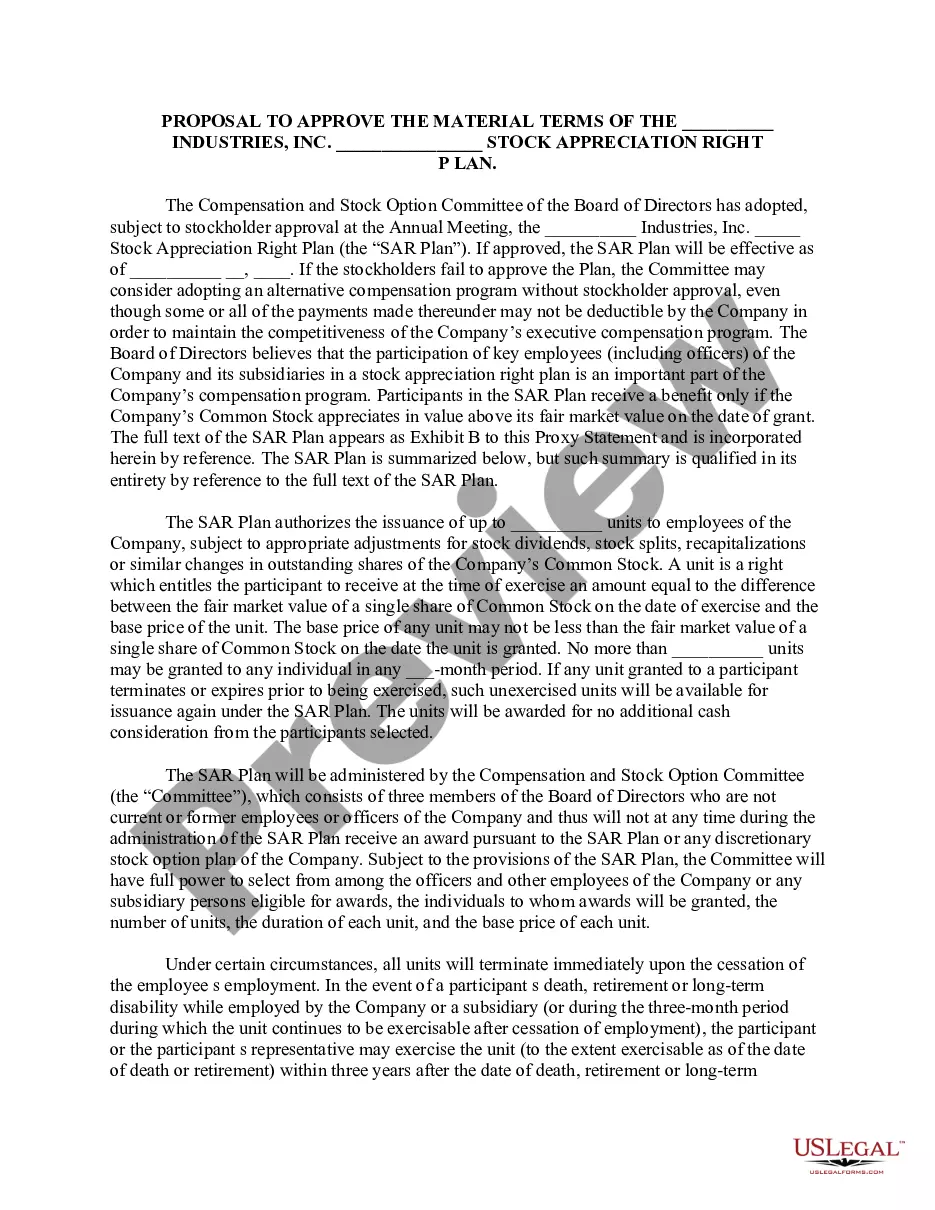

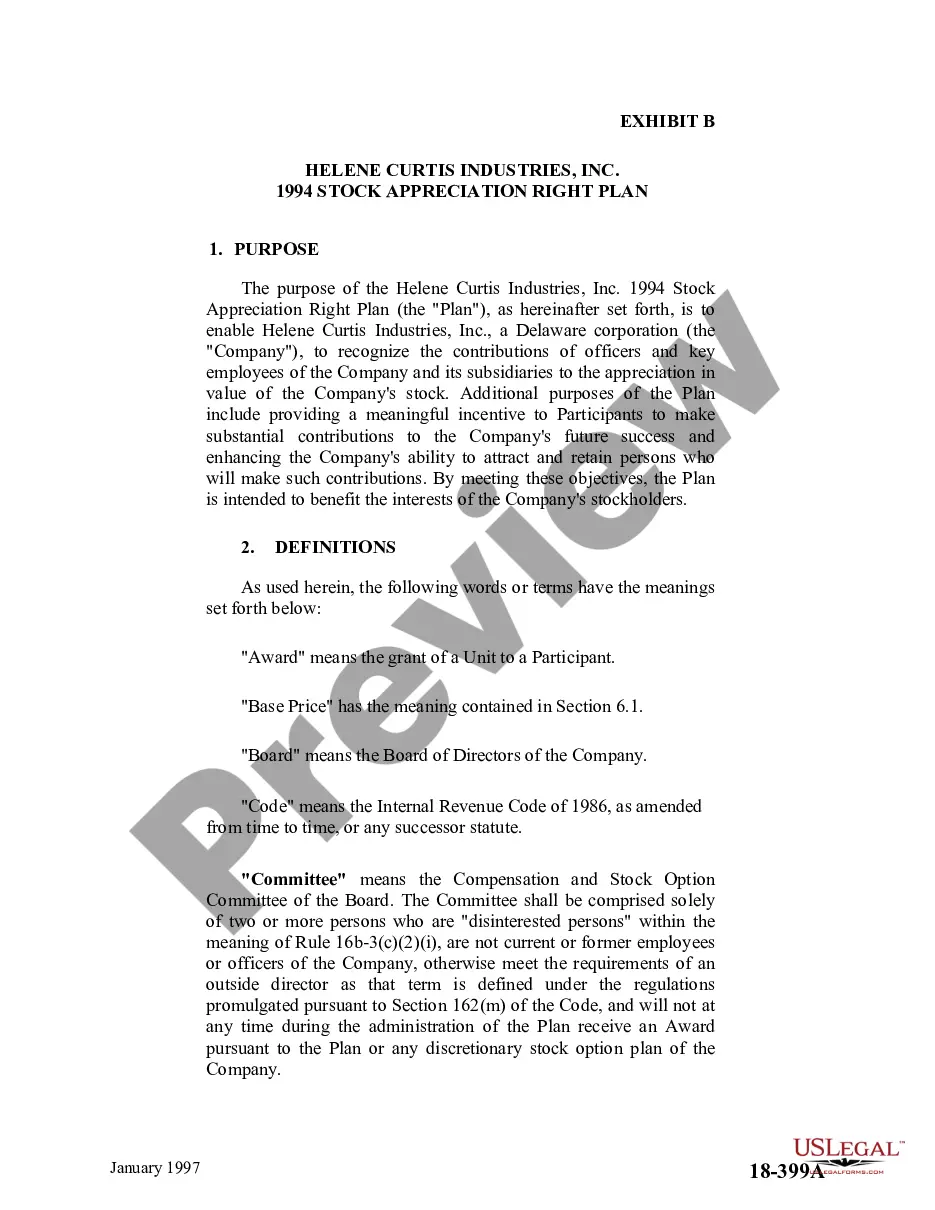

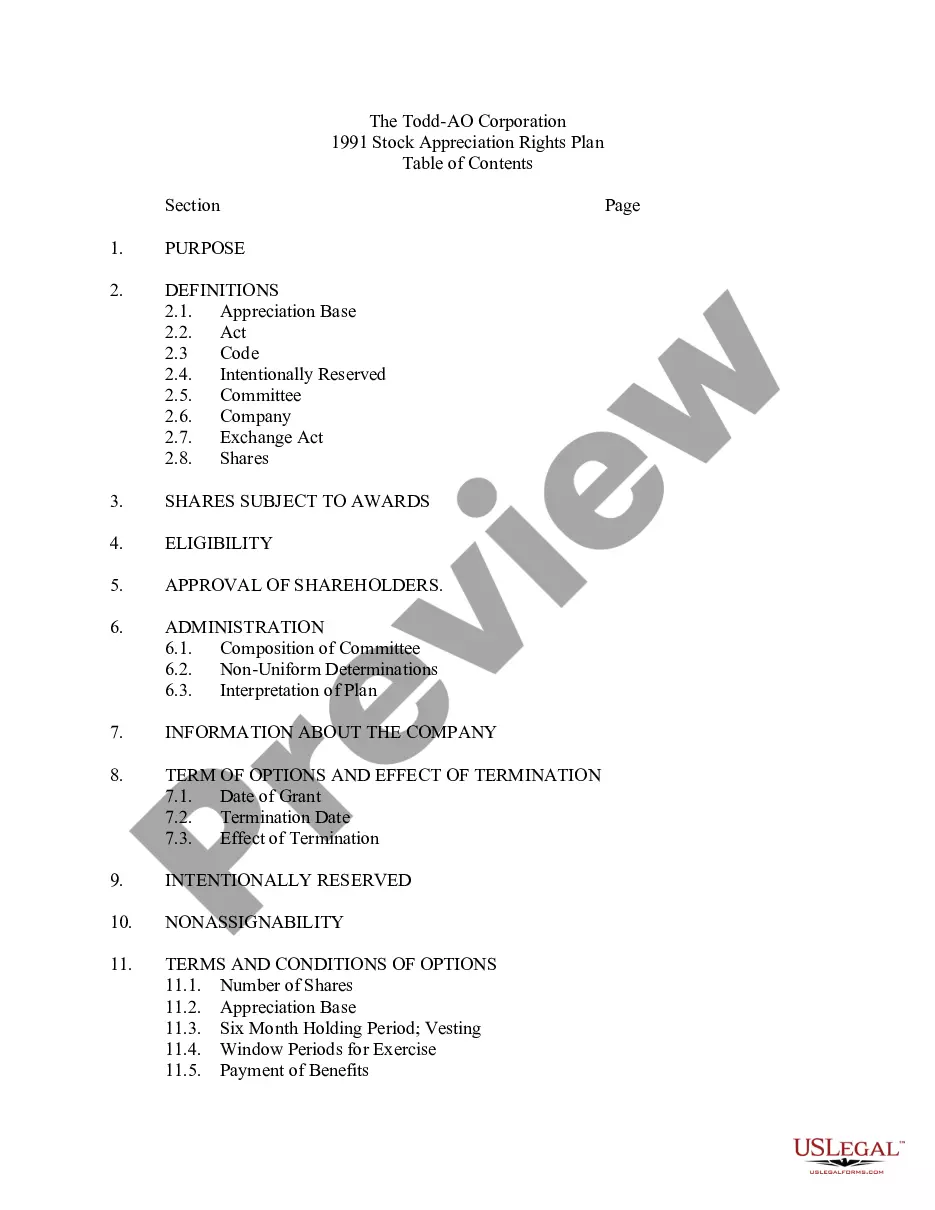

18-400D 18-400D . . . Share Appreciation Rights Plan under which stock option committee determines to whom units are awarded, number of units to be awarded and terms of such units. On grant date, committee assigns each unit a base value which cannot be less than market value of share of common stock on that date. Each award becomes exercisable with respect to 25% of units awarded on each of first four anniversaries of grant date, provided grantee has been continually employed full-time by corporation or subsidiary. Units may be exercised, to extent vested, at any time until five years after grant date. Upon exercise of vested units, grantee is entitled to receive net appreciation of such units in cash or in shares of common stock, as determined by committee

Tennessee Share Appreciation Rights Plan with amendment

Category:

State:

Multi-State

Control #:

US-CC-18-400D

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Share Appreciation Rights Plan With Amendment?

Choosing the right authorized papers template could be a have difficulties. Needless to say, there are plenty of layouts available on the net, but how can you get the authorized develop you need? Utilize the US Legal Forms internet site. The support offers a huge number of layouts, like the Tennessee Share Appreciation Rights Plan with amendment, which can be used for enterprise and personal requirements. Every one of the forms are examined by specialists and satisfy state and federal demands.

