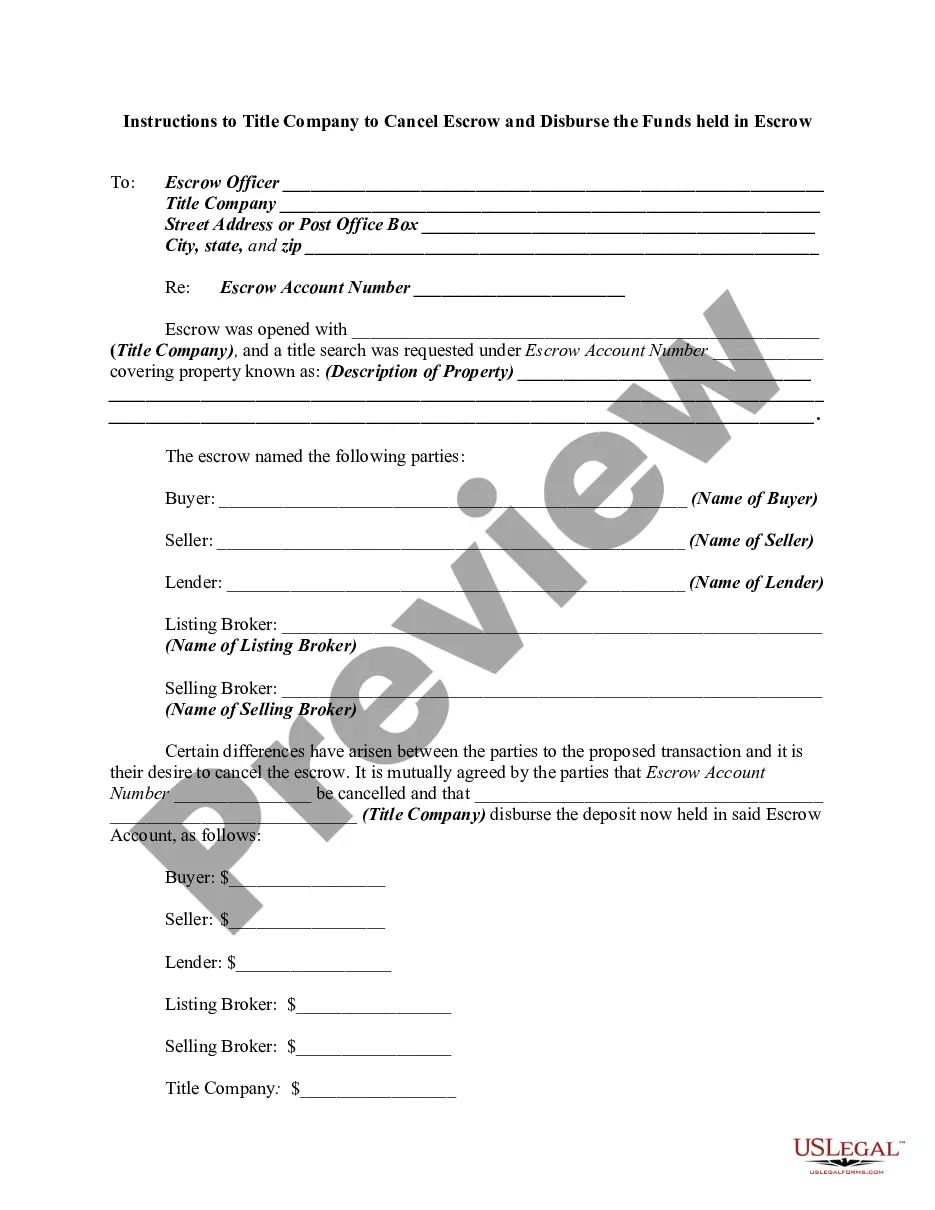

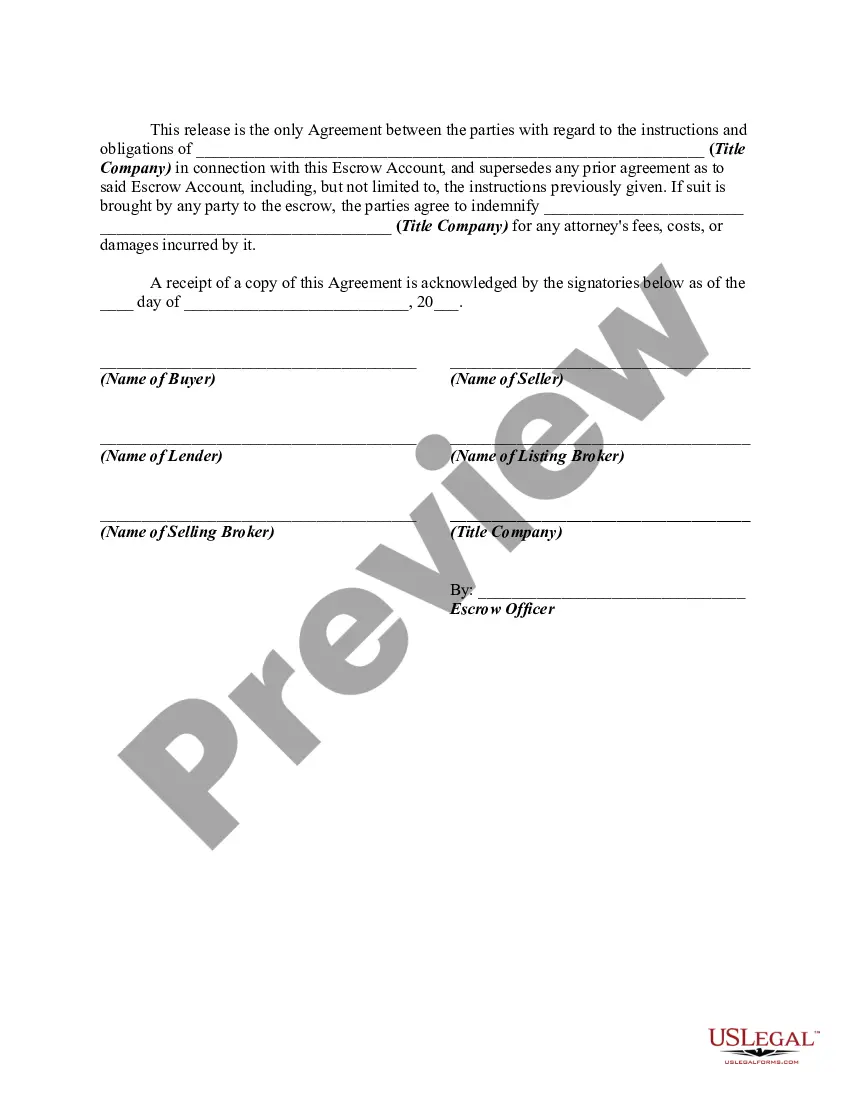

An escrow may be terminated according to the escrow agreement when the parties have performed the conditions of the escrow and the escrow agent has delivered the items to the parties entitled to them according to the escrow instructions. An escrow may be prematurely terminated by cancellation after default by one of the parties or by mutual consent. An escrow may also be terminated at the end of a specified period if the parties have not completed it within that time and have not extended the time for performance.

Canceling an escrow account for taxes involves terminating a financial arrangement made with a mortgage lender. Under normal circumstances, homeowners contribute a portion of their monthly mortgage payment into an escrow account to cover property taxes and insurance. However, canceling an escrow account for taxes means that homeowners take on the responsibility of paying their property taxes directly to the tax collector, instead of routing the funds through the escrow account. This process is usually initiated by submitting a formal request to the mortgage lender. By canceling an escrow account for taxes, homeowners gain control over their property tax payments, allowing them to have a direct relationship with the tax collector. This provides individuals with greater flexibility and the freedom to manage their tax payments according to their financial situation. However, canceling an escrow account implies taking on the responsibility of timely tax payments, as failure to pay may result in penalties or liens against the property. There are different types of cancel escrow accounts for taxes that homeowners can explore, based on their specific needs and circumstances. 1. Voluntarily Canceling Escrow: This involves homeowners proactively deciding to terminate the escrow account for taxes. They typically consider factors such as financial stability, tax planning preferences, or potential savings on interest or insurance costs. 2. Automatically Canceling Escrow: In some cases, an escrow account may be canceled automatically based on certain conditions. For instance, if the homeowner reaches a loan-to-value ratio below 80% on their mortgage, lenders might eliminate the escrow account. 3. Refinancing: Homeowners can cancel escrow accounts for taxes by refinancing their mortgage. This involves paying off the existing loan and obtaining a new one with different terms and conditions, including the choice to eliminate the escrow arrangement. 4. Account Adjustment: Some homeowners may opt for account adjustment where they choose to keep the escrow account for taxes but adjust the monthly payment amount. This adjustment can be done in collaboration with the mortgage lender to align the escrow funds more accurately with the property tax obligations. Canceling an escrow account for taxes can be a strategic decision for homeowners seeking more control over their finances. However, it is crucial to consider the potential drawbacks, like the responsibility of ensuring timely tax payments and maintaining sufficient funds to cover property tax bills. Ultimately, individuals should assess their financial situation, consult with mortgage lenders, and weigh the pros and cons before deciding to cancel an escrow account for taxes.