Bexar Texas Approval of Incentive Stock Option Plan

Description

How to fill out Approval Of Incentive Stock Option Plan?

Are you seeking to swiftly compose a legally-enforceable Bexar Approval of Incentive Stock Option Plan or potentially any other paperwork to manage your personal or business affairs.

You can choose between two alternatives: employ a specialist to create a legitimate document for you or compose it entirely by yourself. Fortunately, there's an additional choice - US Legal Forms.

Firstly, verify if the Bexar Approval of Incentive Stock Option Plan aligns with your state's or county's regulations.

In the event the document contains a description, ensure to ascertain what it's applicable for.

- It will assist you in obtaining well-crafted legal documents without incurring exorbitant costs for legal services.

- US Legal Forms boasts a comprehensive inventory of over 85,000 state-specific document templates, including Bexar Approval of Incentive Stock Option Plan and form bundles.

- We offer documents for a variety of life situations: from divorce paperwork to real estate forms.

- We have been operating for over 25 years and have established a formidable reputation among our clientele.

- Here's how you can join them and acquire the necessary template without any hassle.

Form popularity

FAQ

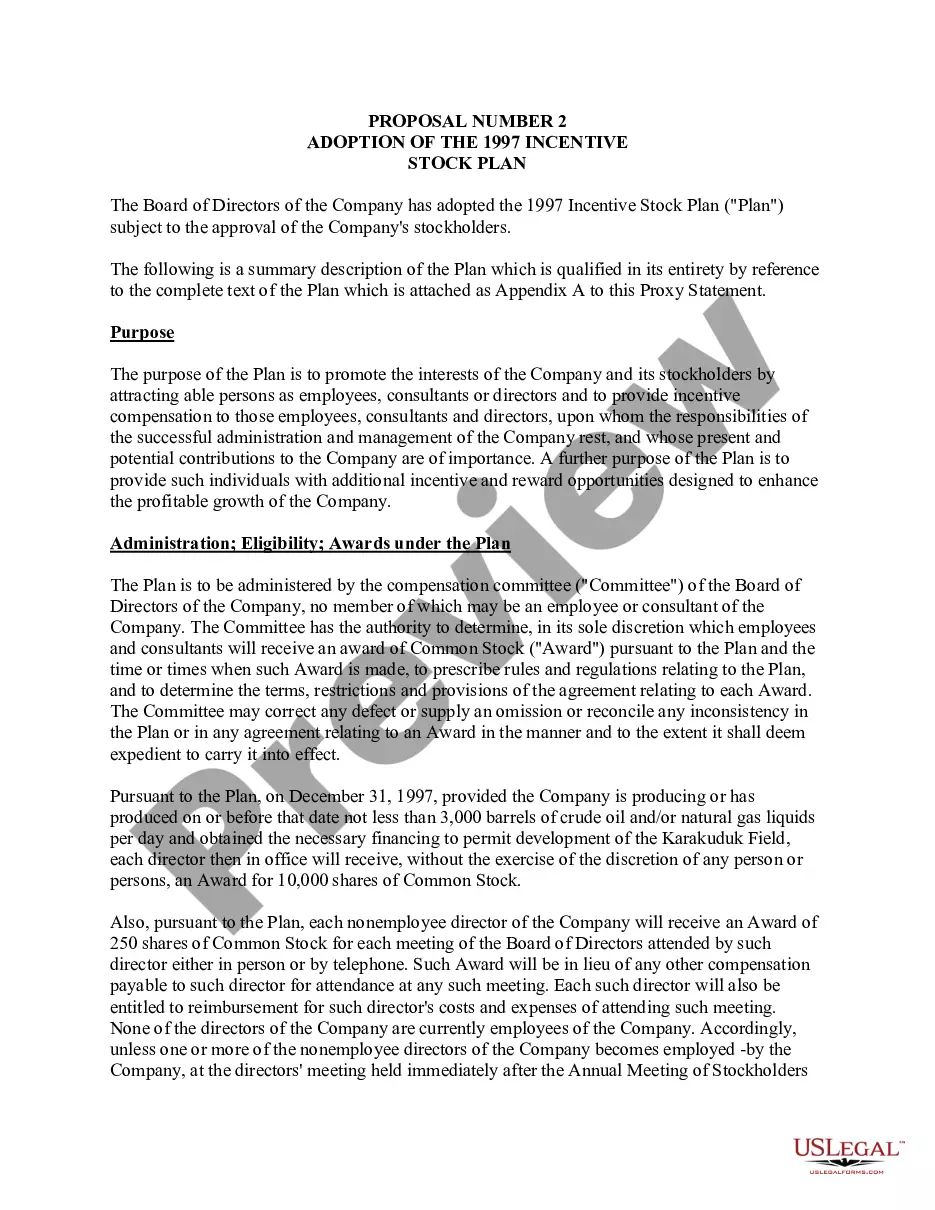

The $100,000 limit for Incentive Stock Options applies to the value of the options that can be granted to an employee in a single tax year. This regulation is part of the Bexar Texas Approval of Incentive Stock Option Plan framework. Companies should plan their offerings accordingly to ensure compliance and optimize benefits for their employees.

