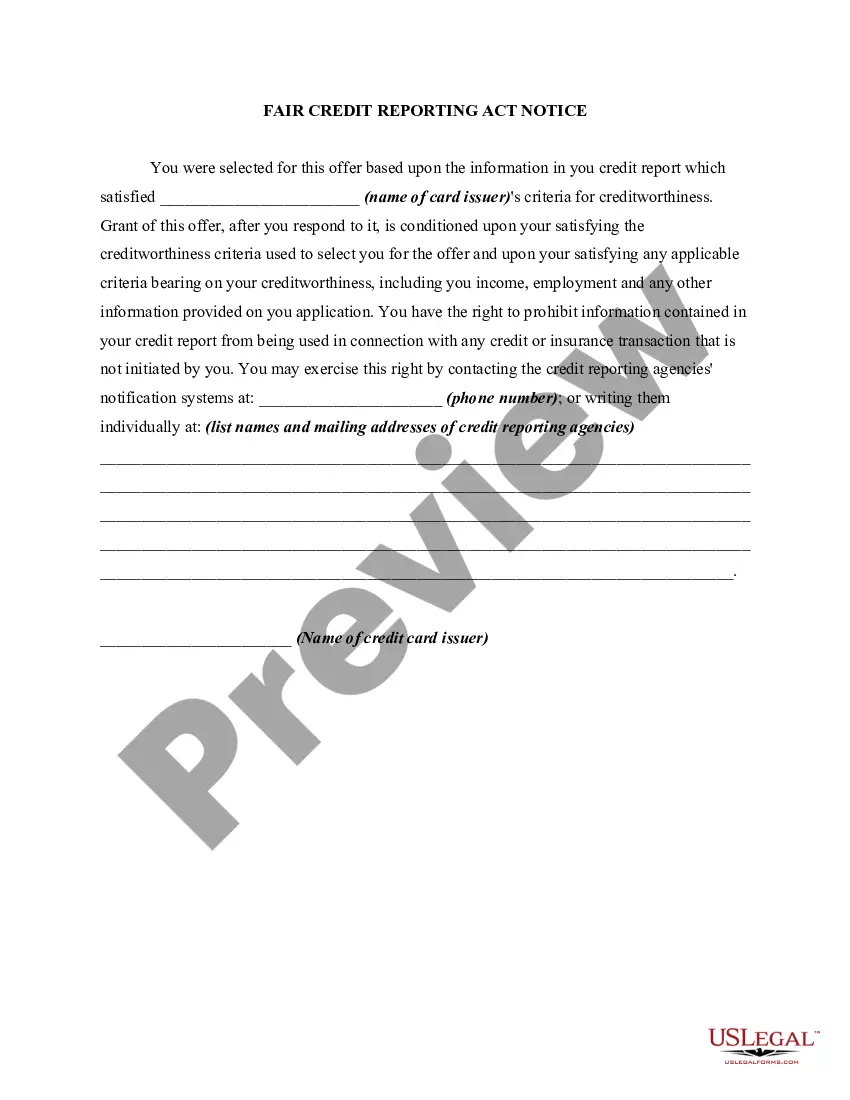

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

Form popularity

FAQ

Banks must ensure that the consumer information they provide is accurate, complete, and current. They need to have protocols in place to rectify any inaccuracies and must comply with the Fair Credit Reporting Act. By observing these regulations and the guidance offered by the Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, banks can foster stronger customer relationships.

A bank must provide an FCRA adverse action notice when it takes an action based on information in a credit report that adversely affects a consumer. This notice should inform the consumer about their right to know the details regarding how the information influenced the decision. To meet this requirement, banks can refer to the Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency for guidance.

An institution must ensure the accuracy of the information it provides to a consumer reporting agency and regularly update any changes. Furthermore, they must comply with relevant regulations to protect consumers' rights. By adhering to the standards stated in the Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, institutions can maintain trust and accountability.

Negative information refers to any unfavorable data that can affect a consumer's credit score, including late payments, defaults, or bankruptcies. This information can significantly influence lending decisions and interest rates. Understanding the standards set in the Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency is vital to managing consumer credit effectively.

A furnisher must notify a consumer within five business days if it determines that a direct dispute is frivolous or irrelevant. This requirement ensures that consumers are promptly informed about the status of their disputes. Following the guidelines outlined in the Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency can help furnishers comply with this rule.

Consumers can submit disputes to the credit reporting agency that maintains the inaccurate information, their lender, or any furnisher who provided the data. This enables consumers to correct errors and ensures the accuracy of their credit reports. As highlighted in the Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, knowing where to direct disputes is essential for consumers.

The negative information notice requirement stipulates that you must inform consumers if you report negative information to credit reporting agencies. This aspect is crucial for consumer rights, allowing them to address issues that might impact their credit. The Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency serves as a relevant guideline in handling such notifications appropriately.

You must notify a consumer within a reasonable time when you furnish negative information to a consumer reporting agency. This notification helps consumers understand how their credit may be affected. The Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency emphasizes the importance of communication in maintaining transparency in credit reporting.

Addressing issues related to FCRA notices starts with understanding your rights under the Fair Credit Reporting Act. If you feel that this notice impacts you negatively, it is essential to take action promptly. Platforms like uslegalforms can assist you in responding appropriately to a Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, ensuring you navigate the process efficiently and effectively.

A FCRA notice is an official communication that informs you about the use of your credit information. It typically outlines what actions have been taken based on your credit report, like an increase in charges or altering terms. For those who receive a Plano Texas Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, understanding this notice helps you know how your data affects your financial position.