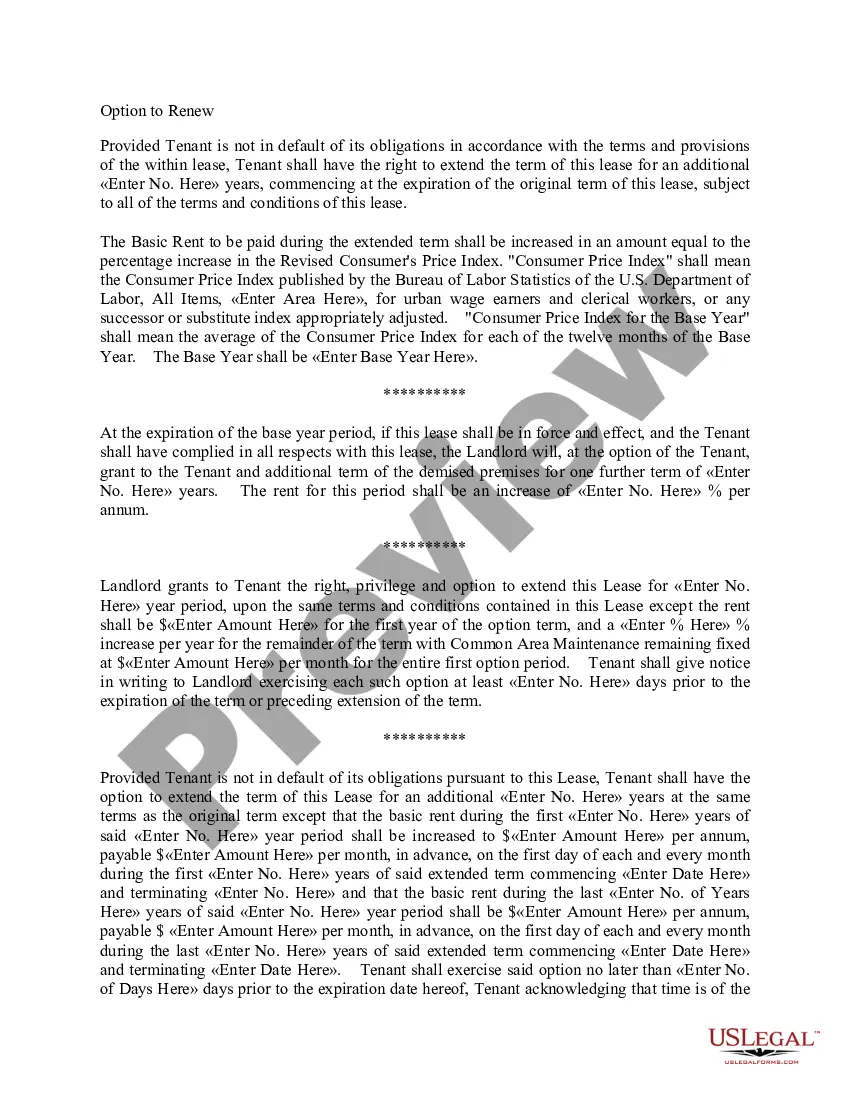

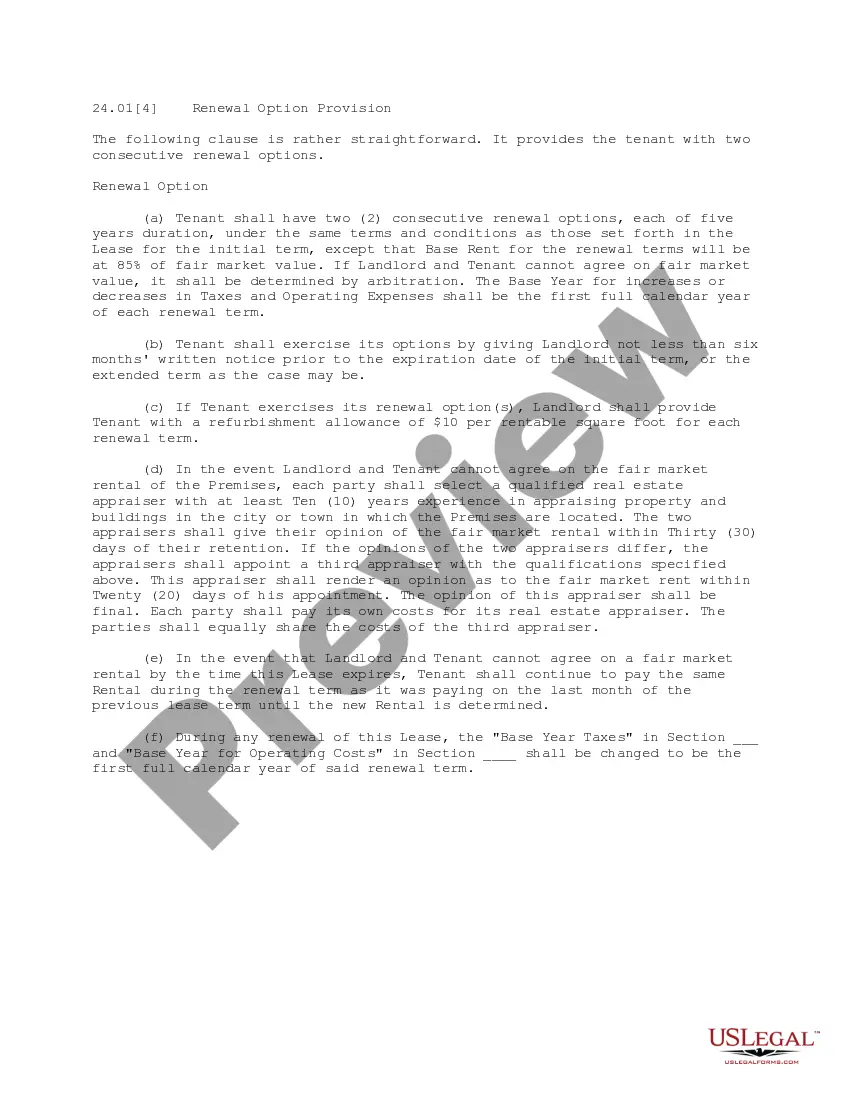

This office lease form is regarding the renewal or other extension of the lease as it relates to the "Base Year Taxes" and the "Base Year for Operating Expenses".

Virgin Islands Option to Renew that Updates the Tenant Operating Expense and Tax Basis

Category:

State:

Multi-State

Control #:

US-OL2402

Format:

Word;

PDF

Instant download

Description

How to fill out Option To Renew That Updates The Tenant Operating Expense And Tax Basis?

You may spend several hours online searching for the legitimate record template that suits the state and federal requirements you want. US Legal Forms offers a huge number of legitimate types which are evaluated by pros. It is possible to obtain or produce the Virgin Islands Option to Renew that Updates the Tenant Operating Expense and Tax Basis from my services.

If you already possess a US Legal Forms profile, you are able to log in and click the Acquire key. Following that, you are able to total, change, produce, or signal the Virgin Islands Option to Renew that Updates the Tenant Operating Expense and Tax Basis. Every single legitimate record template you acquire is yours eternally. To have yet another backup for any purchased develop, proceed to the My Forms tab and click the corresponding key.

Should you use the US Legal Forms site initially, keep to the easy recommendations listed below:

- Very first, ensure that you have selected the best record template for your area/city of your liking. Browse the develop information to ensure you have picked the correct develop. If offered, use the Preview key to look throughout the record template at the same time.

- In order to get yet another model in the develop, use the Lookup discipline to find the template that fits your needs and requirements.

- After you have found the template you want, click Acquire now to carry on.

- Pick the rates program you want, enter your qualifications, and register for a merchant account on US Legal Forms.

- Comprehensive the purchase. You should use your bank card or PayPal profile to purchase the legitimate develop.

- Pick the formatting in the record and obtain it to your gadget.

