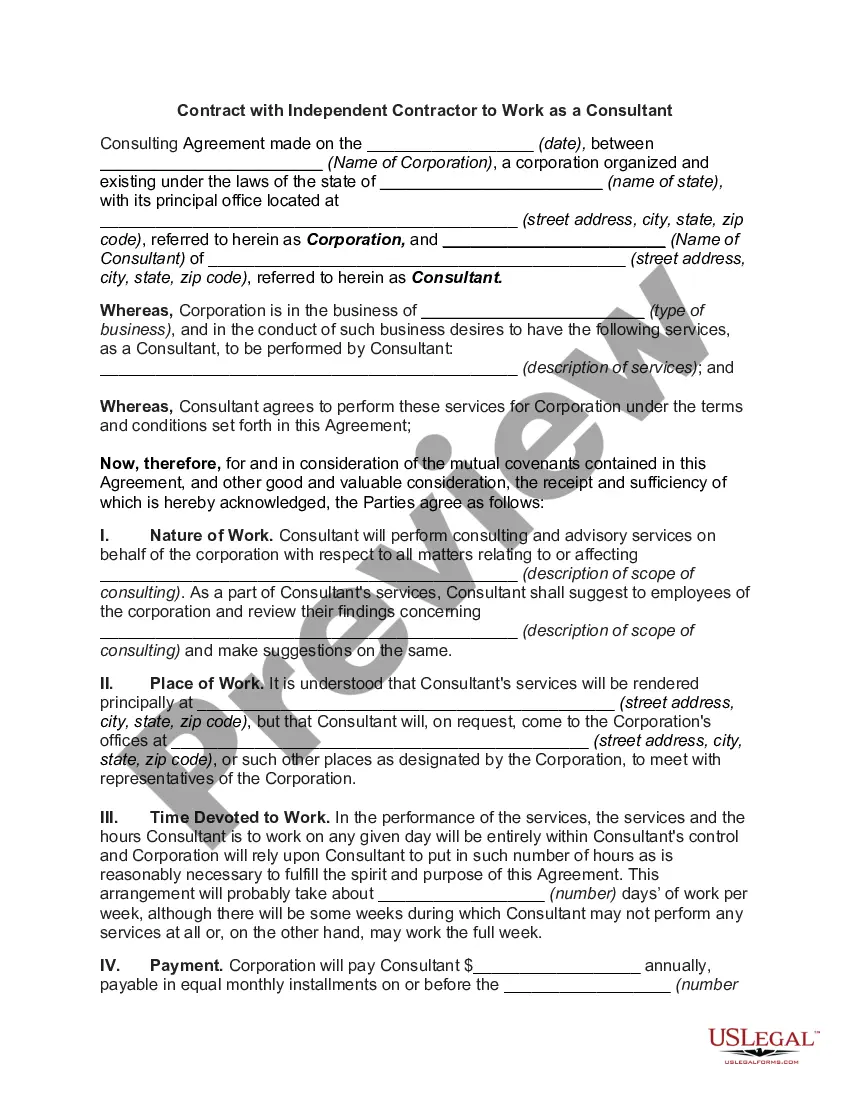

Consultant Work Contract For Taxes In Allegheny

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Pennsylvania personal income tax is levied at the rate of 3.07 percent against taxable income of resident and nonresident individuals, estates, trusts, partnerships, S corporations, business trusts and limited liability companies not federally taxed as corporations.

There is no specific threshold for reporting 1099s with the state of Pennsylvania. Instead, the reporting requirements align with the federal guidelines. The payer should assess and file a Form 1099 based on the applicable federal threshold for each specific form.

What is the tax rate for self-employment? The self-employment tax rate in 2024 is 15.3%.

Most consultants receive 1099 forms because they work for multiple companies, while an in-house consultant would receive a W-2.

A person who is required to file a Federal 1099-MISC or 1099-NEC, as referenced above, for a non-resident individual or disregarded entity with a nonresident owner for payments of Pennsylvania source compensation or net profits is required to withhold Pennsylvania Personal Income Tax from such payments.

What is the tax rate for self-employment? The self-employment tax rate in 2024 is 15.3%.

A consultant can operate independently as an individual contractor. You may also hire a consultant who is an employee of a consulting company. Your business must file 1099 forms for either employment scenario since the worker is not your employee.