In case you are presently listed, log in to the accounts and then click the Acquire key to find the Tennessee Share Appreciation Rights Plan with amendment. Make use of your accounts to appear throughout the authorized forms you have bought earlier. Go to the My Forms tab of your accounts and obtain another copy in the papers you need.

In case you are a new customer of US Legal Forms, allow me to share simple recommendations for you to adhere to:

- Initially, make certain you have selected the right develop for the area/state. It is possible to look through the shape making use of the Preview key and look at the shape information to make certain this is basically the best for you.

- In case the develop will not satisfy your requirements, use the Seach field to find the proper develop.

- Once you are certain that the shape is acceptable, click the Purchase now key to find the develop.

- Pick the rates plan you need and enter in the essential info. Create your accounts and buy an order with your PayPal accounts or charge card.

- Choose the document formatting and obtain the authorized papers template to the system.

- Complete, revise and produce and sign the received Tennessee Share Appreciation Rights Plan with amendment.

US Legal Forms will be the greatest catalogue of authorized forms that you will find different papers layouts. Utilize the service to obtain skillfully-manufactured paperwork that adhere to status demands.

Form popularity

FAQ

Stock Appreciation Rights plans do not result in equity dilution because actual shares are not being transferred to the employee. Participants do not become owners. Instead, they are potential cash beneficiaries in the appreciation of the underlying company value.

However, when a stock appreciation right is exercised, the employee does not have to pay to acquire the underlying security. Instead, the employee receives the appreciation in value of the underlying security, which would equal the current market value less the grant price.

