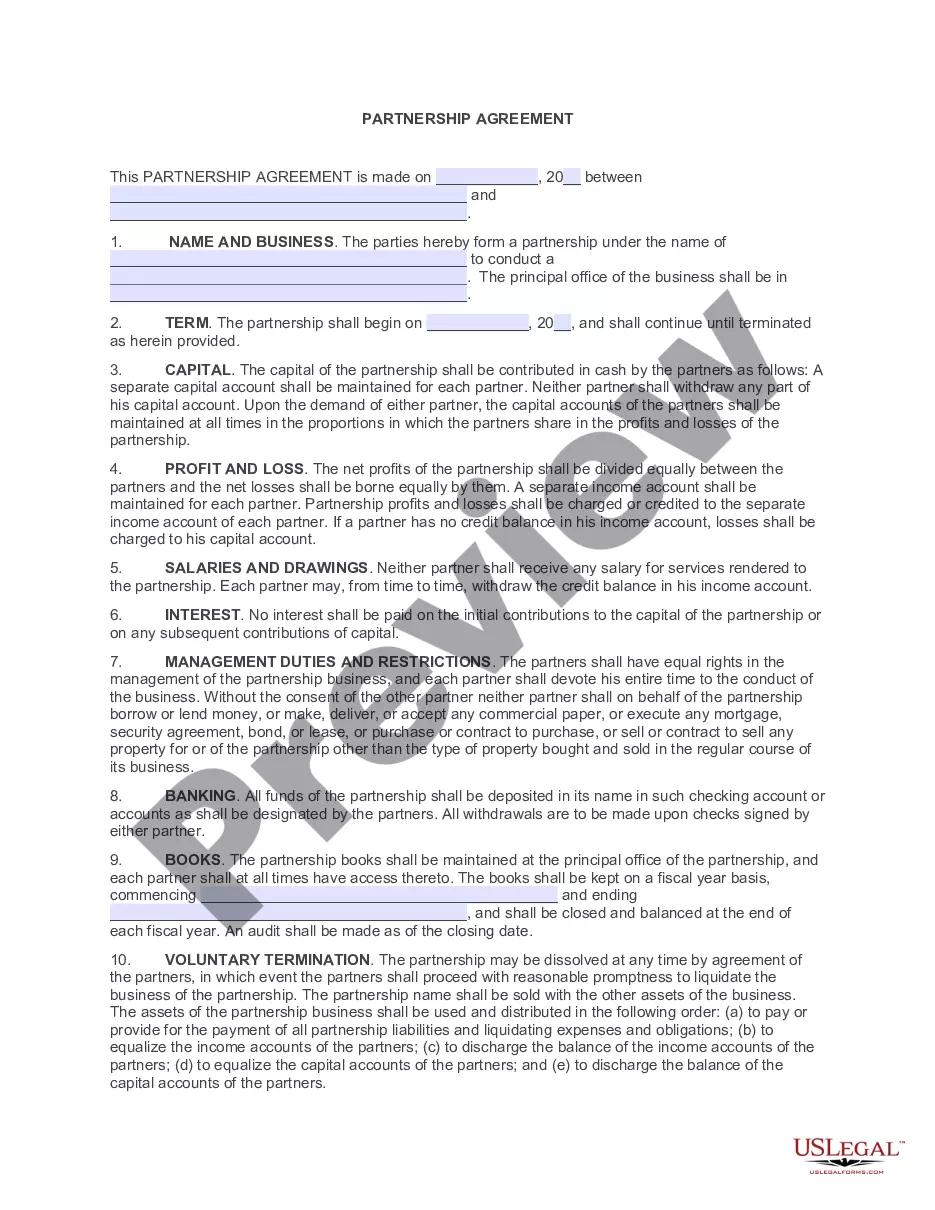

Virginia General Partnership for the Purpose of Farming

Description

How to fill out General Partnership For The Purpose Of Farming?

You might dedicate hours online exploring for the legal document template that satisfies the federal and state requirements you will require.

US Legal Forms offers thousands of legal documents that are evaluated by specialists.

You can easily download or print the Virginia General Partnership for the Purpose of Farming from this service.

