West Virginia Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Partial Assignment Of Life Insurance Policy As Collateral?

US Legal Forms - among the largest libraries of legal forms in the United States - gives a variety of legal papers themes you can down load or print. Using the website, you may get a huge number of forms for business and specific functions, sorted by categories, suggests, or keywords and phrases.You can find the latest versions of forms like the West Virginia Partial Assignment of Life Insurance Policy as Collateral within minutes.

If you already possess a subscription, log in and down load West Virginia Partial Assignment of Life Insurance Policy as Collateral through the US Legal Forms catalogue. The Down load button can look on each and every form you perspective. You get access to all earlier acquired forms in the My Forms tab of your respective account.

In order to use US Legal Forms for the first time, listed below are straightforward directions to help you get began:

- Be sure to have chosen the correct form for your personal area/state. Click the Preview button to analyze the form`s content. Read the form explanation to ensure that you have selected the proper form.

- In case the form does not satisfy your requirements, take advantage of the Search area at the top of the monitor to discover the one that does.

- When you are pleased with the shape, validate your selection by simply clicking the Buy now button. Then, choose the rates program you want and offer your credentials to sign up to have an account.

- Approach the transaction. Utilize your credit card or PayPal account to finish the transaction.

- Find the file format and down load the shape on your gadget.

- Make adjustments. Fill out, modify and print and indicator the acquired West Virginia Partial Assignment of Life Insurance Policy as Collateral.

Each and every format you included in your account lacks an expiry day which is the one you have permanently. So, if you wish to down load or print another copy, just check out the My Forms section and then click about the form you want.

Obtain access to the West Virginia Partial Assignment of Life Insurance Policy as Collateral with US Legal Forms, probably the most comprehensive catalogue of legal papers themes. Use a huge number of professional and status-particular themes that meet your business or specific needs and requirements.

Form popularity

FAQ

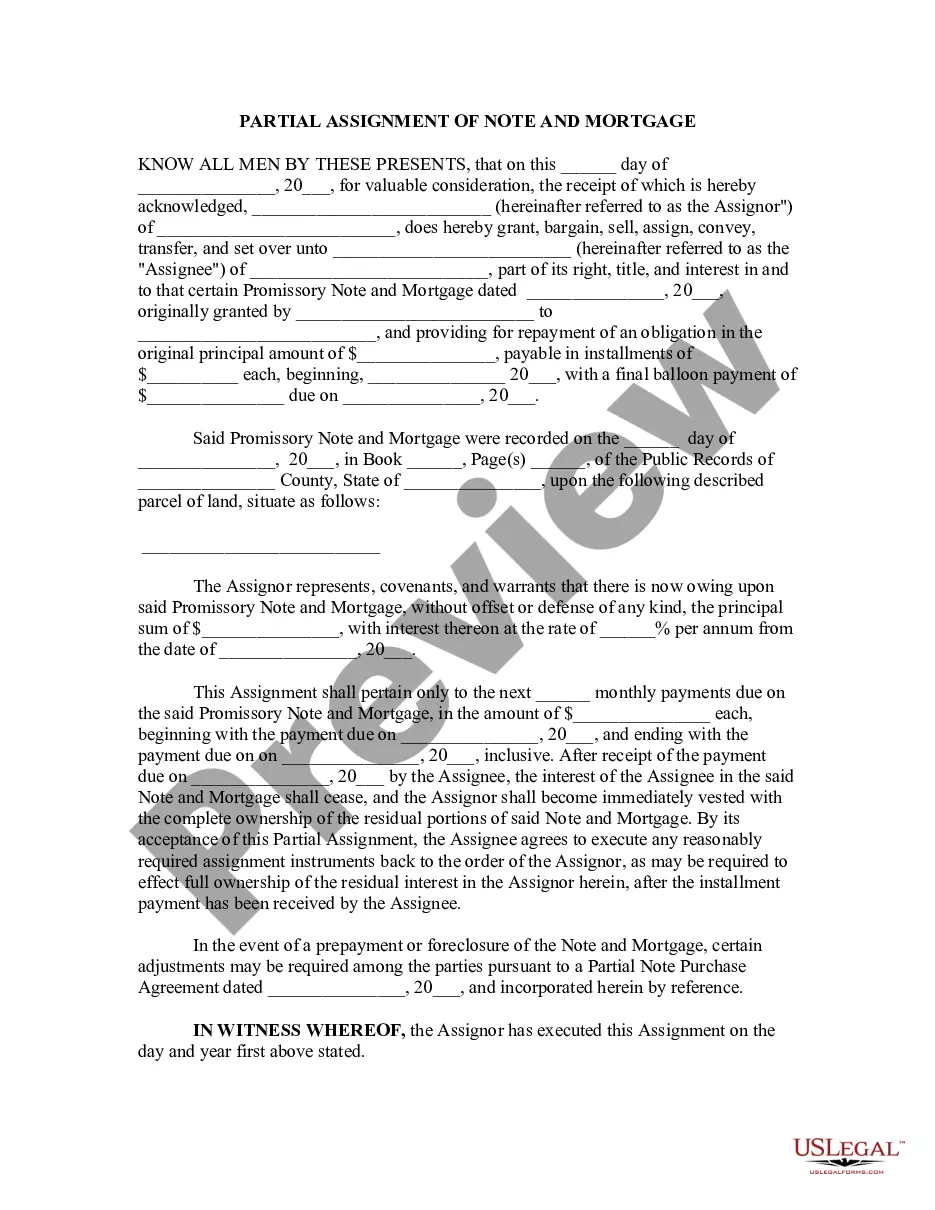

People often assign their life insurance policies to banks. A bank becomes the policy owner in this case, while the original policyholder continues to be the life assured whose death may be claimed by either the bank or the policy owner.

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.

With an absolute assignment, the entire ownership of the policy would be transferred to the assignee, or the lender. Then, the lender would be entitled to the full death benefit. With a collateral assignment, the lender is only entitled to the balance of the outstanding loan.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.