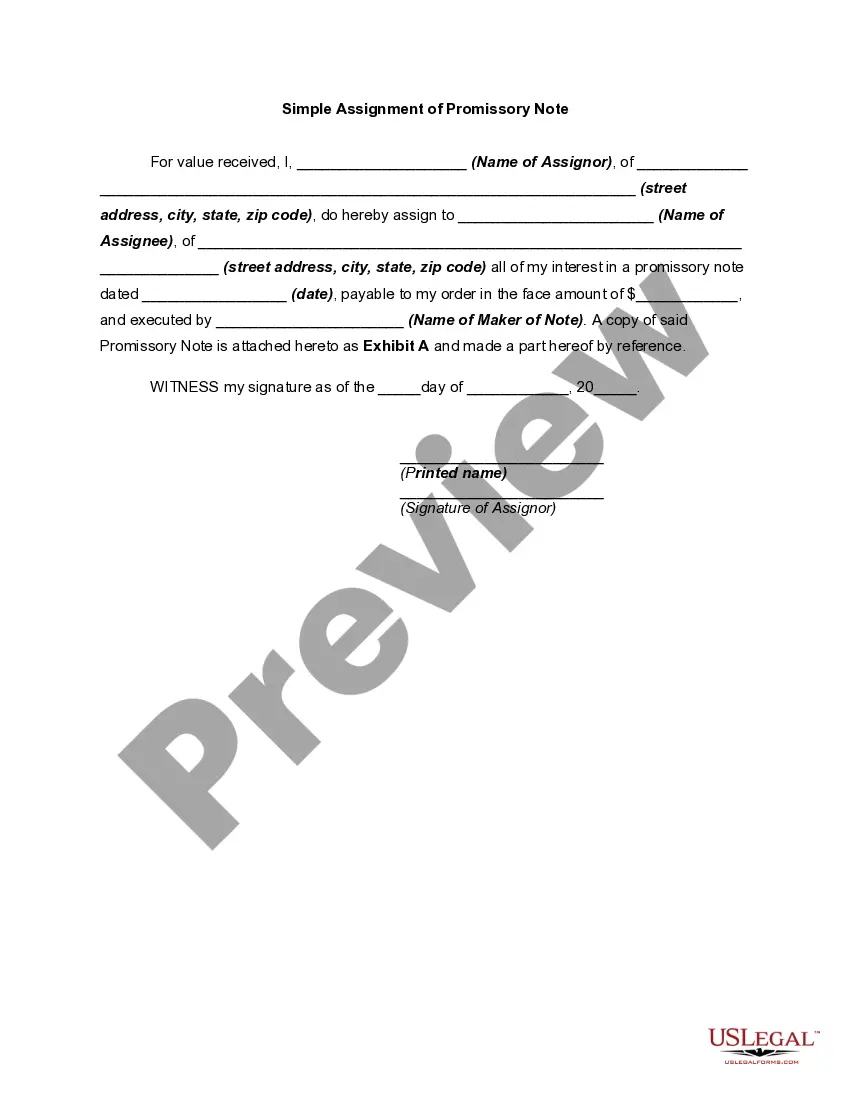

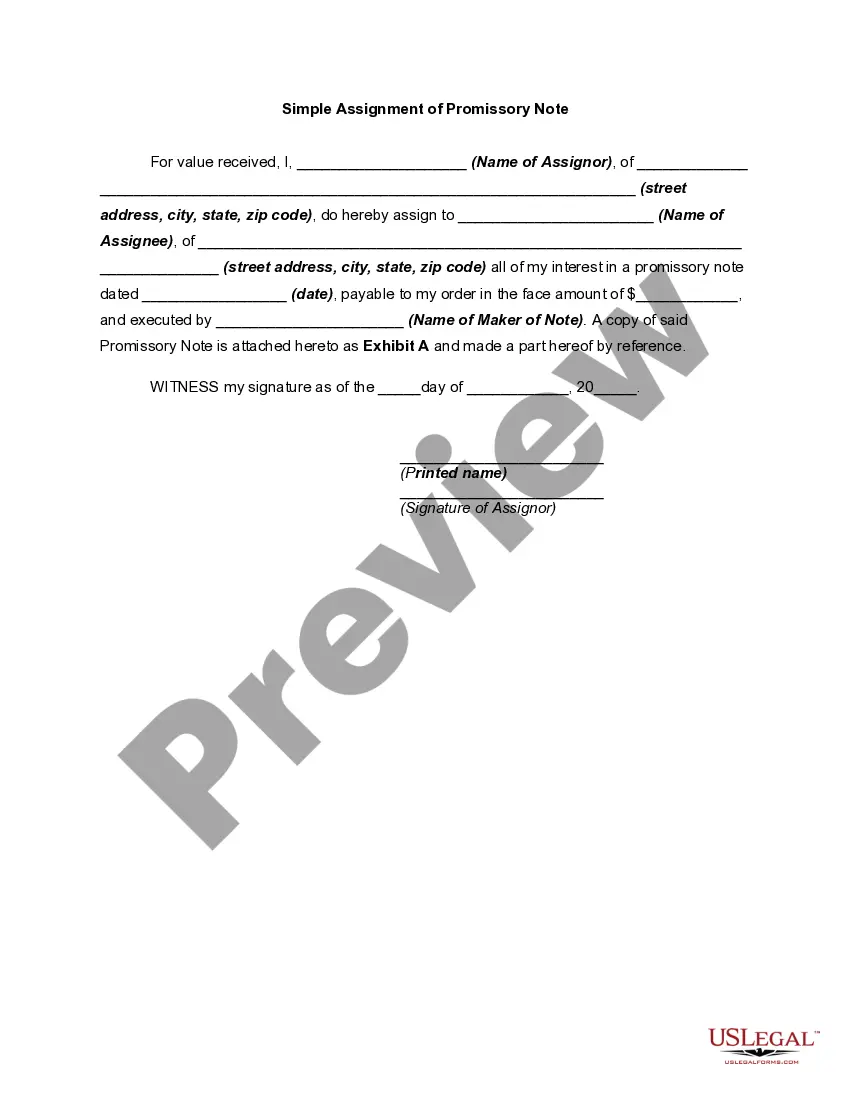

Sell Business Promissory Note With Collateral

Description

How to fill out Sale Of Business - Promissory Note - Asset Purchase Transaction?

Whether for commercial purposes or personal matters, everyone must handle legal issues at some point in their life. Completing legal documents necessitates careful consideration, starting from selecting the correct form template. For example, if you choose an incorrect version of a Sell Business Promissory Note With Collateral, it will be denied once submitted. Thus, it is crucial to have a reliable source of legal documents such as US Legal Forms.

If you need to obtain a Sell Business Promissory Note With Collateral template, follow these simple steps.

With a comprehensive US Legal Forms catalog available, you do not have to waste time searching for the appropriate template online. Utilize the library’s easy navigation to find the right template for any situation.

- Search for the template you require using the search bar or catalog browsing.

- Review the form’s description to confirm it aligns with your circumstances, state, and area.

- Click on the form’s preview to inspect it.

- If it is the wrong document, return to the search function to locate the Sell Business Promissory Note With Collateral template you need.

- Download the template if it meets your specifications.

- If you possess a US Legal Forms account, simply click Log in to access previously saved documents in My documents.

- If you do not yet have an account, you can acquire the form by clicking Buy now.

- Select the suitable pricing option.

- Fill out the account registration form.

- Choose your payment method: use a credit card or PayPal account.

- Select the file format you prefer and download the Sell Business Promissory Note With Collateral.

- Once saved, you can complete the form using editing software or print it out and fill it in manually.

