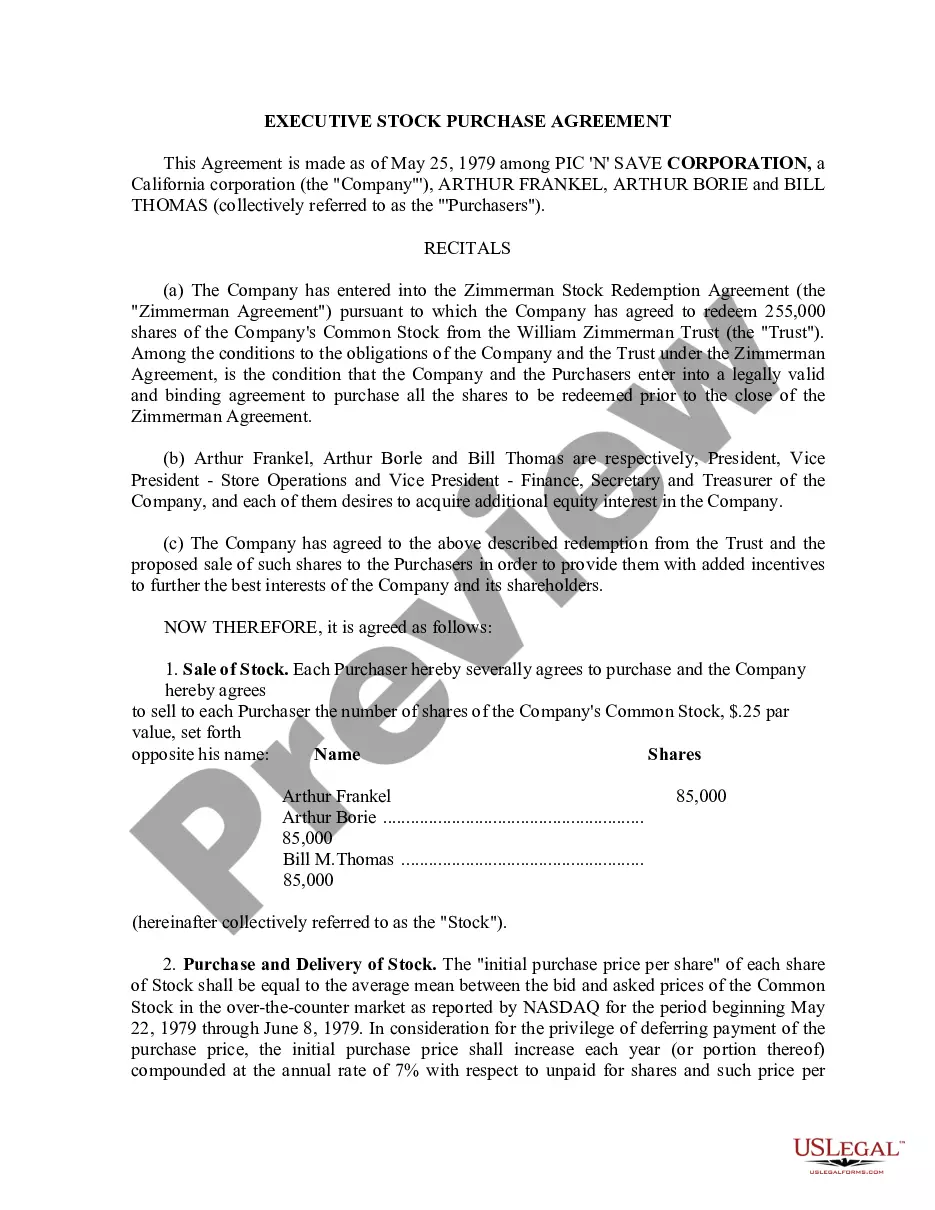

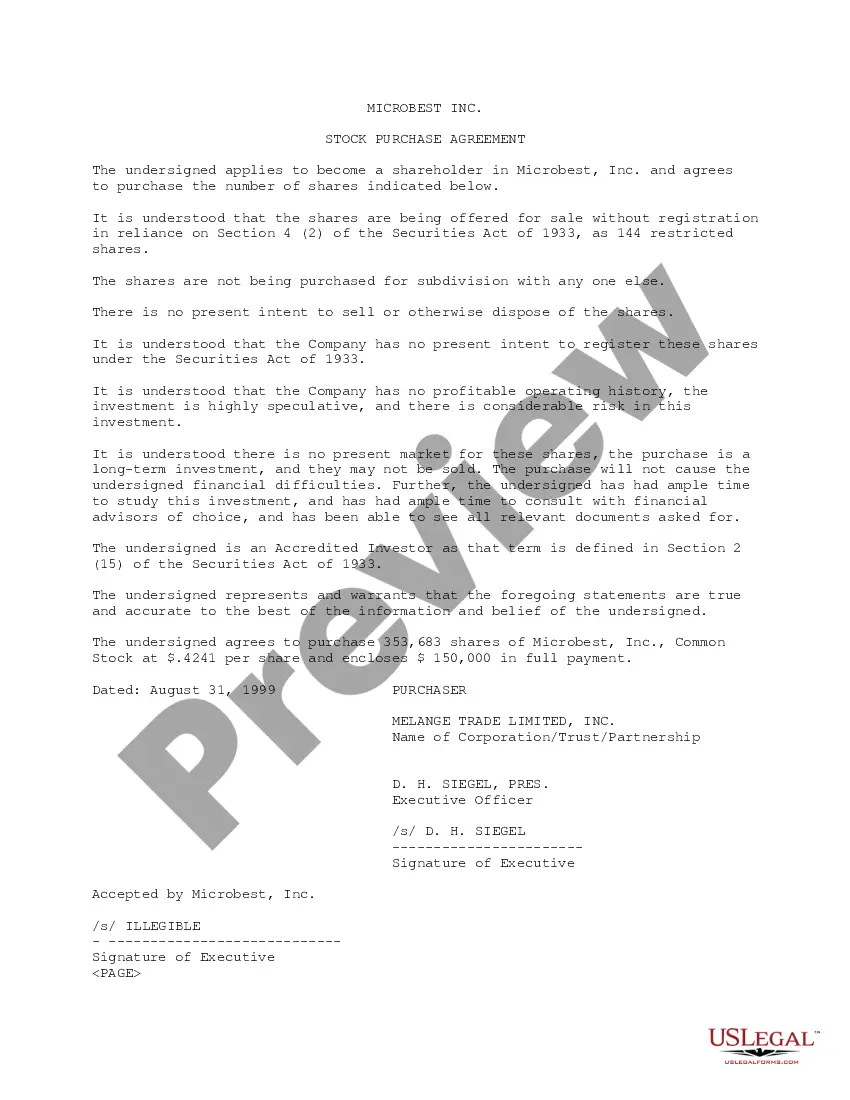

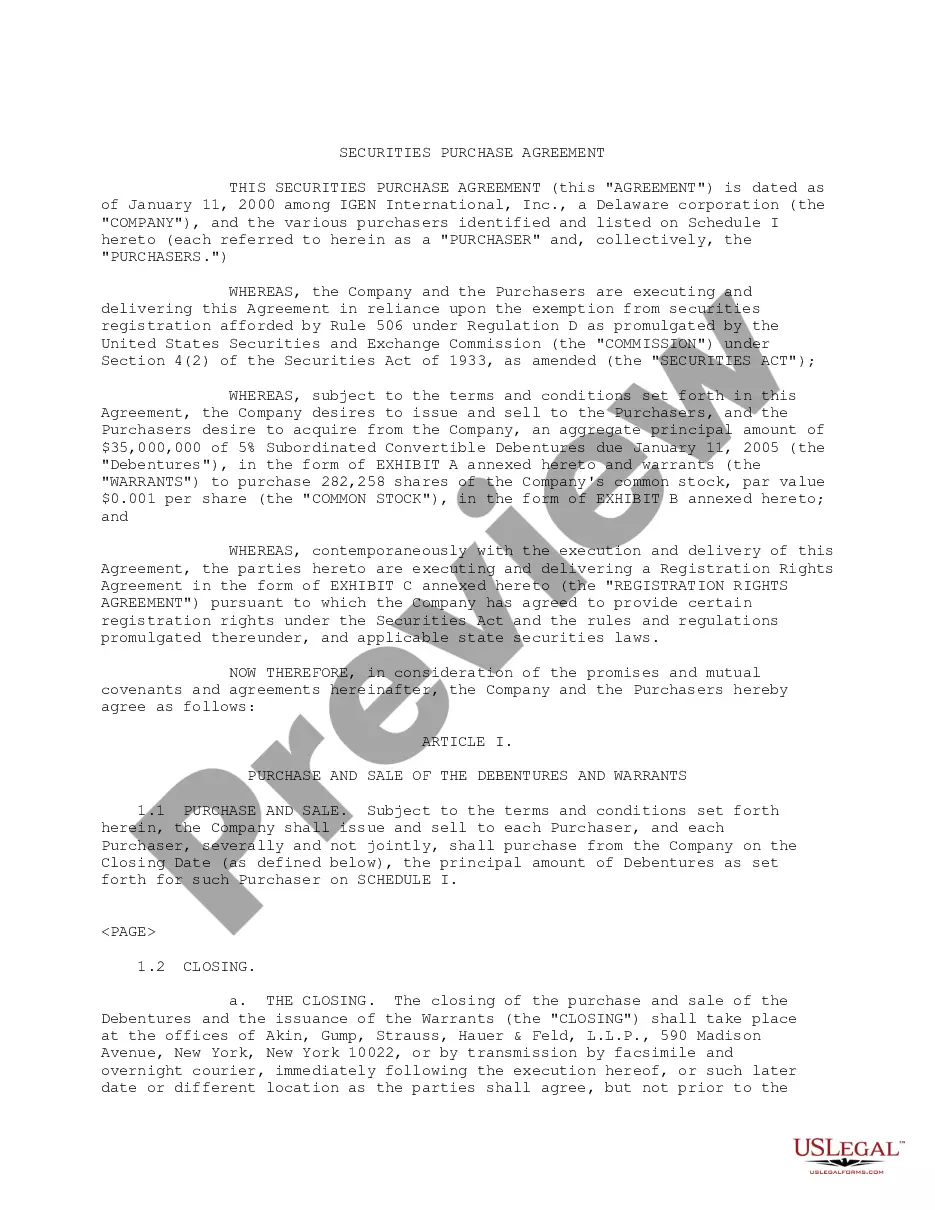

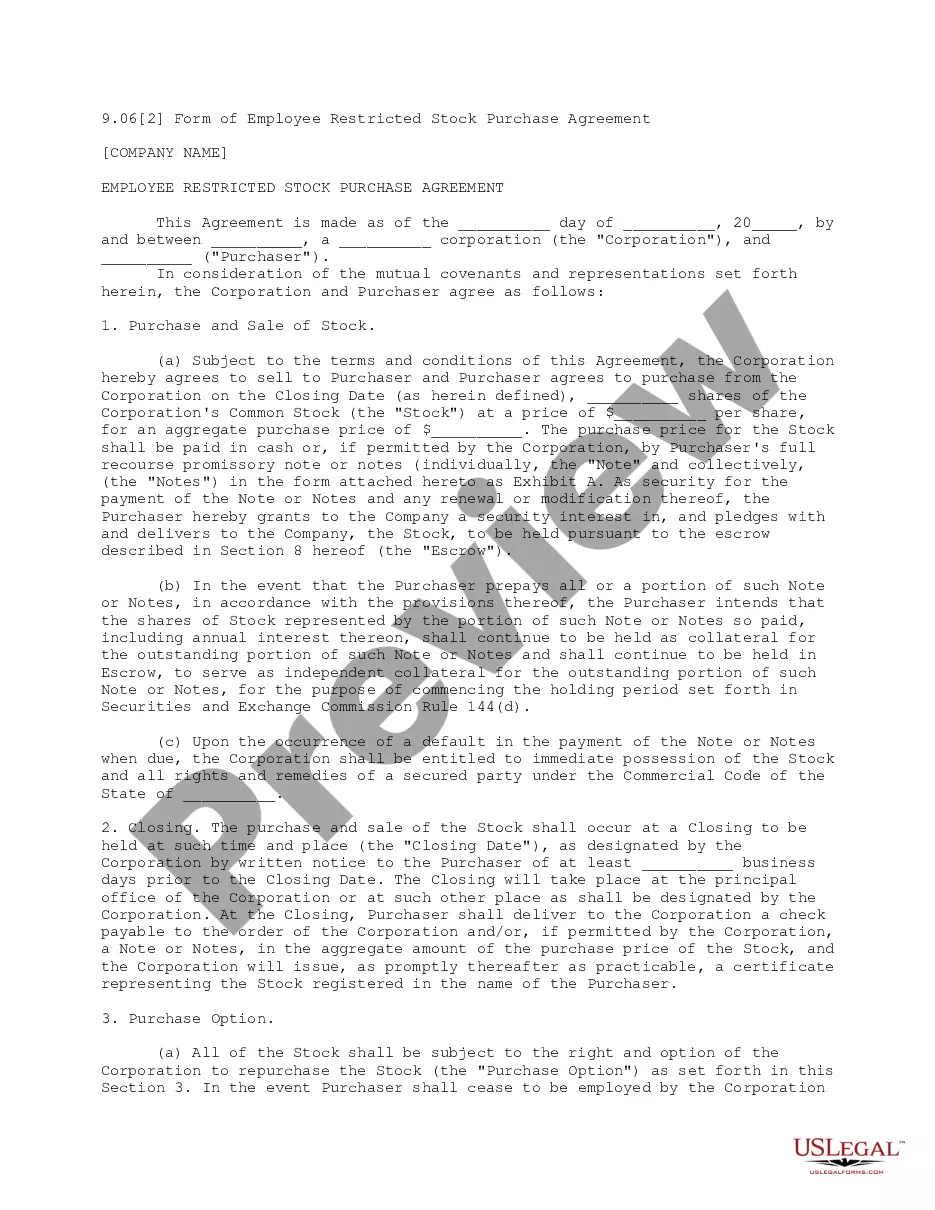

Restricted Stock Between Foreign And Domestic

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Restricted Stock Purchase Agreement Between Intermark, Inc. And Purchasers?

Legal administration can be daunting, even for seasoned experts.

When you're seeking a Restricted Stock Between Foreign And Domestic and lack the opportunity to invest time in finding the correct and updated edition, the processes can be anxiety-inducing.

Access a valuable repository of articles, guides, and manuals related to your circumstances and requirements.

Conserve time and energy searching for the documents you require, and use US Legal Forms’ sophisticated search and Review feature to find Restricted Stock Between Foreign And Domestic and obtain it.

