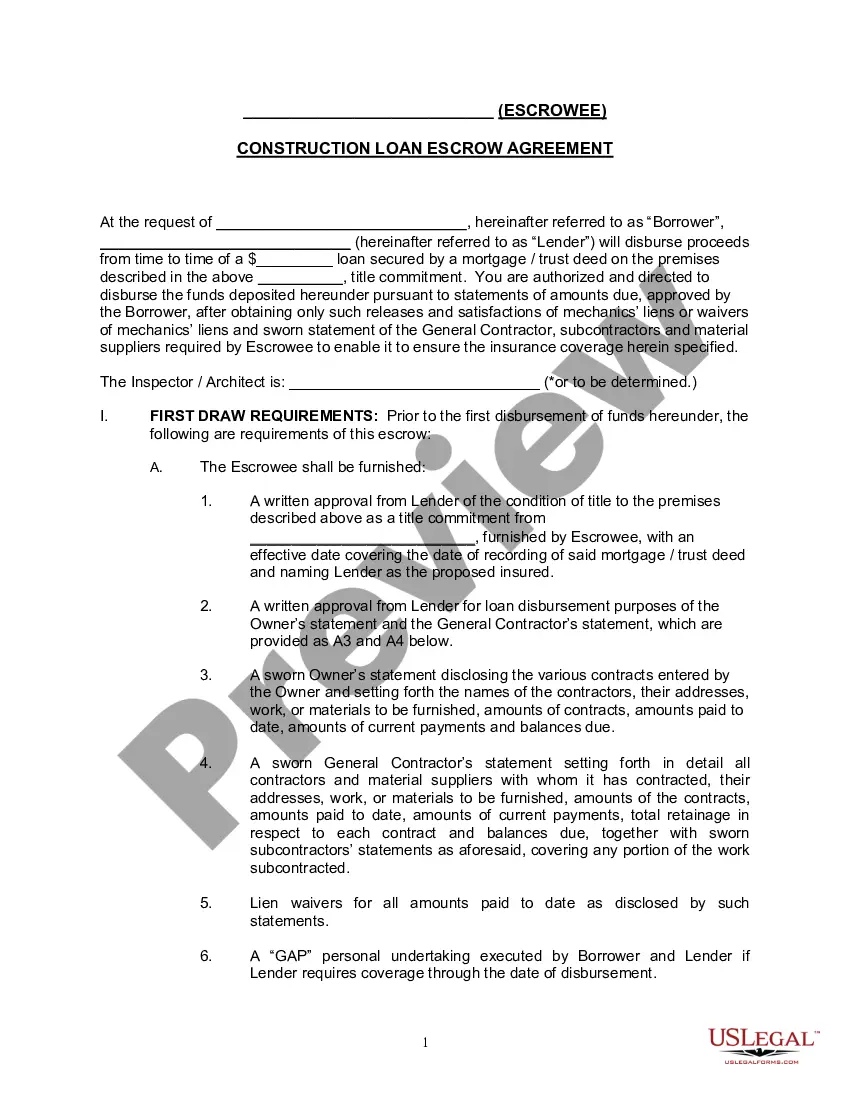

"A construction loan agreement isa legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

A Loan Agreement is a document between a borrower and lender that details the loan repayment schedule.

The Loan Agreement protects the lender by enforcing the borrower's pledge to repay the loan; payment via regular payments or lump sums. The borrower may also find the loan contract useful because it records the details of the loan for their records and helps keep track of payments.

Loan agreements generally include information about:

* The location.

* The loan amount.

* Interest and late fees.

* Repayment method.

* Collateral and insurance."

Wake North Carolina Construction Loan Agreement

Category:

State:

Multi-State

County:

Wake

Control #:

US-ENTREP-0065-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Construction Loan Agreement?

Creating documents, such as the Wake Construction Loan Agreement, to handle your legal affairs is a challenging and lengthy endeavor.

Many situations necessitate the involvement of a lawyer, which further renders this task not especially economical.

Nevertheless, you can take control of your legal matters and manage them independently.

The onboarding experience for new users is equally uncomplicated! Here’s what you should do before obtaining the Wake Construction Loan Agreement.

- US Legal Forms is here to assist you.

- Our platform offers over 85,000 legal templates crafted for various situations and life events.

- We ensure that every document meets the legal requirements of each state, alleviating concerns regarding compliance-related legal issues.

- If you’re already familiar with our site and hold a subscription with US, you understand how simple it is to access the Wake Construction Loan Agreement template.

- Just Log In to your account, download the template, and tailor it to your preferences.

- Have you misplaced your document? No need to fret. You can retrieve it from the My documents section in your account - available on both desktop and mobile.

Form popularity

FAQ

Construction disbursement is the process of slowly releasing the funds for construction projects throughout the entire process. This is a much-preferred way to manage a project instead of writing one large check at the beginning of the construction.

Paying off unsecured liens or construction costs paid by the Borrower outside of the secured Interim Construction Financing is considered cash out to the Borrower, if above $2,000 or 1% of the loan amount, whichever is greater.

Commercial construction loans are typically funded partially at closing to cover previously paid soft and hard costs. After the initial partial funding, loan proceeds are disbursed monthly based on draw requests for costs incurred. These costs are submitted by the developer and verified by the lender.

The disbursement of funds during construction the construction loan is disbursed over the course of the project, reimbursing the costs of every milestone. The funds are released per the details in the Schedule of Values and the Draw Schedule.

If your project goes over budget, you'll need to come up with the difference out of pocket or take out a second loan to cover the overages. For that reason, unless you have a solid grasp of the costs and schedule for the project, a one-time construction loan may not be right for your project.

It's harder to get approved for a construction loan than for a typical purchase mortgage, Moralez and Thomas say. That's because the bank is taking extra risk during the building phase, since there isn't an asset to secure the mortgage. Typical down payments are around 20%.

Take-out loans can be used as a long-term personal loan to pay off previous outstanding balances with other creditors. They are most commonly used in real estate construction to help a borrower replace a short-term construction loan and obtain more-favorable financing terms.

Compare The Best Construction Loan Lenders CompanyStarting Interest RateMinimum Credit ScoreNationwide Home Loans Group Best OverallVaries640FMC Lending Best for Bad Credit ScoreVariesNoneNationwide Home Loans, Inc. Best for First-Time BuyersVariesVariesNormandy Best Online Borrower ExperienceVaries6203 more rows

Construction Loan Requirements To win approval for a construction loan, you may need: Good to excellent credit. To reduce their risk, lenders require borrowers to have a credit score of 680 or higher to qualify for a construction loan. That's just the minimum, as some lenders may require a score of 720 or better.

What Do You Need to Get a Home Construction Loan? Good to excellent credit. Most lenders will require you to have a credit score of 680 or higher. A good debt-to-income (DTI) ratio. Many lenders will accept DTI ratios of up to 45%, but lower is better. Necessary documentation.