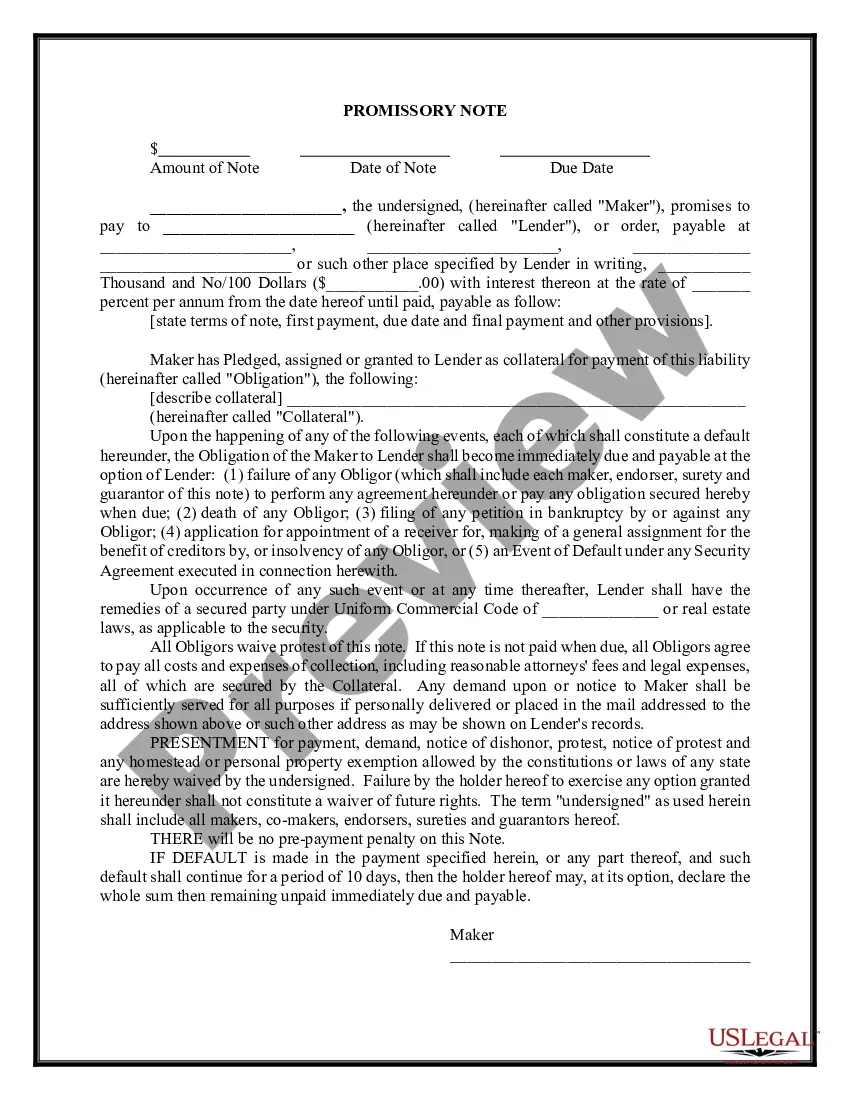

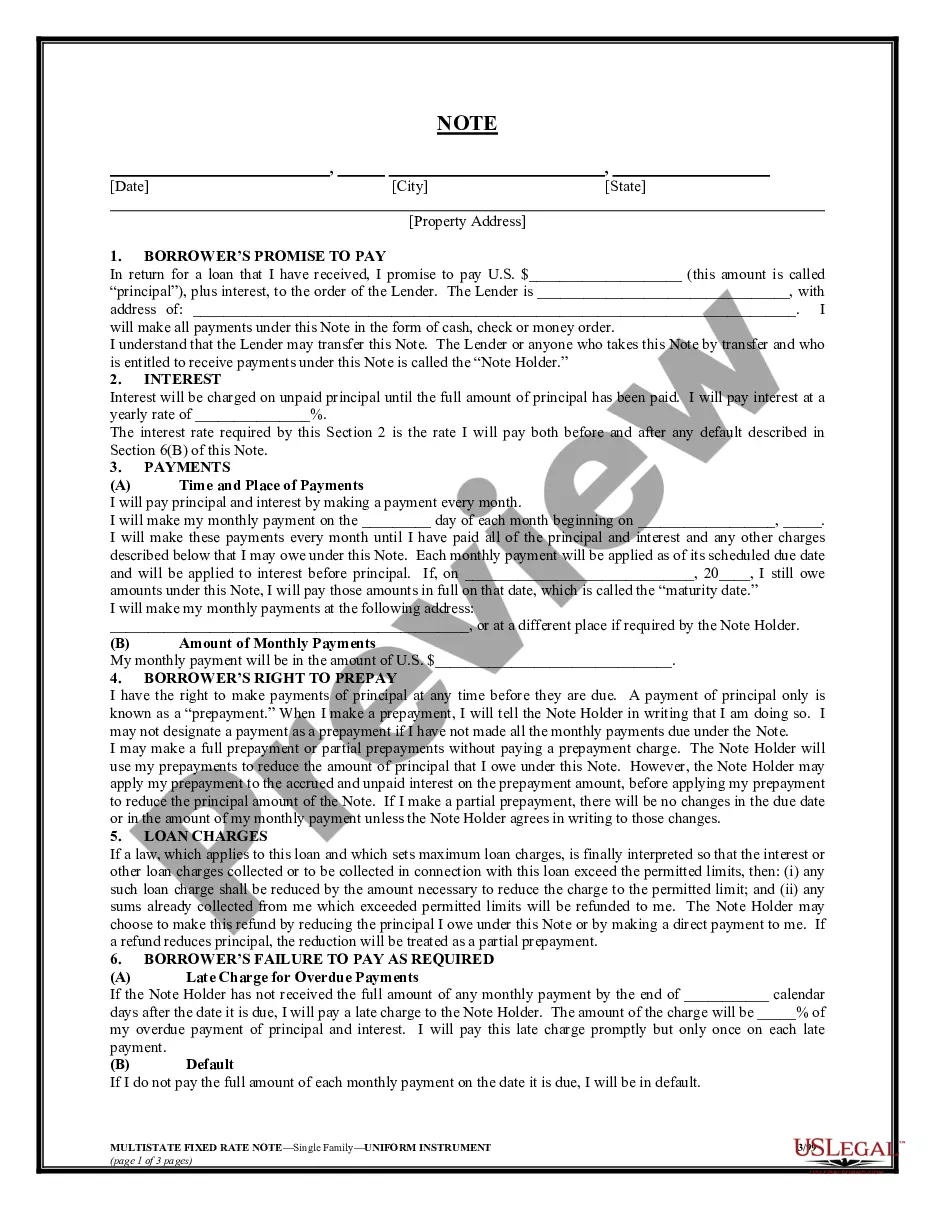

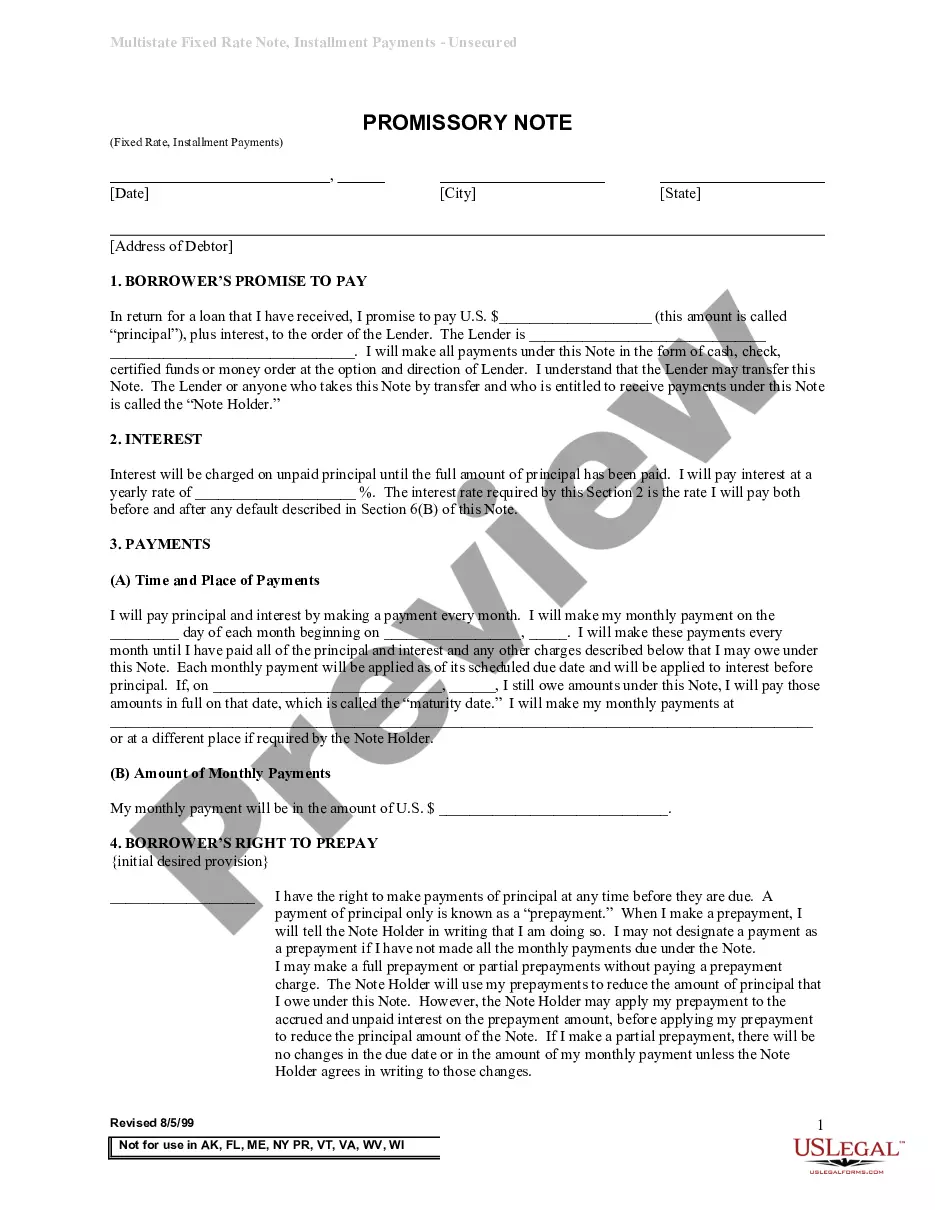

What Is a Promissory Note? Understanding Its Purpose and Use

A promissory note is a legal document wherein the issuer, referred to as the maker, promises to pay a specified amount of money to a payee at a designated time or on-demand. This instrument is a written promise and serves as evidence of a debt. Essentially, it captures the terms of the loan and can include details regarding interest rates, payment schedules, and consequences of default.

Key components of the form

A well-drafted promissory note contains several essential elements:

- Principal Amount: The total sum of money borrowed.

- Interest Rate: The cost of borrowing expressed as a percentage of the principal.

- Payment Schedule: Specifies the timeline for repayments, including amount and frequency.

- Maturity Date: The date by which the loan must be fully repaid.

- Signatures: Required from the borrower and, if applicable, co-signers or witnesses.

These components ensure that both parties have a clear understanding of their obligations under the agreement.

Who should use this form

A promissory note is utilized by individuals or entities who are lending money and need formal documentation to ensure repayment. This includes:

- Friends or family members lending to one another.

- Businesses offering loans to clients.

- Investors providing capital in exchange for repayment with interest.

It verifies the details of the loan and protects the interests of both the lender and borrower.

Common mistakes to avoid when using this form

When creating or entering into a promissory note, it is crucial to avoid several common pitfalls, such as:

- Not specifying repayment terms: Ensure that the payment schedule and terms are clear and complete.

- Failure to include interest rates: Omitting this detail can lead to misunderstandings or disputes.

- Neglecting to sign the document: Failing to have all required parties sign invalidates the note.

- Ignoring state laws: Be aware that laws governing promissory notes can vary by state.

Addressing these issues can help minimize risks and protect all parties involved.

