This form is a generic example that may be referred to when preparing such a form.

Anaheim California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually

Category:

State:

California

City:

Anaheim

Control #:

CA-01701BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out California Deed Of Trust Securing Promissory Note With No Payment Due Until Maturity And Interest To Compound Annually?

If you have previously employed our service, sign in to your account and store the Anaheim California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually on your device by clicking the Download button. Ensure that your subscription is active. If not, renew it per your payment plan.

If this is your initial encounter with our service, follow these straightforward steps to acquire your file.

You have continuous access to every document you have purchased: you can find it in your profile within the My documents section whenever you need to use it again. Leverage the US Legal Forms service to effortlessly locate and save any template for your personal or business requirements!

- Ensure you’ve located the right document. Browse through the description and utilize the Preview feature, if available, to confirm its suitability for your requirements. If it does not suit you, use the Search tab above to find the suitable one.

- Acquire the template. Click the Buy Now button and select either a monthly or yearly subscription option.

- Create an account and complete the payment. Use your credit card information or the PayPal option to finalize the purchase.

- Receive your Anaheim California Deed of Trust Securing Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually. Choose the file format for your document and save it to your device.

- Complete your document. Print it out or make use of professional online editors to fill it out and sign it digitally.

Form popularity

FAQ

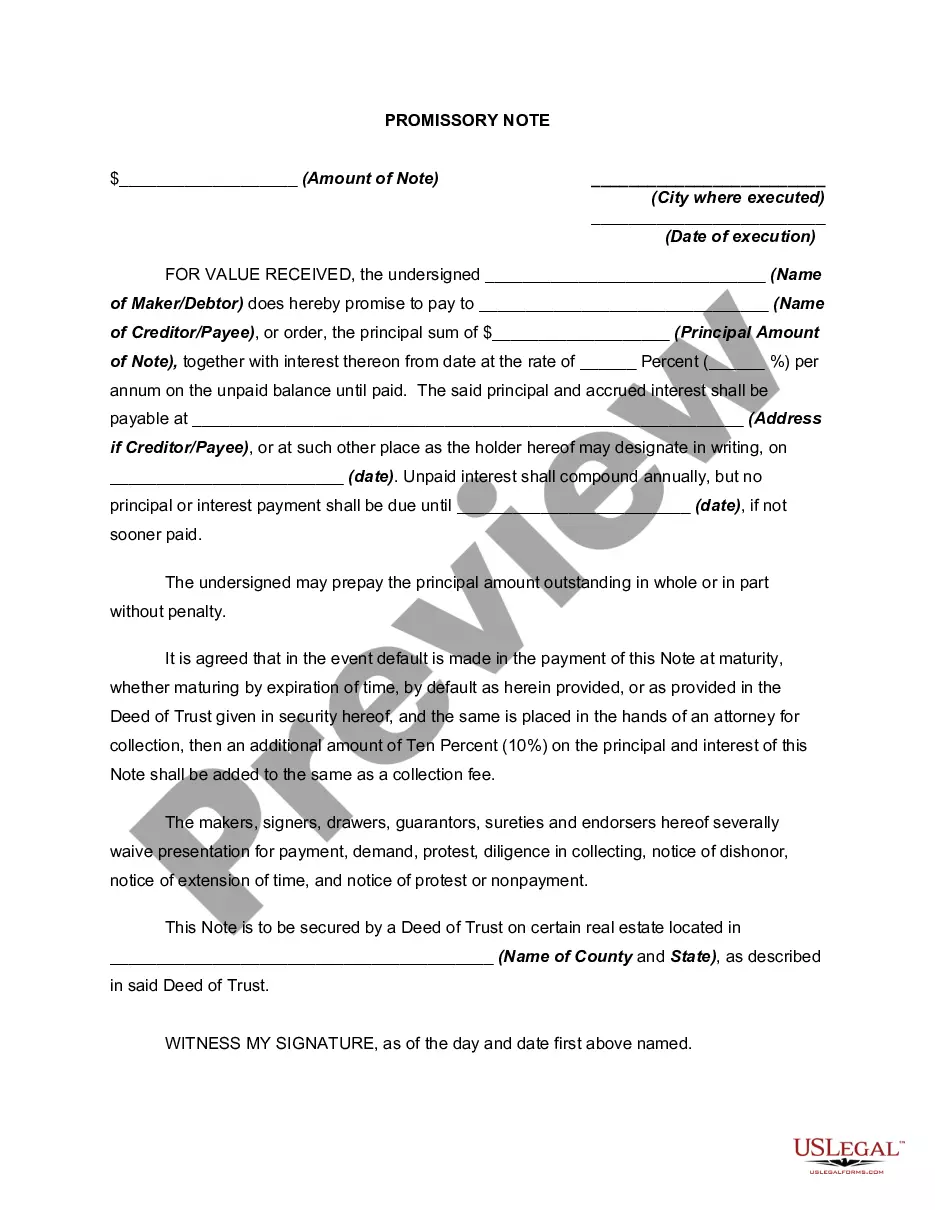

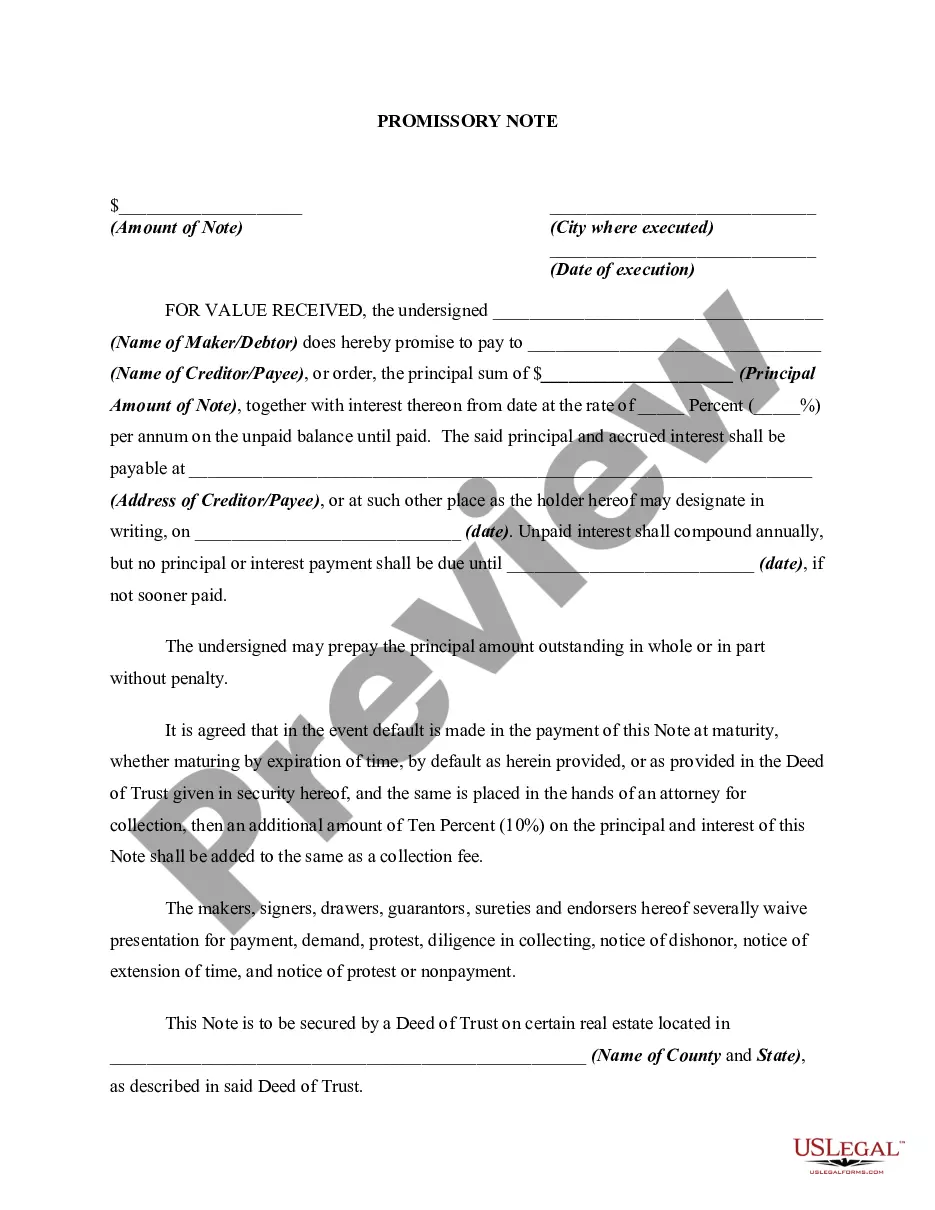

To Recap: The Deed is a recorded document memorializing the transfer of property from the Grantor to the Grantee. The Note is an unrecorded paper that binds an individual who has assumed debt through a promise-to-pay instrument.

