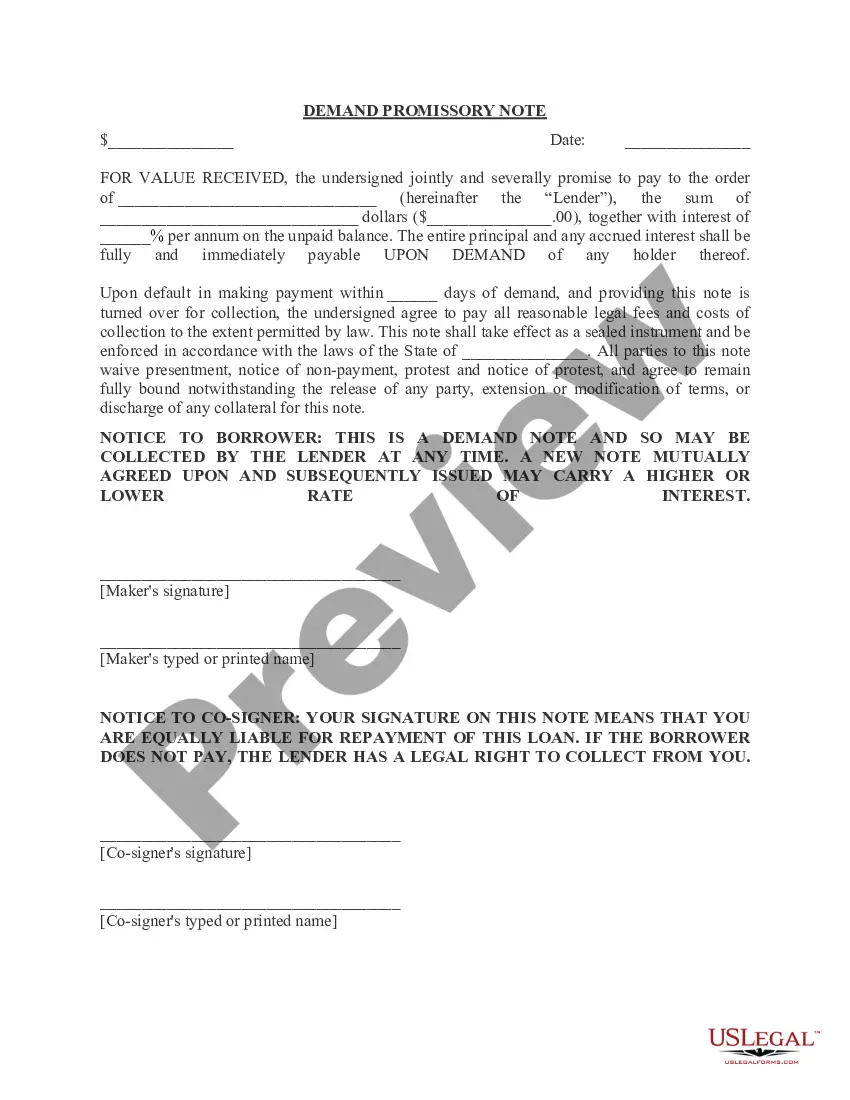

This form is a Promissory Note in connection with the sale of a vehicle where the Buyer is to pay a portion of the purchase price over time.

Chicago Illinois Promissory Note in Connection with Sale of Vehicle or Automobile

Category:

State:

Illinois

City:

Chicago

Control #:

IL-00431-D

Format:

Word;

Rich Text

Instant download

Description

How to fill out Illinois Promissory Note In Connection With Sale Of Vehicle Or Automobile?

Regardless of social or career position, completing legal forms is an unfortunate obligation in today's society.

Frequently, it is nearly impossible for an individual lacking legal expertise to produce such documents from scratch, primarily due to the complex language and legal intricacies involved.

This is where US Legal Forms proves to be useful.

Make certain that the document you have selected is tailored to your region, as the regulations of one state may not apply in another.

Examine the document and review a brief summary (if available) of scenarios for which the paper can be utilized.

- Our service offers an extensive assortment of over 85,000 ready-to-use, state-specific documents applicable to nearly any legal situation.

- US Legal Forms is also an excellent tool for associates or legal advisors seeking to enhance their efficiency by using our DIY forms.

- Whether you need the Chicago Illinois Promissory Note in Context with Sale of Vehicle or Automobile, or any other document recognized in your jurisdiction, everything is readily available with US Legal Forms.

- Here’s how to swiftly obtain the Chicago Illinois Promissory Note in Context with Sale of Vehicle or Automobile using our reliable service.

- If you are already a customer, feel free to Log In to your account to access the necessary document.

- However, if you are new to our service, please ensure you follow these steps prior to downloading the Chicago Illinois Promissory Note in Context with Sale of Vehicle or Automobile.

Form popularity

FAQ

A car promissory note is an agreement where a borrower promises to make payments in exchange for a vehicle. It typically has even terms throughout the loan, but often also includes a lump sum down payment at the beginning of the loan term. It also should include information about the make and model of the vehicle.

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

Generally, as long as the promissory note contains legally acceptable interest rates, the signatures of the two contracted parties, and are within the applicable Statute of Limitations, they can be upheld in a court of law.

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame.

A promissory note can be used for different types of loans such as a mortgage, student loan, car loan, business loan or personal loan.

A promissory note is a specific form of a bill of exchange with the essential difference being that a promissory note is a promise by the maker to pay whereas an 'ordinary' bill of exchange is an order to someone else to pay.

When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. In some cases, the note is endorsed in blank, which makes it a bearer instrument under Article 3 of the Uniform Commercial Code. So, any party that possesses the note has the legal authority to enforce it.

Promissory Notes: An Overview. Bills of exchange and promissory notes are written commitments between two parties that confirm a financial transaction has been agreed upon. Bills of exchange are more often used in international trade, whereas promissory notes are used most often in domestic trade.