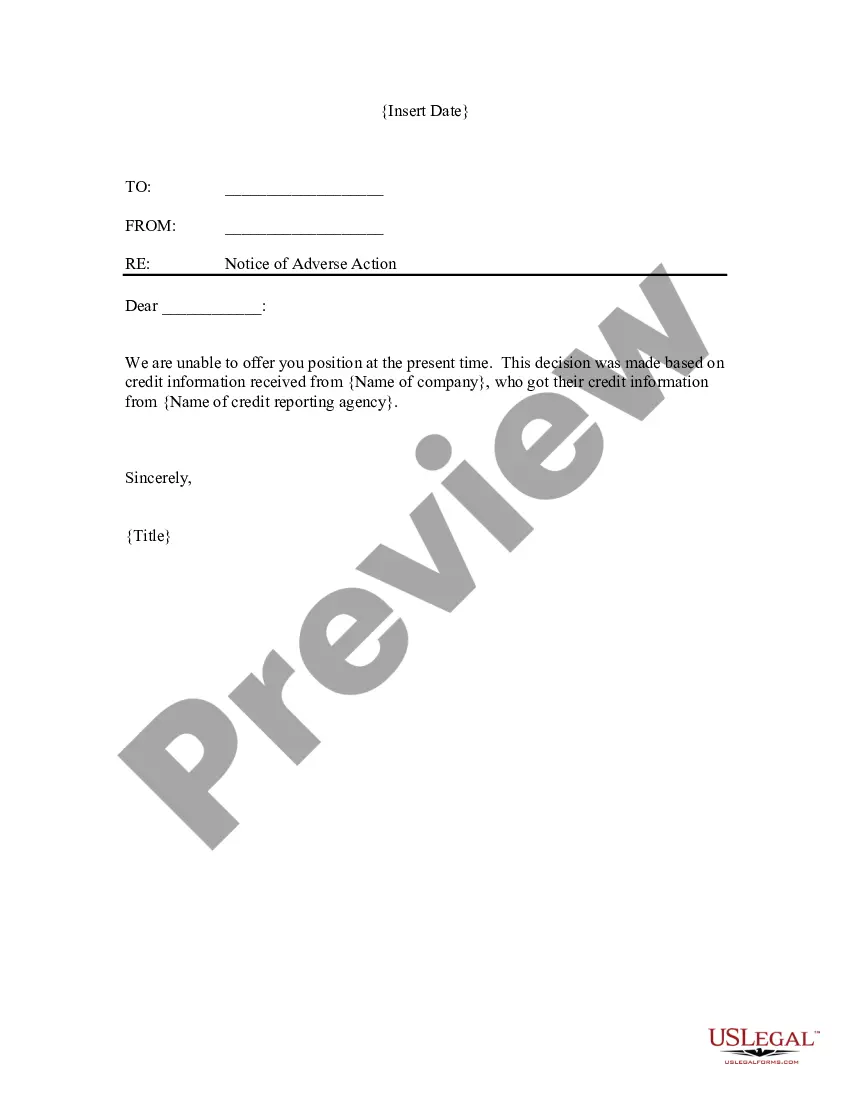

Tennessee Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report

Description

How to fill out Notice Of Adverse Action - Non-Employment - Due To Consumer Investigative Report?

US Legal Forms - one of the most considerable collections of legal documents in the United States - provides a diverse selection of legal form templates that you can download or print.

By utilizing the website, you will find thousands of forms for business and personal purposes, categorized by types, states, or keywords. You can access the latest types of documents like the Tennessee Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report in just a few minutes.

If you have a monthly subscription, Log In and download the Tennessee Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report from the US Legal Forms library. The Download button will appear on each form you view.

Complete the transaction. Use your Visa, Mastercard, or PayPal account to finalize the purchase.

Select the format and download the form to your device. Edit. Fill out, modify, print, and sign the downloaded Tennessee Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report. Each template you save to your account does not have an expiration date and belongs to you indefinitely. If you need to download or print another copy, simply go to the My documents section and click on the desired form. Gain access to the Tennessee Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report through US Legal Forms, one of the largest archives of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal requirements.

- Ensure you have selected the correct form for your city/state.

- Click the Preview button to review the content of the form.

- Examine the form description to confirm that you have chosen the right form.

- If the form does not meet your requirements, utilize the Search box at the top of the screen to find a suitable one.

- Once you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, select the pricing plan you want and provide your information to register for an account.