A promissory note is a key piece of a home loan application and mortgage agreement, ensuring that a borrower agrees to be indebted to a lender for loan repayment. Ultimately, it serves as a necessary piece of the legal puzzle that helps guarantee that sums are repaid in full and in a timely fashion.

Promissory notes, also known as mortgage notes, are written agreements in which one party promises to pay another party a certain amount of money at a later date in time. Banks and borrowers typically agree to these notes during the mortgage process.

A promissory note and deed of trust have one simple function to secure the repayment of a loan by placing a lien on the property as collateral. If the loan is not paid, then the lender has the right to sell the property. Both documents are used to make sure the seller secures the repayment of the loan.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

In general, promissory notes are used for more informal relationships than loan agreements. A promissory note can be used for friend and family loans, or short-term, small loans. Loan agreements, on the other hand, are used for everything from vehicles to mortgages to new business ventures.

The promissory note could bear reasonable interest and be secured by the trust property. As discussed below, a promissory note is generally considered evidence of a loan transaction rather than the current payment of a specific amount.

Deeds of trust are used in conjunction with promissory notes. The deed of trust is the security for the amount loaned to finance the real estate purchase, and is secured by the underlying piece of real estate. The deed of trust is what secures the promissory note.

The maker signs the note, but the payee doesn't have to do so. A negotiable promissory note is one where the payee can negotiate (i.e., transfer) it to another party who becomes its holder. If a payee negotiates the note, its new holder is entitled to be paid.

With a deed of trust, the lender gives the borrower the funds to make the purchase. The borrower provides the lender with a promissory note. The promissory note outlines the terms of the loan and the borrower's promise to pay. At this point, the borrower transfers the real property interest to the trustee.