Accidental Damage For

Description

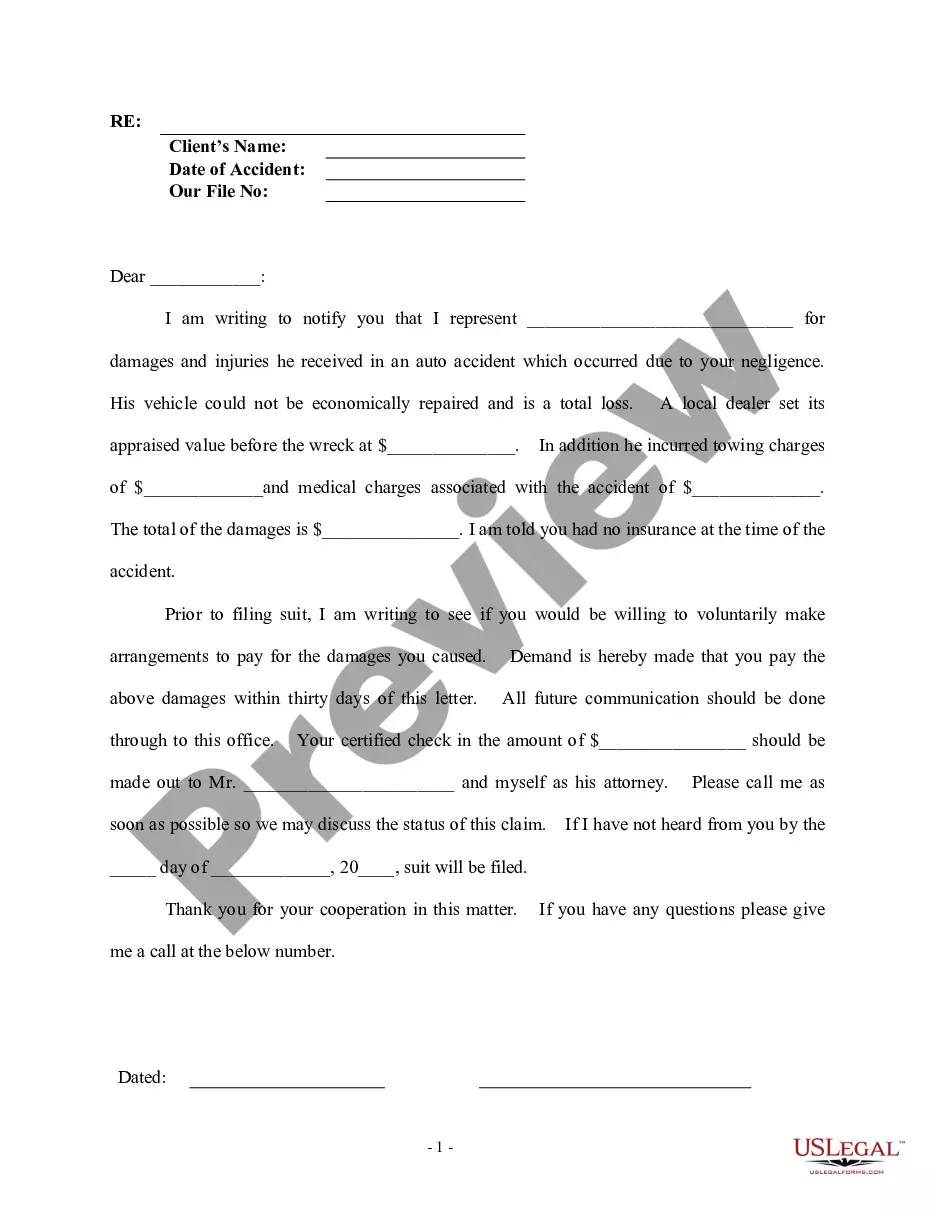

How to fill out Sample Letter For Automobile Accident Demand For Damages To Party Opposite?

Utilizing legal templates that comply with federal and local regulations is crucial, and the internet provides a multitude of choices to select from.

However, what is the purpose of spending time searching for the suitable Accidental Damage For example on the internet if the US Legal Forms online library already possesses such templates consolidated in one place.

US Legal Forms is the largest digital legal repository with over 85,000 fillable templates created by attorneys for any business and life situation.

Review the template using the Preview feature or through the text outline to ensure it meets your requirements.

- They are easy to navigate with all documents categorized by state and intended use.

- Our experts keep abreast of legislative changes, so you can always trust that your form is current and compliant when obtaining an Accidental Damage For from our platform.

- Acquiring an Accidental Damage For is straightforward and quick for both existing and new users.

- If you already have an account with an active subscription, Log In and save the document sample you need in the desired format.

- If you are new to our site, follow the steps below.

Form popularity

FAQ

Claiming for accidental damage can be a smart choice, especially if the costs of repair exceed your deductible. When you experience damage, it’s essential to assess the situation promptly. If the damage significantly impacts your daily life or incurs high repair costs, pursuing a claim can help you recover financially. At US Legal Forms, we provide resources that guide you through the claims process for accidental damage, ensuring you make informed decisions.

Accidental damage for insurance can include unintentional incidents like spills, drops, or impacts that result in physical harm to your property. For example, if you accidentally break a window or spill liquid on your electronics, these incidents typically qualify as accidental damage. Understanding your coverage can help you address unexpected mishaps efficiently. You can use US Legal Forms to explore your options and ensure you have the right protection in place.

Accidental damage for insurance typically excludes injuries or damages resulting from normal wear and tear. Deliberate actions, such as self-inflicted harm or neglect, do not fall under this category. Additionally, damages like rust, mold, or other gradual deterioration are usually not covered. Therefore, it’s essential to understand the specific terms of your policy.

Accidental damage coverage typically includes items such as computers, mobile devices, and appliances that suffer unforeseen harm. Additionally, it can cover damage to your home's interior, like broken tiles or stained carpets, under specific circumstances. Many policies will explain any exclusions or limitations that apply, so taking the time to familiarize yourself with the details is beneficial. For a clearer understanding of what your plan includes, consider utilizing tools available through uslegalforms.

Accidental damage for insurance policies generally covers the costs associated with repairing or replacing damaged items caused by unintended incidents. This protection usually extends to items like electronics, furniture, and certain structural aspects of your home. However, coverage specifics can vary among policies, so it is vital to read the terms carefully. Resources, such as uslegalforms, can assist you in understanding these nuances to ensure appropriate coverage.

Accidental damage means any unintentional harm done to your property that occurs suddenly and unexpectedly. This can encompass a wide range of incidents, such as cracking a phone screen or damaging a wall during a home improvement project. It is essential to distinguish this from intentional damage or general wear, as these do not typically qualify for coverage. Thus, knowing the specifics can help you assess your protection effectively.

An example of an accidental damage claim could involve a scenario where someone accidentally spills coffee on their laptop, causing it to malfunction. In this case, the individual may file a claim to receive compensation for repairs or replacement. Such claims are crucial, as they can provide significant financial relief when you face unexpected mishaps. When exploring this further, remember that uslegalforms can guide you through filing your claim effectively.

Accidental damage for insurance purposes refers to unexpected and unintended harm caused to your property or belongings. This includes incidents like dropping a device, spilling liquid on electronics, or breaking a piece of furniture. To qualify, the damage must not result from neglect or wear and tear, but rather from an unforeseen event. Understanding this distinction can help you determine whether your situation is eligible for a claim.