Form popularity

FAQ

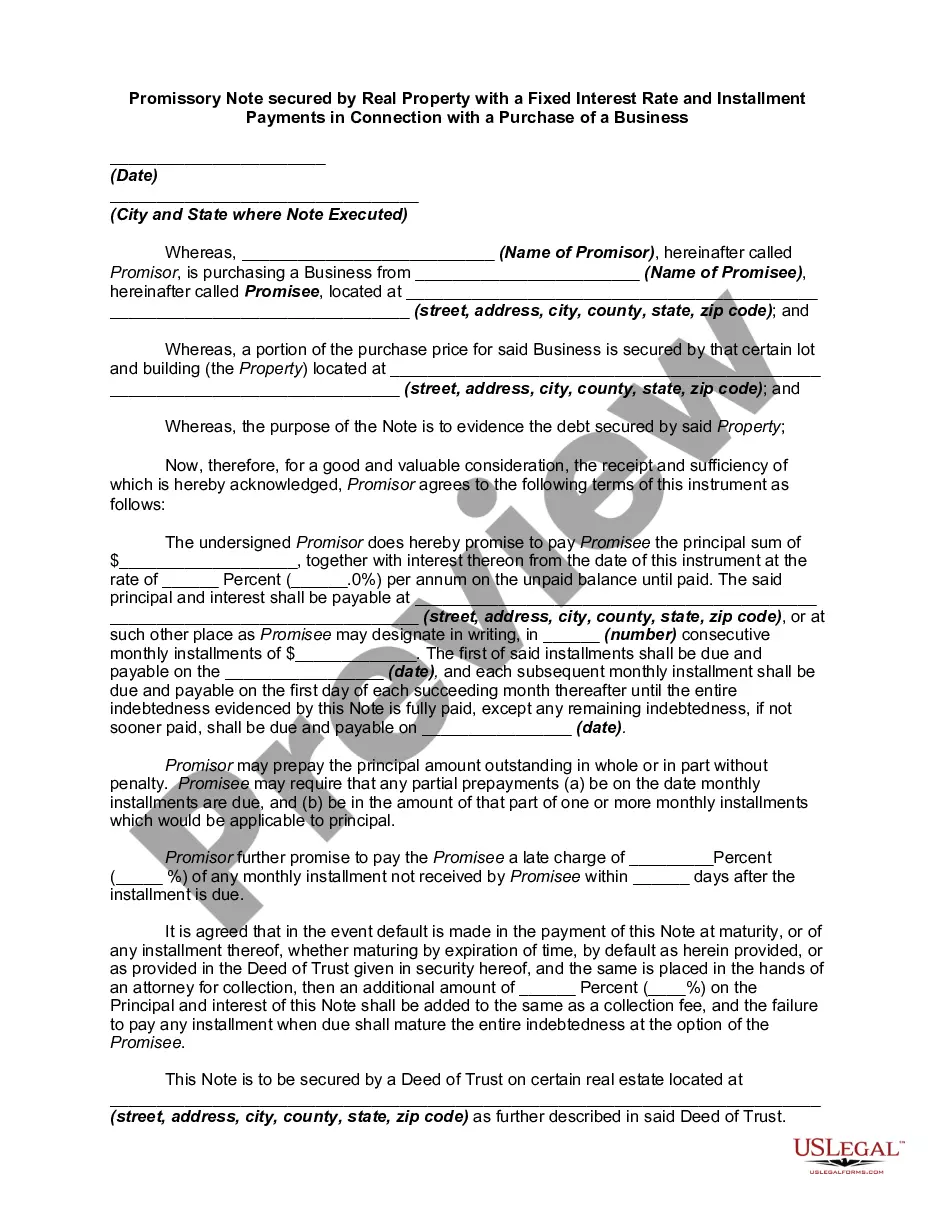

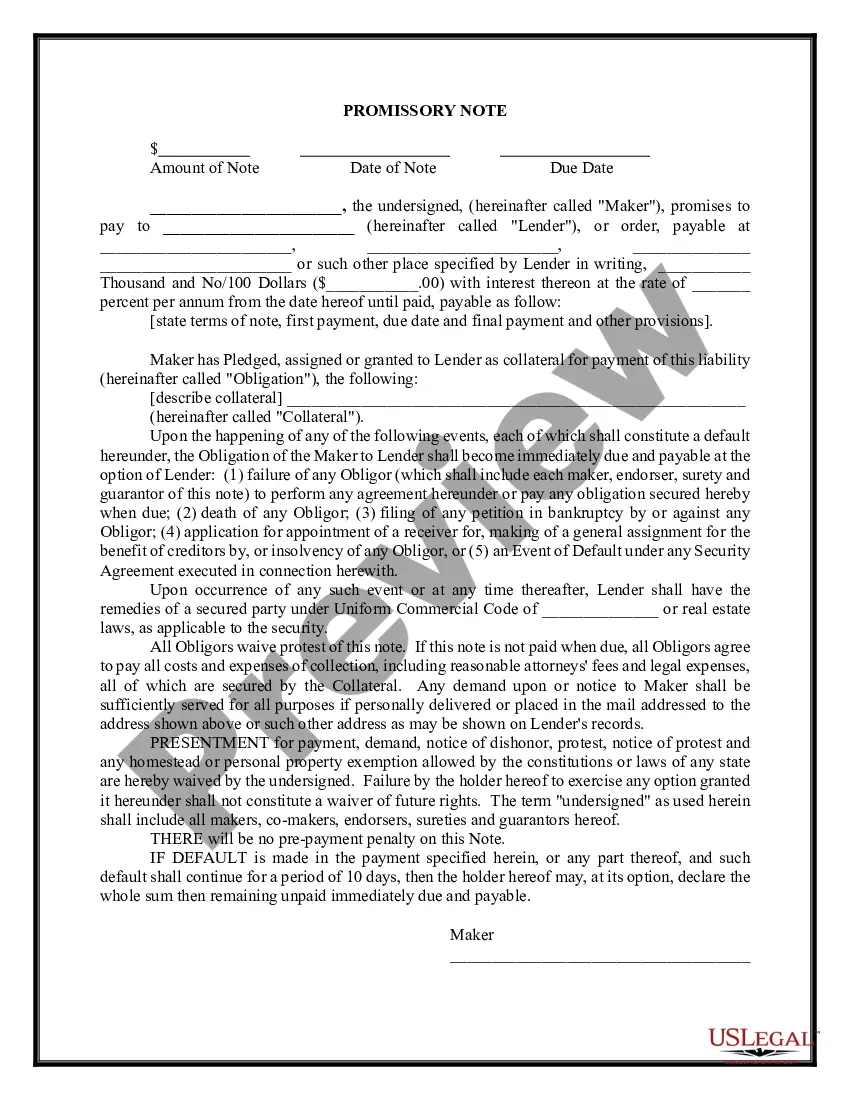

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner didn't make their loan payments. Your lender will keep the original promissory note until your loan is paid off.

The note can include specific details such as the borrower and lender's identities, the loan amount, interest rate, repayment terms, maturity date, and collateral (if any). There are two main categories of promissory notes: secured (with collateral) and unsecured (without collateral).

There are three main options for selling a promissory note: to an individual, to a family member, or to a note-buying company. A note-buying company will offer you a partial or full purchase of the remaining balance on loan. The entire process of selling a promissory note can take 15 to 35 days.

A Secured Promissory Note is a legal agreement that requires a borrower to provide security for a loan. With this lending document, the borrower puts forth their personal property or real estate as collateral if the loan isn't repaid.