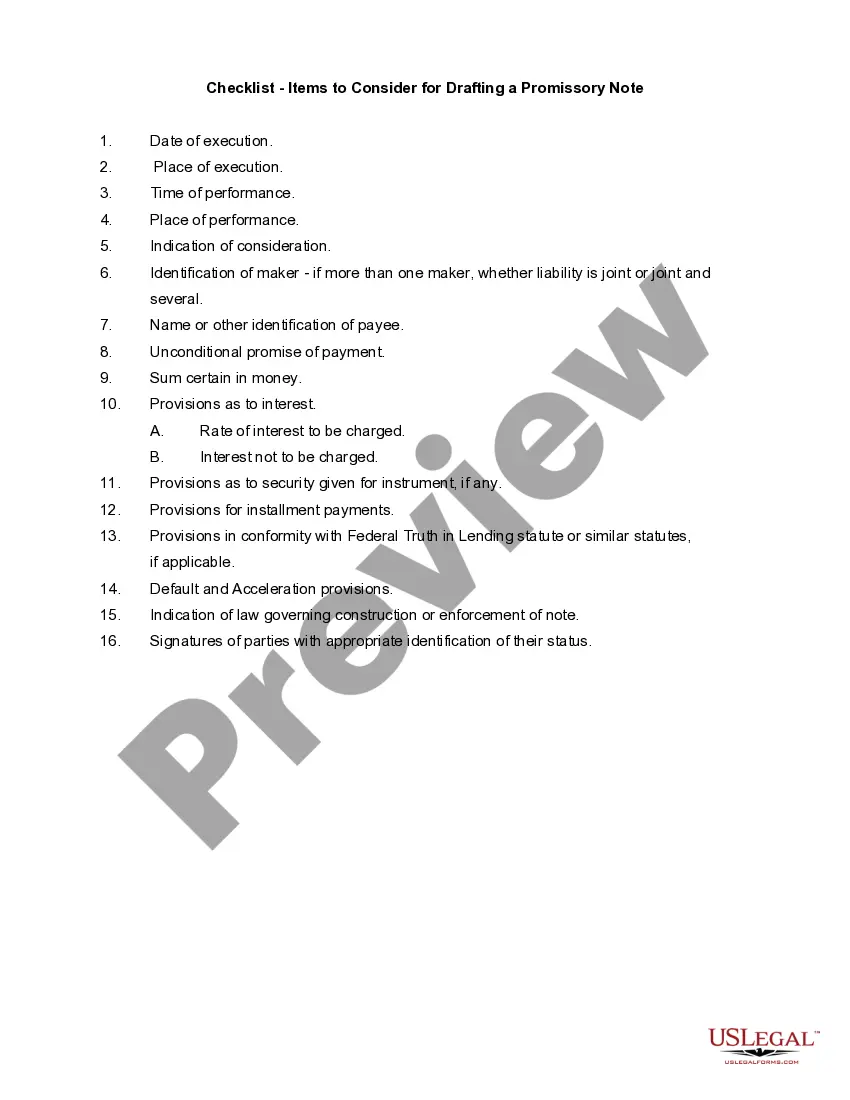

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person or to the bearer.

Fulton Georgia Checklist - Items to Consider for Drafting a Promissory Note

Category:

State:

Multi-State

County:

Fulton

Control #:

US-03060BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Fulton Georgia Checklist - Items To Consider For Drafting A Promissory Note?

Whether you intend to open your company, enter into an agreement, apply for your ID update, or resolve family-related legal issues, you must prepare certain paperwork corresponding to your local laws and regulations. Finding the right papers may take a lot of time and effort unless you use the US Legal Forms library.

The platform provides users with more than 85,000 professionally drafted and verified legal documents for any personal or business occurrence. All files are collected by state and area of use, so opting for a copy like Fulton Checklist - Items to Consider for Drafting a Promissory Note is fast and easy.

The US Legal Forms library users only need to log in to their account and click the Download button next to the required form. If you are new to the service, it will take you a few more steps to obtain the Fulton Checklist - Items to Consider for Drafting a Promissory Note. Adhere to the guidelines below:

- Make sure the sample meets your personal needs and state law regulations.

- Look through the form description and check the Preview if available on the page.

- Make use of the search tab specifying your state above to locate another template.

- Click Buy Now to get the sample when you find the right one.

- Opt for the subscription plan that suits you most to proceed.

- Log in to your account and pay the service with a credit card or PayPal.

- Download the Fulton Checklist - Items to Consider for Drafting a Promissory Note in the file format you require.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Forms provided by our library are reusable. Having an active subscription, you are able to access all of your previously acquired paperwork at any time in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date formal documents. Sign up for the US Legal Forms platform and keep your paperwork in order with the most extensive online form library!

Form popularity

FAQ

A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan.

A Promissory Note is a document that is signed by an individual that details the amount of money borrowed from another individual or organization (Lender). A promissory note is also referred to as a Promise to Pay note or a Note payable.

Parties of Promissory Note All promissory notes constitute three primary parties. These include the drawee, drawer and payee. Drawer: A drawer is a person who agrees to pay the drawee a certain amount of money on the maturity of the promissory note. He/she is also known as maker.

Signatures : All parties must sign the note for it to be legally enforceable. Generally promissory notes only need to be signed by the borrower that is making the promise. Release of Promissory Note : Once the loan is paid back, the commitment of the parties in the promissory note can also be brought to an end.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

The format of a promissory note holds the principal amount, issuance date and place, interest rate, due date, parties' contact details, etc. One can make the payment in instalments or as a lump sum, thus ensuring flexibility.

A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan.

Types of Promissory Notes Simple Promissory Note.Student Loan Promissory Note.Real Estate Promissory Note.Personal Loan Promissory Notes.Car Promissory Note.Commercial Promissory note.Investment Promissory Note.

How To Write a Promissory Note Step 1 Full names of parties (borrower and lender)Step 2 Repayment amount (principal and interest)Step 3 Payment plan.Step 4 Consequences of non-payment (default and collection)Step 5 Notarization (if necessary)Step 6 Other common details.