Virginia Owner Financing Contract for Moblie Home

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Owner Financing Contract For Moblie Home?

If you wish to finalize, acquire, or produce sanctioned document formats, utilize US Legal Forms, the most significant collection of legally recognized forms, accessible online.

Take advantage of the website's simple and user-friendly search to obtain the documents you need.

Various templates for commercial and individual purposes are categorized by types and states, or keywords.

Step 4. Once you have found the form you need, click the Buy now button. Choose the pricing plan you prefer and enter your information to create an account.

Step 5. Complete the purchase. You can use your credit card or PayPal account to finalize the transaction.

- Employ US Legal Forms to acquire the Virginia Owner Financing Contract for Mobile Home in just a few clicks.

- If you are already a US Legal Forms member, Log In to your account and click the Download button to access the Virginia Owner Financing Contract for Mobile Home.

- You can also retrieve forms you previously saved in the My documents section of your account.

- If this is your first experience with US Legal Forms, please follow the guidelines below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Preview option to review the form's details, and make sure to read the description.

- Step 3. If you are not satisfied with the form, use the Search bar at the top of the screen to locate alternative forms of the legal template.

Form popularity

FAQ

In a Virginia Owner Financing Contract for Mobile Home, the lender typically does not hold the deed. Instead, the seller acts as the lender, retaining the deed until the buyer completes all payments. Therefore, it is essential for buyers to understand their agreement with the seller to avoid any confusion regarding ownership rights.

If the buyer defaults on a Virginia Owner Financing Contract for Mobile Home, the seller has the right to initiate foreclosure proceedings. This can involve reclaiming the property and selling it to recover lost payments. Buyers should be aware of the consequences and the importance of maintaining timely payments to avoid such scenarios.

One downside of a Virginia Owner Financing Contract for Mobile Home is the potential for higher interest rates compared to traditional loans. Additionally, sellers might face the risk of buyer default, which could lead to financial loss and the need to reclaim the property. It is crucial for both buyers and sellers to thoroughly understand these risks before proceeding.

In a Virginia Owner Financing Contract for Mobile Home, the seller retains the deed until the buyer fulfills the payment terms. This situation creates a secure investment for the seller while allowing the buyer to enjoy the property. Thus, the seller has the authority to reclaim the property if the buyer defaults on payments, ensuring peace of mind for both parties.

Many banks hesitate to finance mobile homes because they often classify them as personal property rather than real estate. This classification can lead to higher risks for lenders due to depreciation and lower resale values. Additionally, the complexities of mobile home financing may deter traditional lenders from offering loans. By utilizing a Virginia Owner Financing Contract for Mobile Home, buyers can bypass bank hurdles and negotiate favorable terms directly with sellers, providing an accessible alternative for mobile home financing.