Leverage the US Legal Forms online library, supported by 25 years of expertise and reliability. Transform your daily document management into a seamless and user-friendly procedure today.

- If you have a subscription, Log In to your US Legal Forms profile, search for the form, and obtain it.

- Check your My documents section to see the documents you have previously saved and to manage your folders as needed.

- If this is your first time with US Legal Forms, set up an account and gain unlimited access to all features of the library.

- Here are the steps to follow after acquiring the form you need.

- Verify it is the correct form by previewing it and reviewing its description.

- Make sure that the specimen is recognized in your state or county.

- Select Buy Now when you are ready.

- Choose a subscription plan.

- Select the format you prefer, and Download, fill out, eSign, print, and send your document.

- Utilize state- or county-specific legal and business documents.

- US Legal Forms caters to any needs you may have, from personal to commercial paperwork, all in one platform.

- Employ cutting-edge tools to complete and manage your Restricted Stock Between Foreign And Domestic.

Form popularity

FAQ

Locate Supplemental Tax Documentation Don't rely only on the 1099-B form. Instead, supply proof of the true cost basis of the restricted stock unit so you only pay taxes on what you owe. Some documentation may include the following: Records from your company supporting the vesting date and number of shares.

Accounting for Restricted Stock/RSU Grants The accounting for restricted stock awards can be quite technical. For example, if actual shares are delivered to the employee, then journal entries would impact equity. If the value of the shares is paid in cash, then the company would most likely record a liability.

RSUs are taxed as income to you when they vest. If you sell your shares immediately, there is no capital gain tax, and you only pay ordinary income taxes. If instead, the shares are held beyond the vesting date, any gain (or loss) is taxed as a capital gain (or loss).

RSUs are considered a form of compensation and are included in your taxable income when they vest. Because RSU income is considered supplemental, the withholding rate can vary between 22% and 37%. Usually, your employer will liquidate a percentage of the shares to cover the withholding requirement.

Taxation of RSUs The amount reported will equal the fair market value of the stock on the date of vesting, which is also the date of delivery in this case. Therefore, the value of the stock is reported as ordinary income in the year the stock becomes vested.