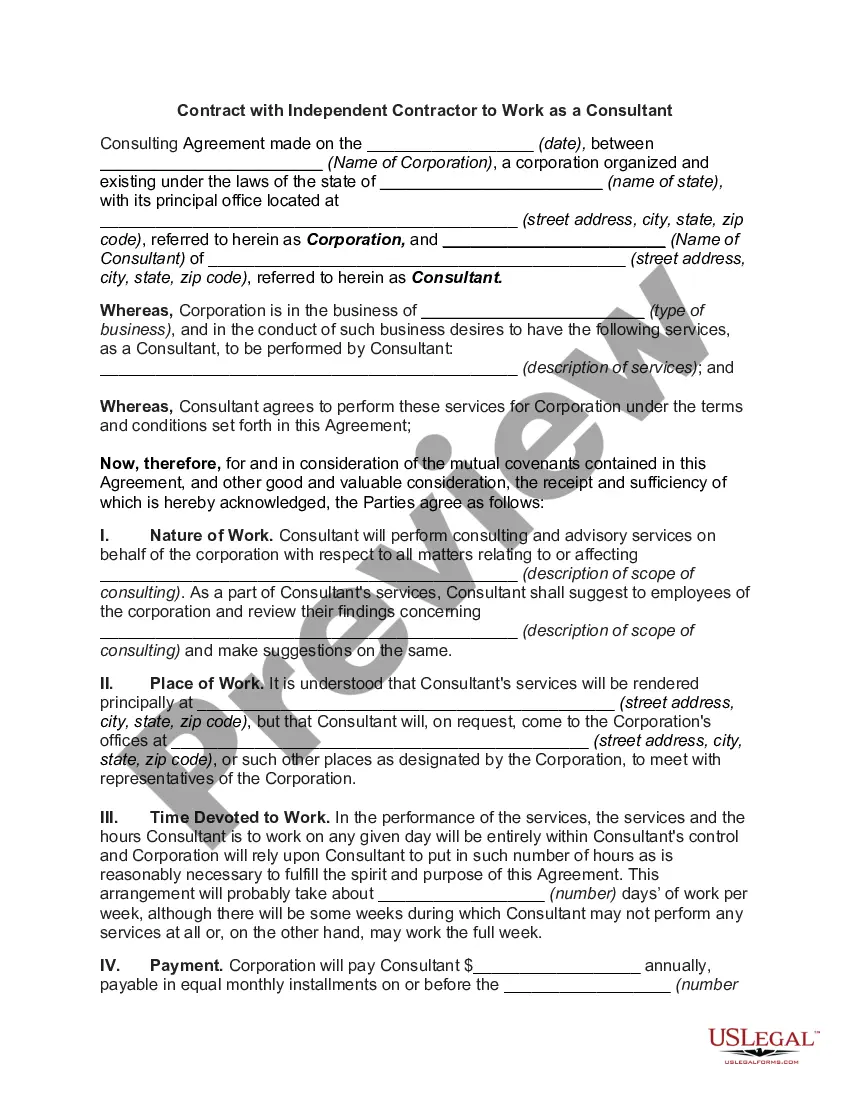

Consultant Contract Under Withholding In Minnesota

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Most professional services are not taxable.

You may claim exempt from Minnesota withholding if at least one of these apply: You meet the requirements and claim exempt from federal withholding. You had no Minnesota income tax liability last year, received a refund of all Minnesota income tax withheld, and do not expect to owe state income tax this year.

Option 1 – Default Tax Withholding Minnesota State - 6.25% (MN residents only. If you are a non-Minnesota resident, contact your state for tax withholding requirements.).

Furthermore, services are not taxable unless specifically included by law. Examples of taxable services include lodging, laundry and cleaning services, pet grooming, lawn care, digital downloads, and telecommunications. A remote seller is a retailer that does not have a physical presence in the state.

It is illegal for an employer to classify a worker as an independent contractor if the worker qualifies as an employee. An employer also cannot make a worker an independent contractor by having workers to sign a contract saying that they are independent contractors, when in reality they are employees.

Most professional services are not taxable. However, sales of some products may be taxable.

Items Exempt by Law Common examples include: Clothing for general use, see Clothing. Food (grocery items), see Food and Food Ingredients. Prescription and over-the-counter drugs for humans, see Drugs.

You may claim exempt from Minnesota withholding if at least one of these apply: You meet the requirements and claim exempt from federal withholding. You had no Minnesota income tax liability last year, received a refund of all Minnesota income tax withheld, and do not expect to owe state income tax this year.

Sign up for an e-Services account online using your Federal Employer ID Number. Log in to your e-Services account and register your business for withholding tax. Upon receipt, provide your withholding tax account ID to your payroll provider.

If you claim exempt from Minnesota withholding, complete only Section 2 of Form W-4MN and sign and date the form to validate it.