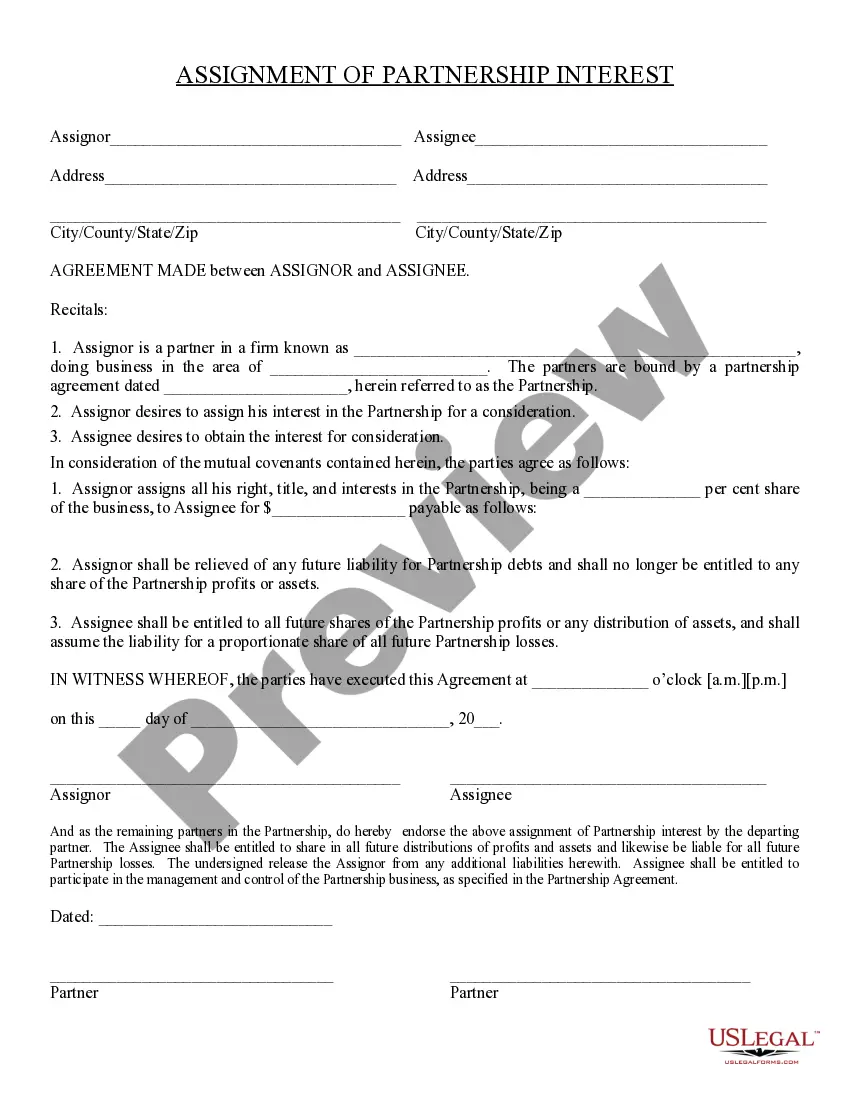

If available, use the Preview option to review the document template as well.

- If you currently possess a US Legal Forms account, you are capable of logging in and selecting the Acquire option.

- Afterward, you can fill out, modify, print, or sign the Virginia General Partnership for the Purpose of Farming.

- Every legal document template you purchase is yours indefinitely.

- To get another copy of any purchased form, visit the My documents tab and select the respective option.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, make sure that you have chosen the correct document template for the region/city of your choice.

- Review the form details to confirm you have selected the appropriate form.

Form popularity

FAQ

Pass-through entities that filed an election to pay the Pass-Through Business Alternative Income Tax must file Form PTE-100 and pay the tax due. They must also pro- vide Schedule PTE-K-1 to each member reporting the amount of the member's share of distributive proceeds and Pass-Through Business Alternative Income Tax.

The PTET is an optional tax that partnerships or New York S corporations may annually elect to pay on certain income for tax years beginning on or after January 1, 2021.

A PTE may file a composite return for only a portion of its qualified nonresident owners, provided that the business pays the pass-through entity withholding tax for any qualified nonresident owners who aren't included in the composite return.

You may qualify to claim this credit if:You're a farmer, grower, rancher, or someone else engaged in agricultural production for market; and.You have a soil conservation plan or resource management plan in place that your local soil and water conservation district has approved.

For taxable years beginning on or after January 1, 2021, and before January 1, 2026, qualifying pass-through entities (PTEs) may annually elect to pay an entity level state tax on income. Qualified taxpayers receive a credit for their share of the entity level tax, reducing their California personal income tax.

Residents of Virginia must file a Form 760. (A person is considered a resident if they have been living in Virginia for more than 183 days in a calendar year). An instruction booklet with return mailing address is also available. Nonresidents of Virginia must file a Form 763.

File Form 760PY to report the income attributable to your period of Virginia residency. File Form 763, the nonresident return, to report the Virginia source income received as a nonresident.

PTE tax is calculated by multiplying the entity's Minnesota source income by the highest Minnesota individual income tax rate, which is currently 9.85%. The PTE tax election is available for an entity's tax years beginning after December 31, 2020.

Download forms at . Order forms online through the Department's website or call (804) 440-2541.

The excise is imposed at a rate of 5% of the amount of the PTE's income that is subject to the Massachusetts personal income tax at the individual partner, shareholder or beneficiary level. Qualified members are allowed a personal income tax credit for 90% of their pro rata share of the PTE Excise paid by the PTE.