This form is for the situation where the seller is to apply for a release of liability from an assumed loan or reinstatement of VA entitlement.

Wyoming Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan

Category:

State:

Multi-State

Control #:

US-00472-A1

Format:

Word;

Rich Text

Instant download

Description

How to fill out Addendum For Release Of Liability On Assumption Of FHA, VA Or Conventional Loan, Restoration Of Seller's Entitlement For VA Guaranteed Loan?

Selecting the optimal legal document format can be a challenge. Of course, there are numerous templates accessible online, but how can you locate the legal form you require? Utilize the US Legal Forms website. The service provides a plethora of templates, including the Wyoming Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan, which you can utilize for business and personal needs. All of the forms are reviewed by experts and meet federal and state standards.

If you are currently registered, Log In to your account and click the Download button to obtain the Wyoming Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan. Use your account to search through the legal forms you may have acquired previously. Visit the My documents section of your account and download another copy of the document you need.

If you are a new user of US Legal Forms, here are some simple steps that you should follow: First, ensure you have selected the correct form for your city/state. You can review the form using the Preview button and examine the form details to confirm this is suitable for you. If the form does not meet your requirements, utilize the Search field to find the appropriate form. Once you are confident that the form is correct, click the Purchase now button to obtain the form. Choose the pricing plan you prefer and enter the required information. Create your account and complete your purchase using your PayPal account or credit card. Select the file format and download the legal document template to your device. Finally, complete, modify, print, and sign the received Wyoming Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan.

Make the most of US Legal Forms for all your legal documentation needs.

- US Legal Forms is the largest repository of legal documents where you can find various paper templates.

- Utilize the service to acquire professionally-crafted documents that adhere to state requirements.

- All forms are verified by professionals.

- You can access a wide range of templates for both business and personal use.

- Ensure compliance with federal and state regulations with every form you download.

- Easily manage your documents through your personal account.

Form popularity

FAQ

VA Loan Foreclosure Waiting Period Generally, Veterans must wait two years after a foreclosure event to reapply for a VA loan. This period is a mandatory cooling-off phase to ensure that the borrower has regained financial stability. While two years may sound like a long time, it's better than some alternatives.