How do I value it? For purposes of financial disclosure, you may value a stock appreciation right based on the difference between the current market value and the grant price. This formula is: (current market value ? grant price) x number of shares = value.

A Stock Appreciation Right (SAR) is an award which provides the holder with the ability to profit from the appreciation in value of a set number of shares of company stock over a set period of time.

A ?Stock Appreciation Right? is the right to receive a payment from the Company in an amount equal to the ?Spread,? which is defined as the excess of the Fair Market Value (as defined in Plan) of one share of common stock, $1.00 par value (the ?Stock?) of the Company at the Exercise Date (as defined below) over a ...

Stock Appreciation Right (SAR) entitles an employee, who is a shareholder in a company, to a cash payment proportionate to the appreciation of stock traded on a public exchange market. SAR programs provide companies with the flexibility to structure the compensation scheme in a way that suits their beneficiaries.

A SAR is very similar to a stock option, but with a key difference. When a stock option is exercised, an employee has to pay the grant price and acquire the underlying security. However, when a SAR is exercised, the employee does not have to pay to acquire the underlying security.

Stock Appreciation Right (SAR) entitles an employee, who is a shareholder in a company, to a cash payment proportionate to the appreciation of stock traded on a public exchange market. SAR programs provide companies with the flexibility to structure the compensation scheme in a way that suits their beneficiaries.