Form popularity

FAQ

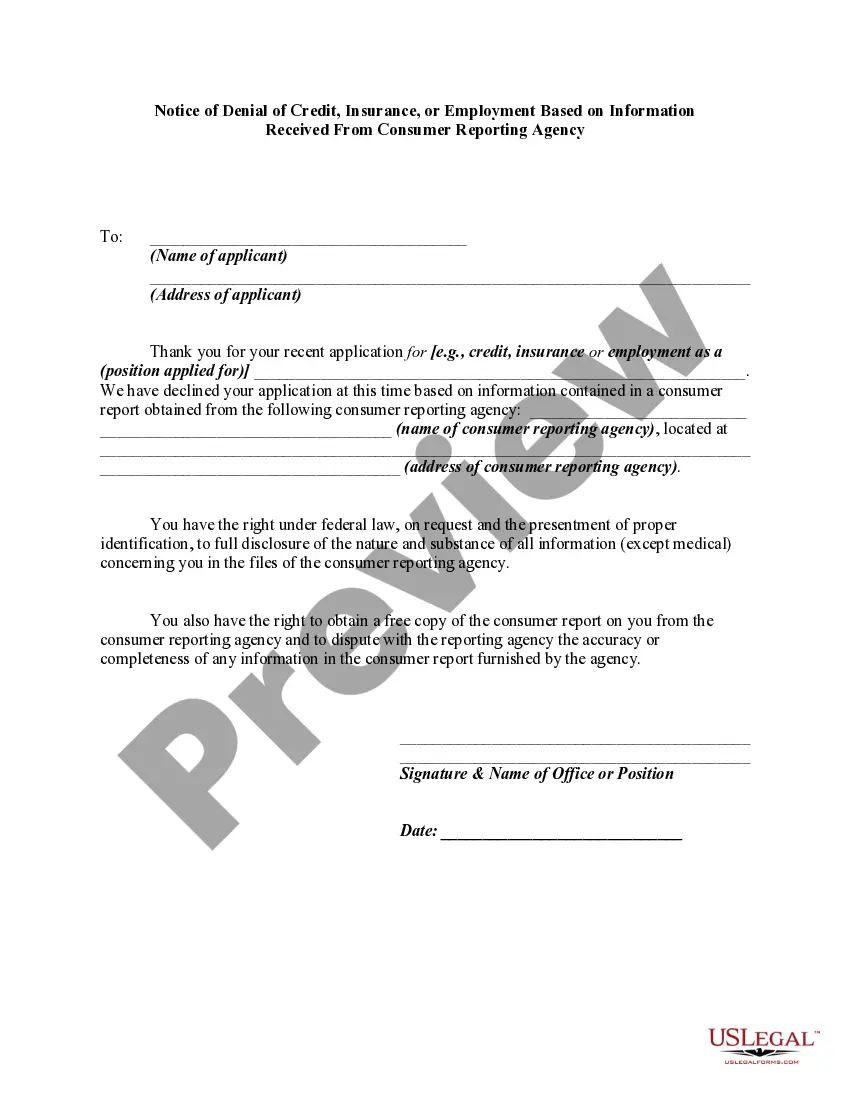

Adverse action is defined in the Equal Credit Opportunity Act and the FCRA to include: a denial or revocation of credit. a refusal to grant credit in the amount or terms requested. a negative change in account terms in connection with an unfavorable review of a consumer's account 5 U.S.C.

adverse action might also occur at pointofsale transactions where an account transaction is denied in real time. Notably, the ECOA does not consider an adverse action to have occurred where an action or forbearance on an account is taken in connection with inactivity, default, or delinquency as to that account.