- Make adjustments to your record if necessary. You may total, change and signal and produce Virgin Islands Option to Renew that Updates the Tenant Operating Expense and Tax Basis.

Acquire and produce a huge number of record layouts utilizing the US Legal Forms website, that provides the largest collection of legitimate types. Use professional and status-certain layouts to handle your small business or person demands.

Form popularity

FAQ

An operating lease is treated like renting, and lease payments are considered operational expenses. A capital lease is treated like a loan, and the asset is considered owned by the lessee.

A triggering event within the lessee's control that changes the certainty of a lessee exercising an option to renew or terminate the lease, or purchase the underlying asset. An event written in the contract occurs that obligates the lessee to exercise or not exercise an extension or termination option.

If a lease is modified and the modification does not result in a separate contract then the lessee will need to subsequently re-measure the lease that was amended. Follow the processes outlined below to subsequently re-measure an operating or finance lease.

IFRS 16 Leases contains detailed guidance on how to account for lease modifications. A lease modification is defined as a change in the scope of a lease, or the consideration for a lease, that was not part of the original terms and conditions of the lease.

Begin with the reported operating income (EBIT). Then, add the current year's operating lease expense and subtract the depreciation on the leased asset to arrive at adjusted operating income. Finally, to adjust debt, take the reported value of debt (book value of debt) and add the debt value of the leases.

If your financial statements are issued on a tax or cash basis of accounting, the ASC 842 lease standard does not apply to you.

That's because that is when the lessee is made aware of the change in the future lease payments. Because of this change, the lessee has a larger lease liability because of the increase in the future lease payments. In this example, the increase in fixed payments is a result of a CPI increase.

The lessee shall remeasure the lease liability to reflect those revised lease payments only when there is a change in the cash flows (ie when the adjustment to the lease payments takes effect).