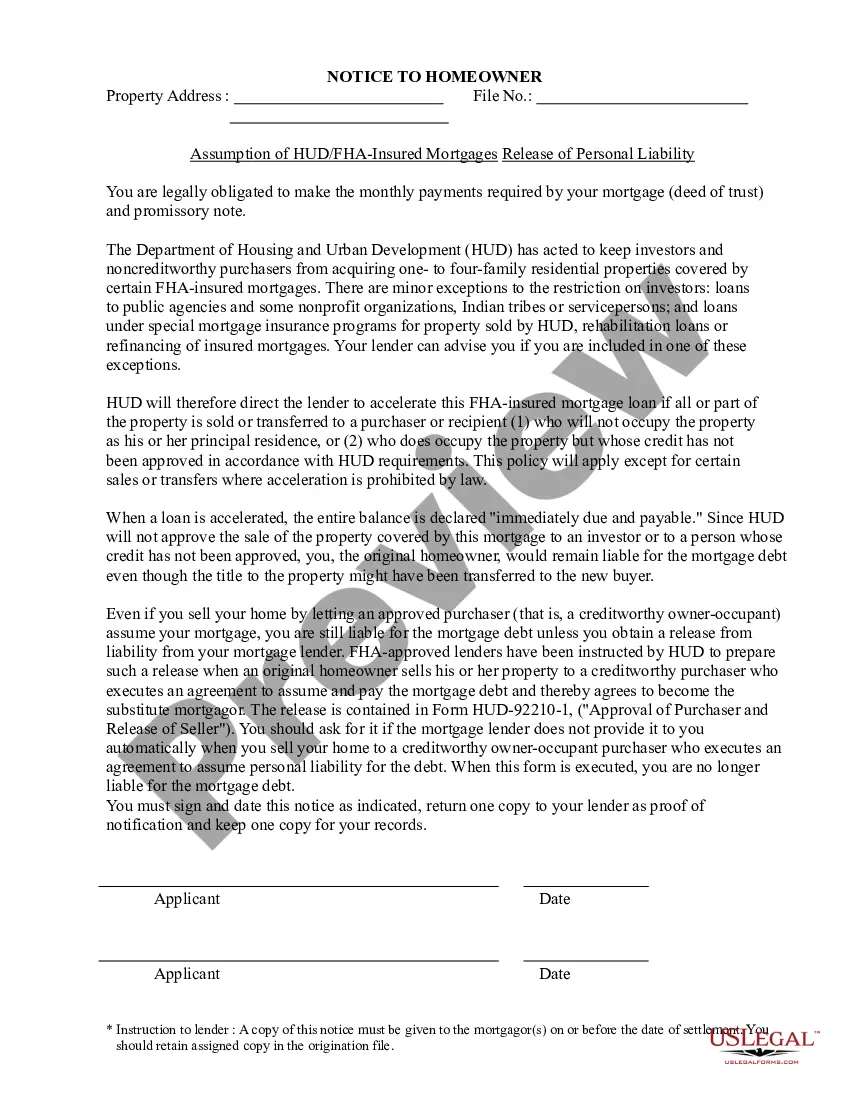

If the purchaser(s) is creditworthy and assumes the liability to the lender and VA to the same extent that you did when you obtained the loan, you will be released from liability on the loan. To obtain a release from liability, you should check with the company to whom you make your payments before you sell your home.