The $100,000 limit refers to the maximum value of ISOs that can qualify for special tax treatment in any given year. In the context of the Bexar Texas Approval of Incentive Stock Option Plan, understanding this limit is crucial. Exceeding this cap means that the excess options will not receive favorable tax treatment, making it essential for companies to navigate these rules carefully.

On June 30, the SEC approved rules requiring shareholder approval of equity compensation plans, including stock option plans. The new rules will also require approval for repricings and material plan changes.

Incentive stock options, or ISOs, are a type of equity compensation granted only to employees, who can then purchase a set quantity of company shares at a certain price, while receiving favorable tax treatment.

Shareholder approval will only be required for issuances to a related party, and will not be required for issuances to 1) a subsidiary, affiliate, or other closely related person of a related party, or 2) any company or entity in which a related party has a substantial direct or indirect interest.

Reporting an Incentive Stock Option adjustment for the Alternative Minimum Tax. If you buy and hold, you will report the bargain element as income for Alternative Minimum Tax purposes. Report this amount on Form 6251: Alternative Minimum Tax for the year you exercise the ISOs.

On June 30, the SEC approved rules requiring shareholder approval of equity compensation plans, including stock option plans. The new rules will also require approval for repricings and material plan changes.

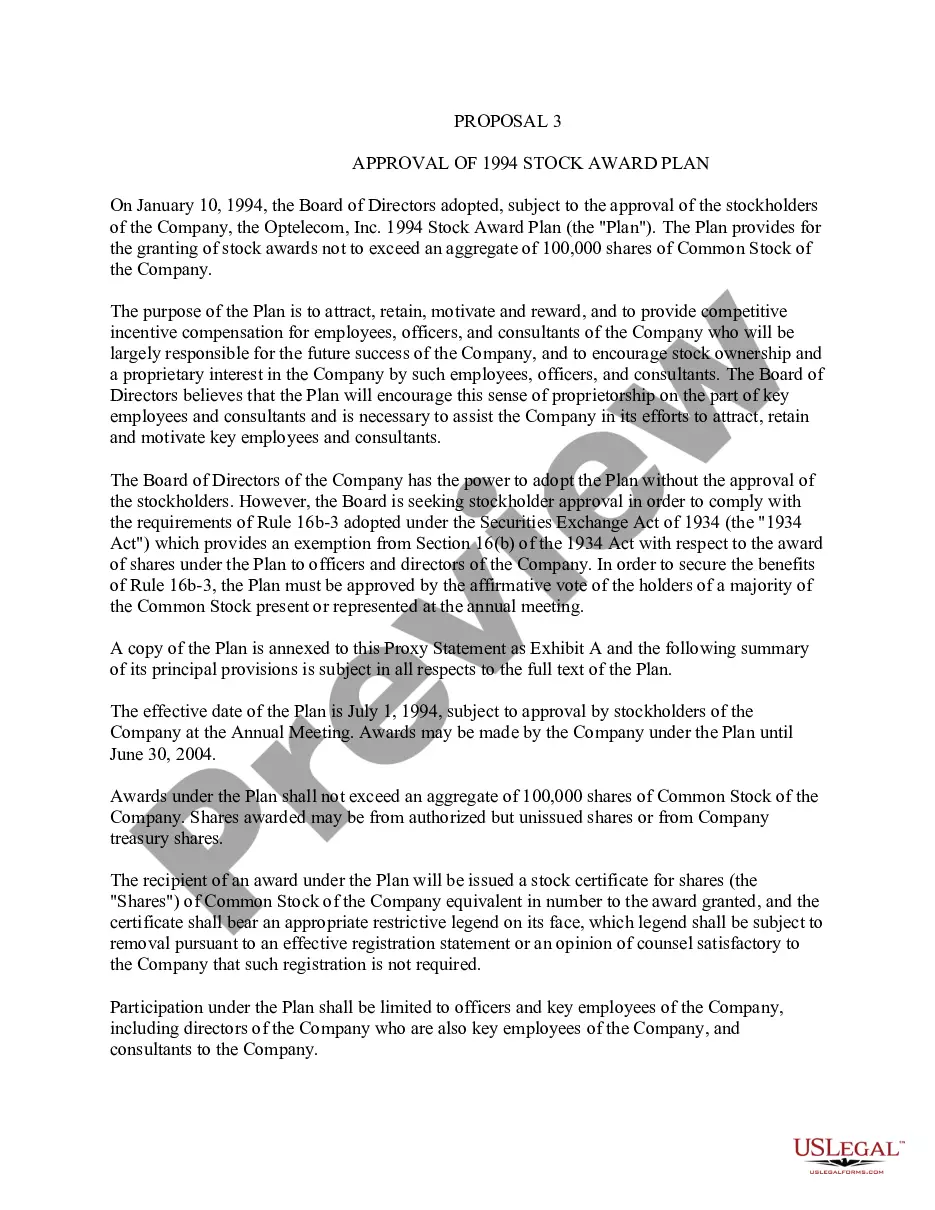

An incentive stock option must be granted within 10 years from the date that the plan under which it is granted is adopted or the date such plan is approved by the stockholders, whichever is earlier. To grant incentive stock options after the expiration of the 10-year period, a new plan must be adopted and approved.

Your employer is not required to withhold income tax when you exercise an Incentive Stock Option since there is no tax due (under the regular tax system) until you sell the stock.

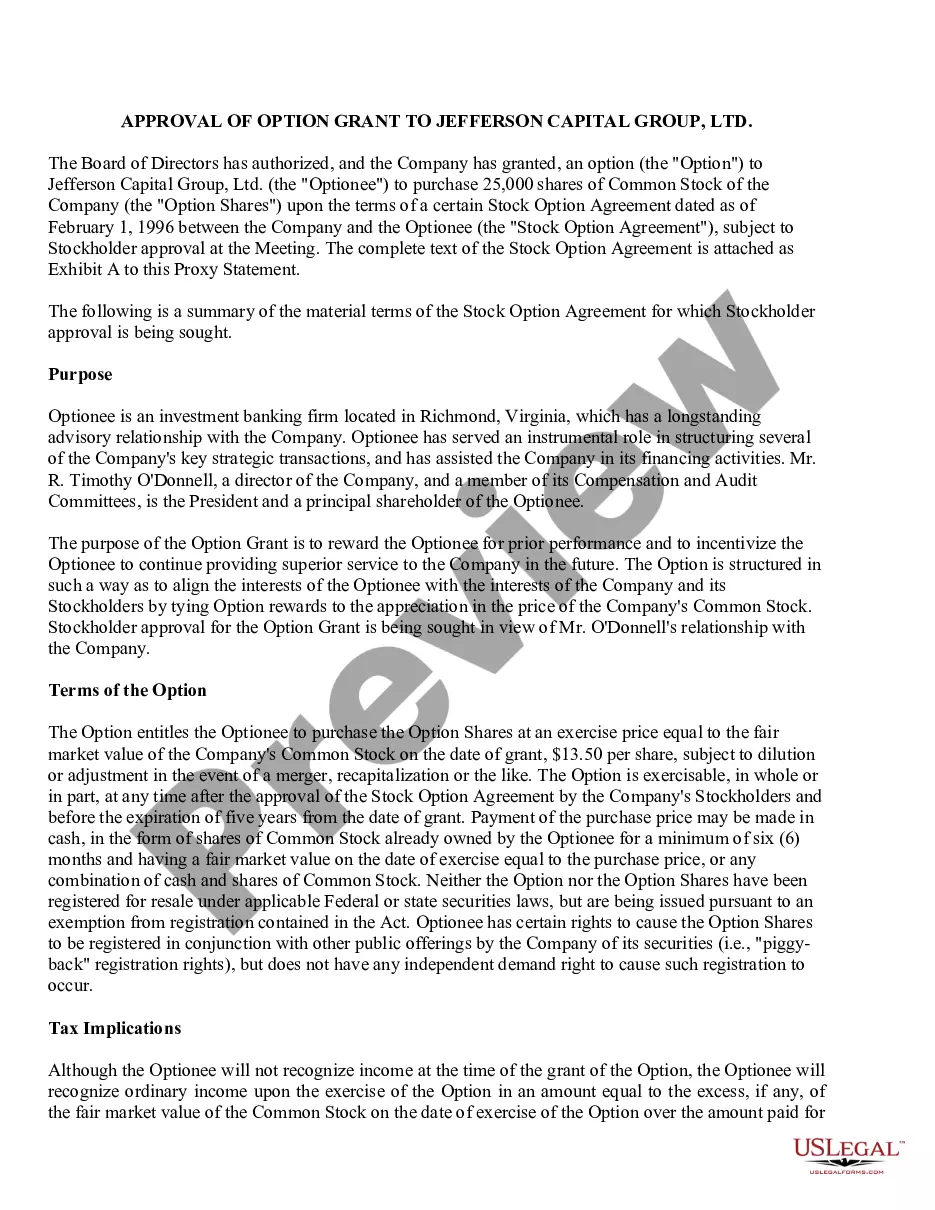

Under both the NYSE and NASDAQ listing standards, a public company must obtain shareholder approval before it can issue shares under an equity incentive plan or make material revisions to an equity incentive plan.