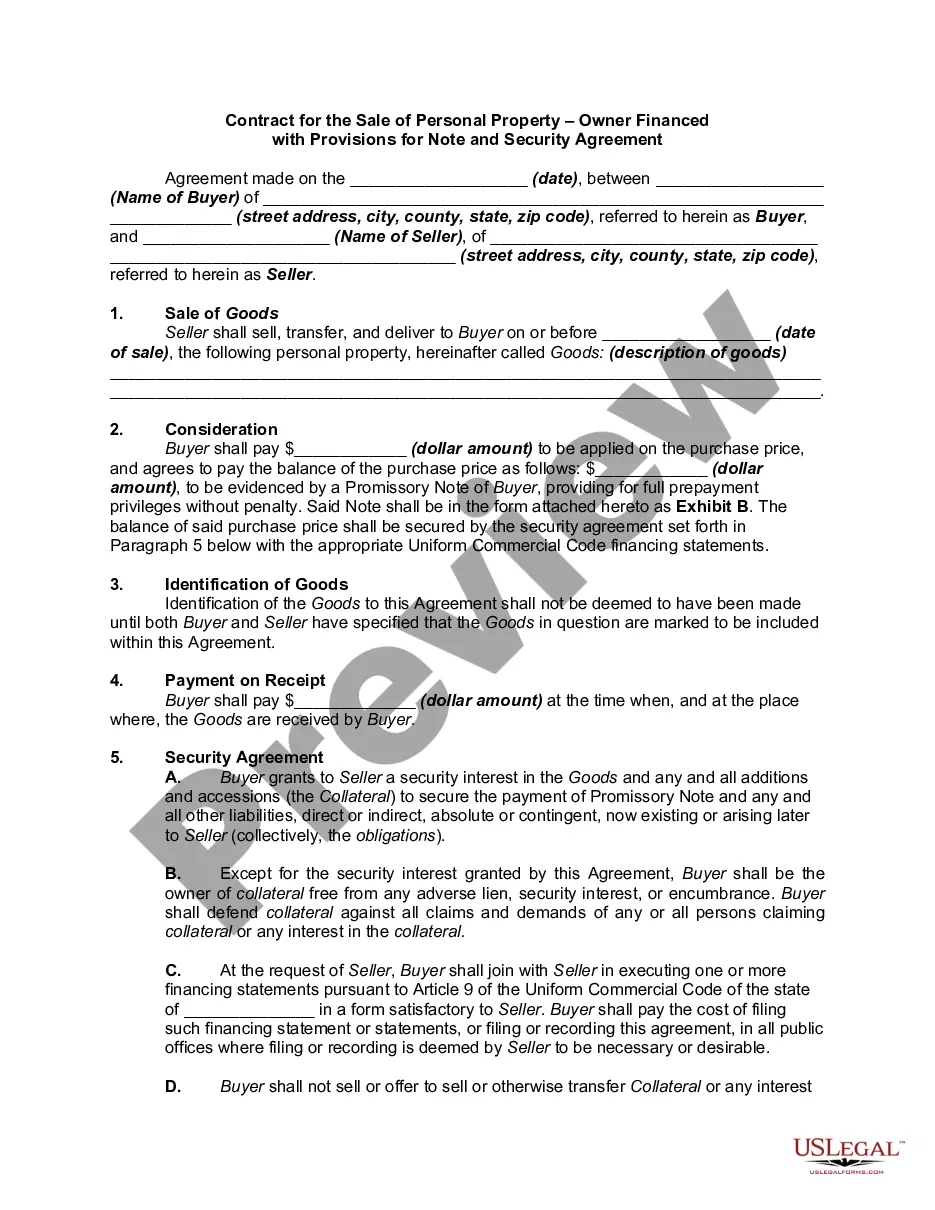

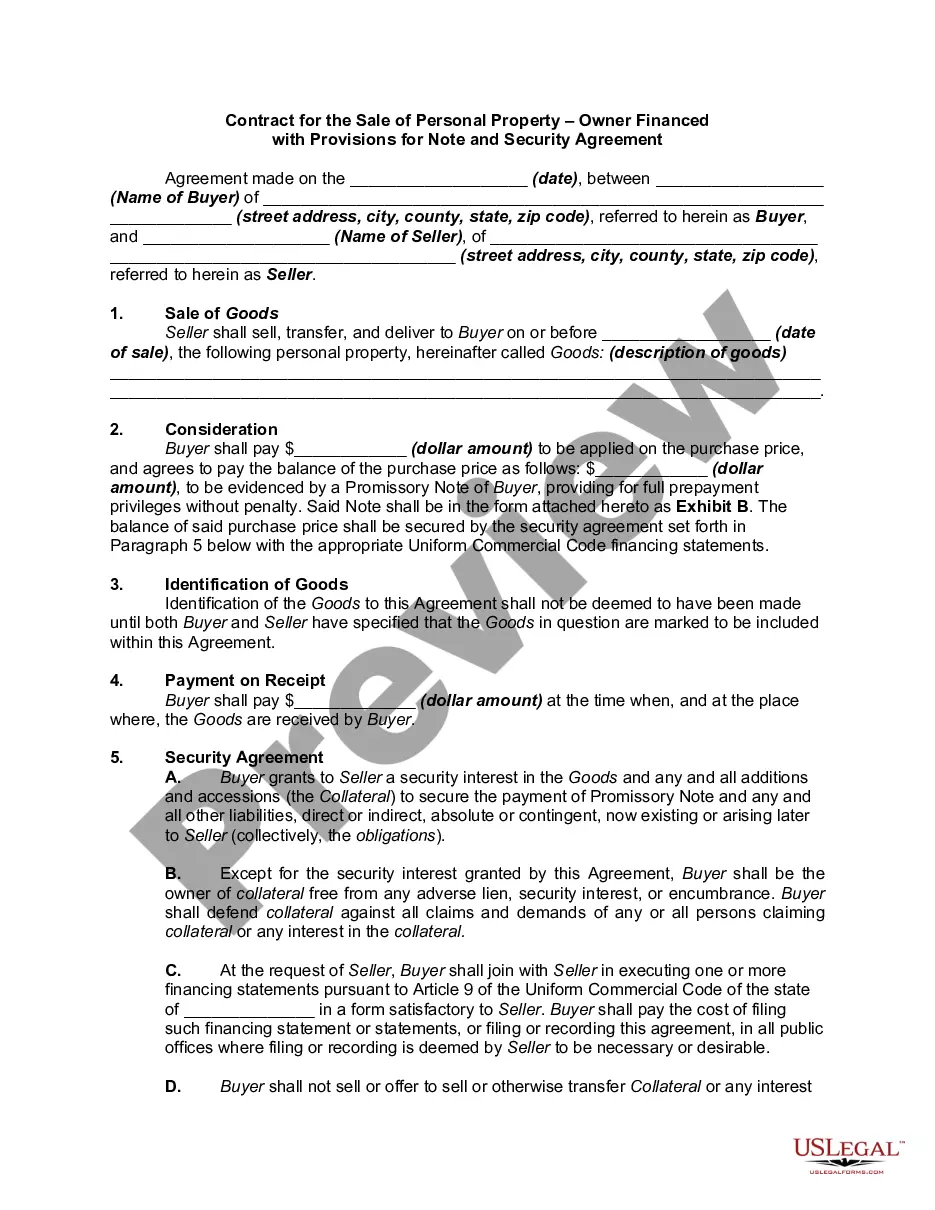

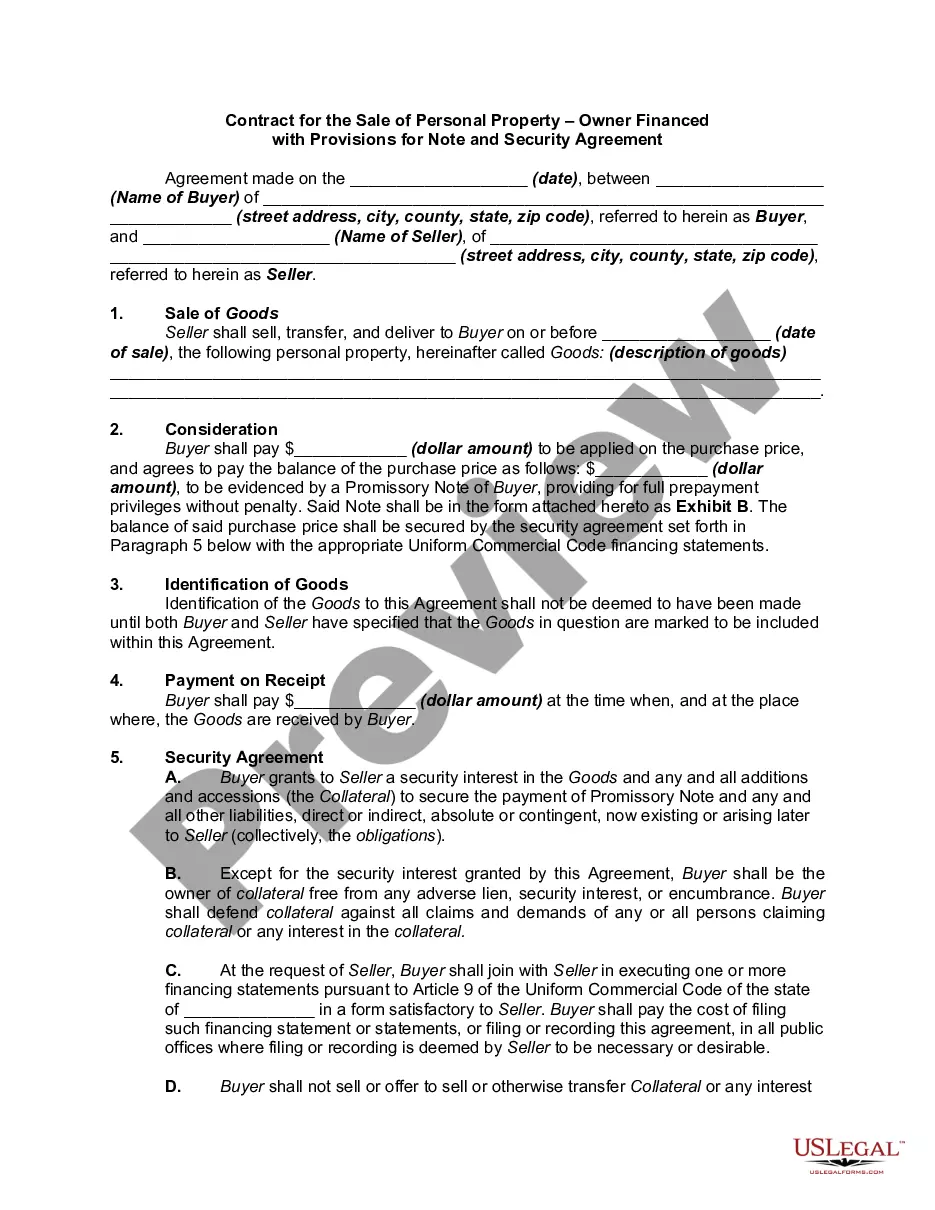

Typical terms for seller financing on a mobile home in Virginia may include a down payment of 10% to 20%, an interest rate that ranges from 5% to 10%, and a repayment schedule that spans 5 to 30 years. Additional terms might cover late fees, prepayment options, and responsibilities for maintenance and property taxes. These terms can vary, so it is important to negotiate and document them thoroughly in a Virginia Owner Financing Contract for Mobile Home. US Legal Forms can assist you in drafting an agreement that reflects your specific needs.

To owner finance a mobile home, you must first negotiate the terms with the buyer, including payment schedule and interest rates. It’s advisable to use a formal agreement outlining these details, like a Virginia Owner Financing Contract for Mobile Home. This contract should provide clarity and protection for both parties involved.

Financing a mobile home can be more challenging compared to traditional homes due to the perceived risk by lenders. However, with a solid financial background, you can still find viable options. Additionally, exploring various financing methods, such as a Virginia Owner Financing Contract for Mobile Home, can simplify the process.

Most lenders prefer to finance mobile homes that are manufactured after 1976 due to safety and quality standards. If your mobile home is newer, it will be easier to secure financing. Age can impact your financing options and terms. Reviewing a Virginia Owner Financing Contract for Mobile Home is essential if you're purchasing an older unit.

To buy a mobile home, lenders typically look for a credit score of at least 620. However, some may consider lower scores if you have a solid income and a down payment. A stronger credit profile can lead to better financing options. Understanding the requirements can help you prepare for a Virginia Owner Financing Contract for Mobile Home.