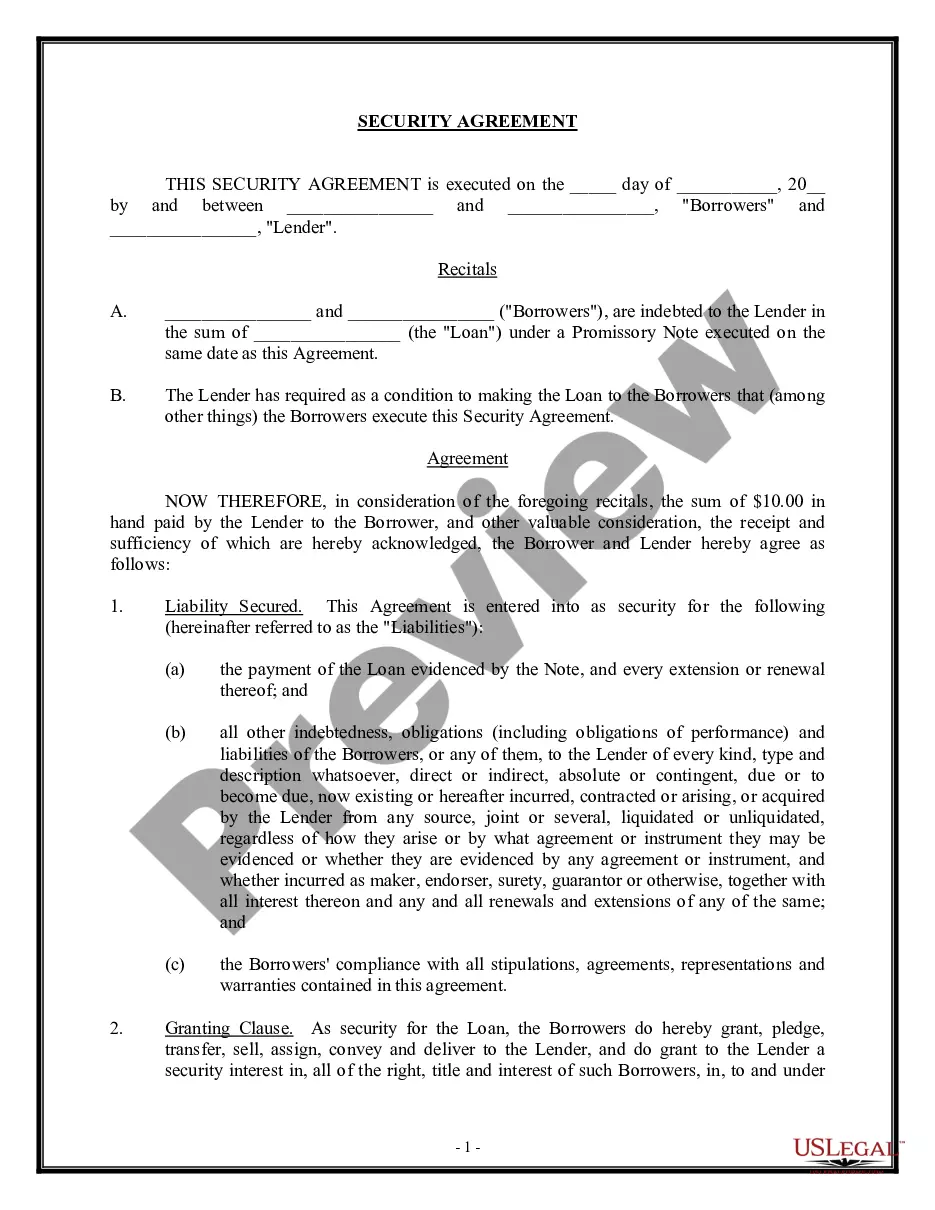

What documents you may need alongside this one

When preparing a promissory note, you may need to gather additional documents to support the agreement, such as:

- Proof of identity for both the borrower and lender.

- A written loan agreement that outlines the terms, if applicable.

- Financial statements or proof of income to validate the borrower’s ability to repay.

Having these documents can lend credibility and reinforce the terms agreed upon in the promissory note.

What to expect during notarization or witnessing

Notarization or witnessing of a promissory note serves as an additional layer of authenticity. During this process, you can expect:

- The notary or witness will verify the identities of all parties involved.

- All parties will need to sign the document in front of the notary or witness.

- The notary will apply their seal and may complete a notarial certificate, acknowledging the signing event.

This process enhances the legal standing of the note and reduces the risk of fraud.