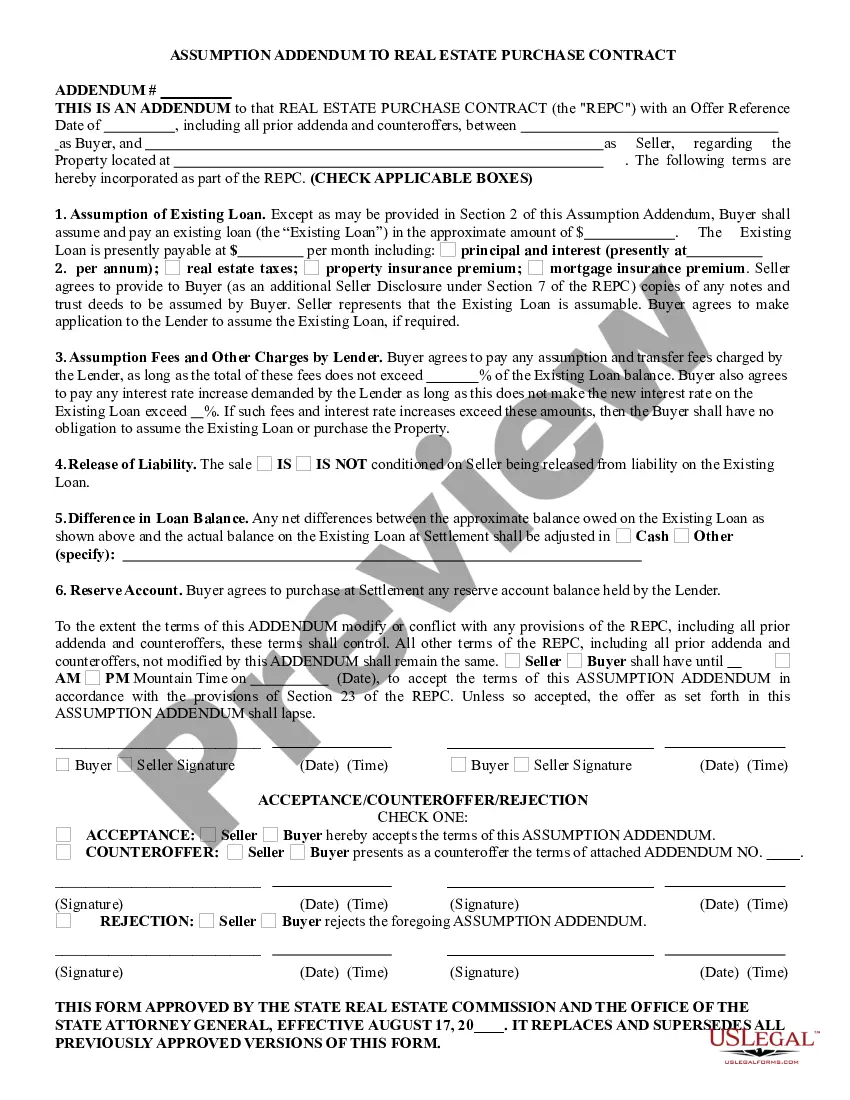

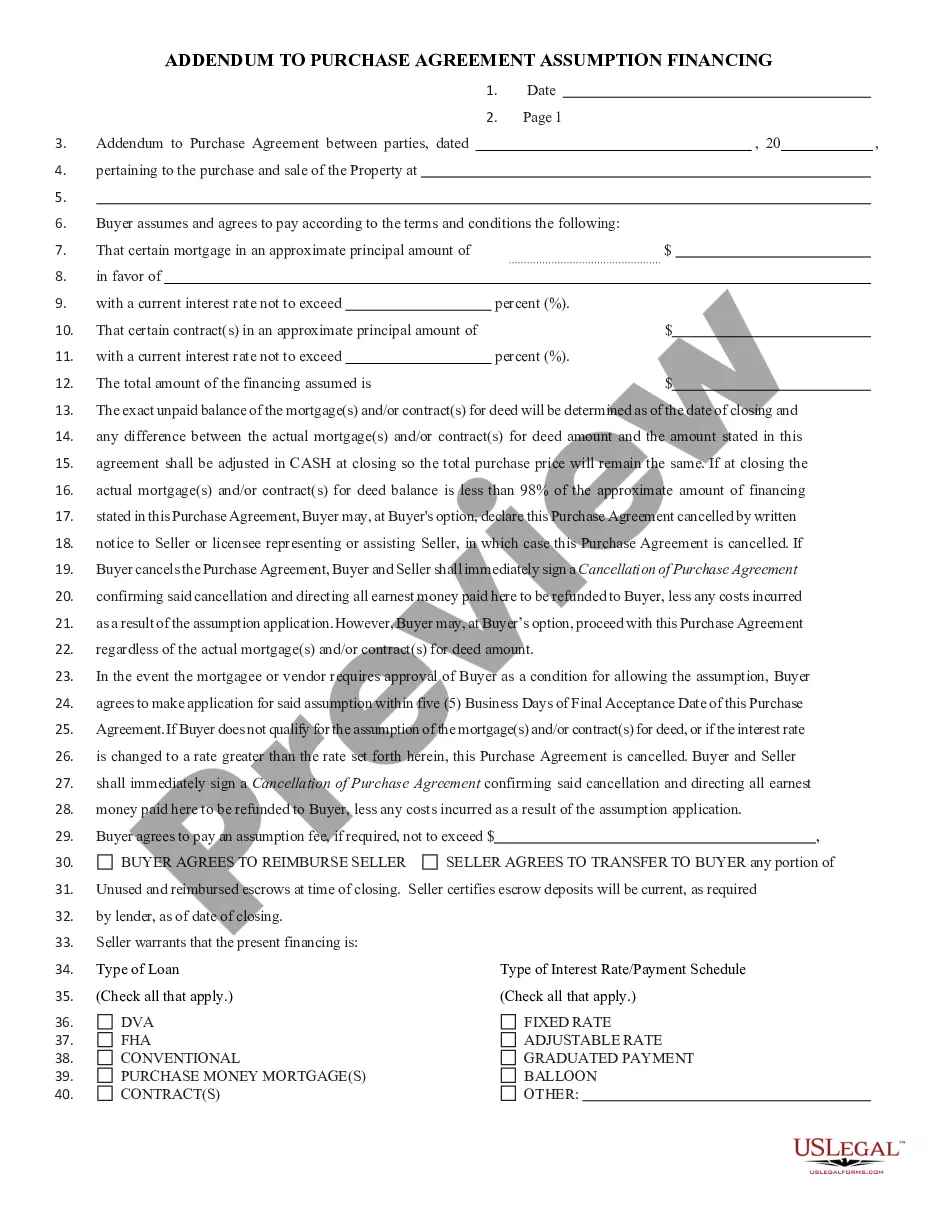

Addendum for Release of Liability on Assumed Loan and/or Restoration of Seller's VA Entitlement. Description: This Addendum is used in conjunction with the Loan Assumption Addendum if the Seller wants to be released from future liability of the loan.

An FHA/VA financing addendum is attached to a purchase contract to state that a buyer with FHA/VA financing can back out of the sale if the appraised property value is less than the asking price.

Sell the property: Selling the property you bought with your current VA loan is the simplest way to restore your entitlement. However, you must also be able to repay the full amount of the loan in addition to selling your property.

How Foreclosure Affects VA Entitlement 25% of $726,200 (standard loan limit) = $181,550. $181,550 (basic + bonus entitlement) - $75,000 (lost entitlement) = $106,550 in remaining entitlement. $106,550 x 4 = $426,200.

Unfortunately, the only way to regain your entitlement after a short sale or foreclosure is to repay that lost entitlement to the VA in full. Some buyers will likely be better served putting that money into a down payment than repaying an entitlement charge.

The $36,000 isn't the total amount you can borrow. Instead, it means that if you default on a loan that's under $144,000, we guarantee to your lender that we'll pay them up to $36,000. For loans over $144,000, we guarantee to your lender that we'll pay up to 25% of the loan amount.