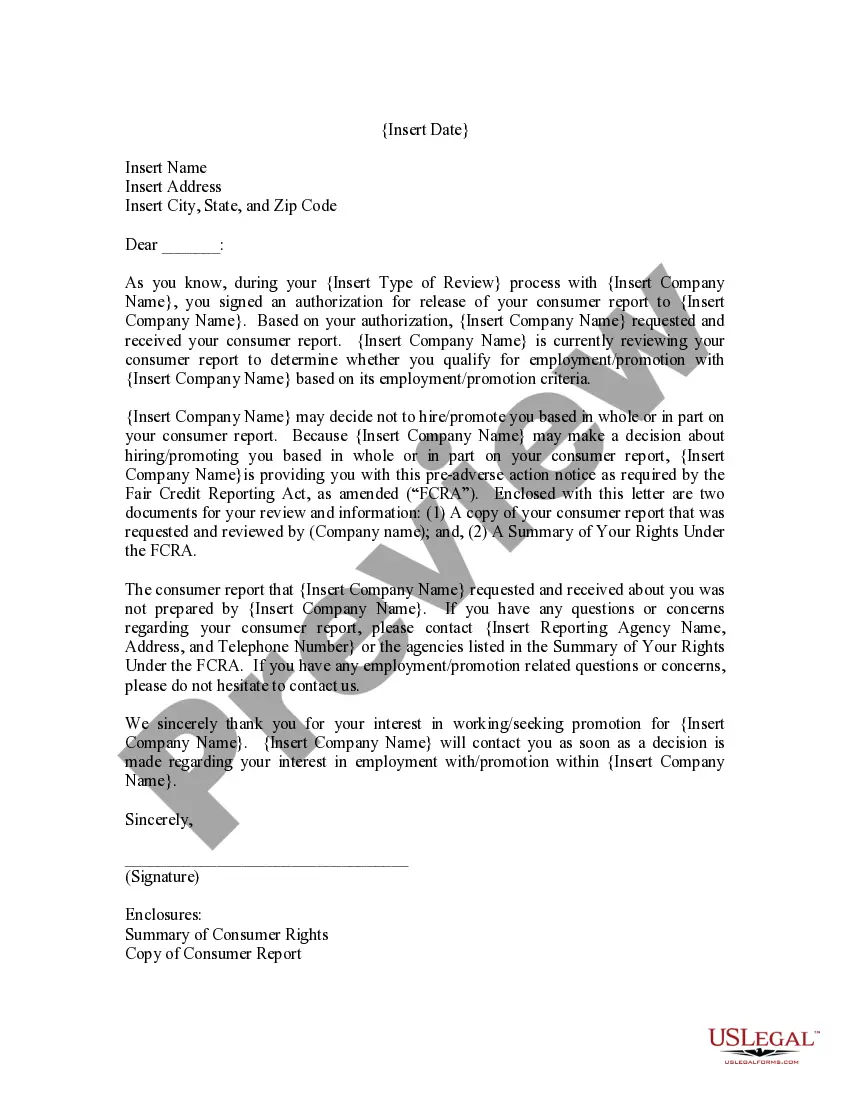

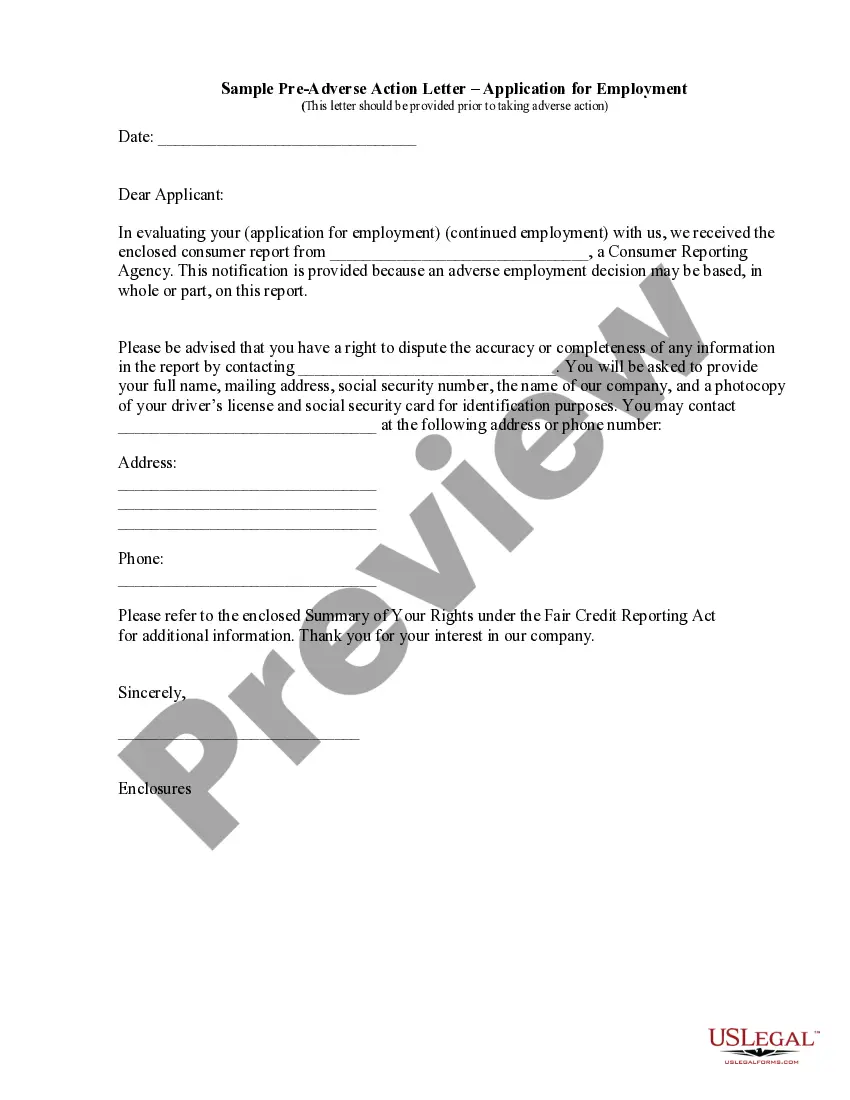

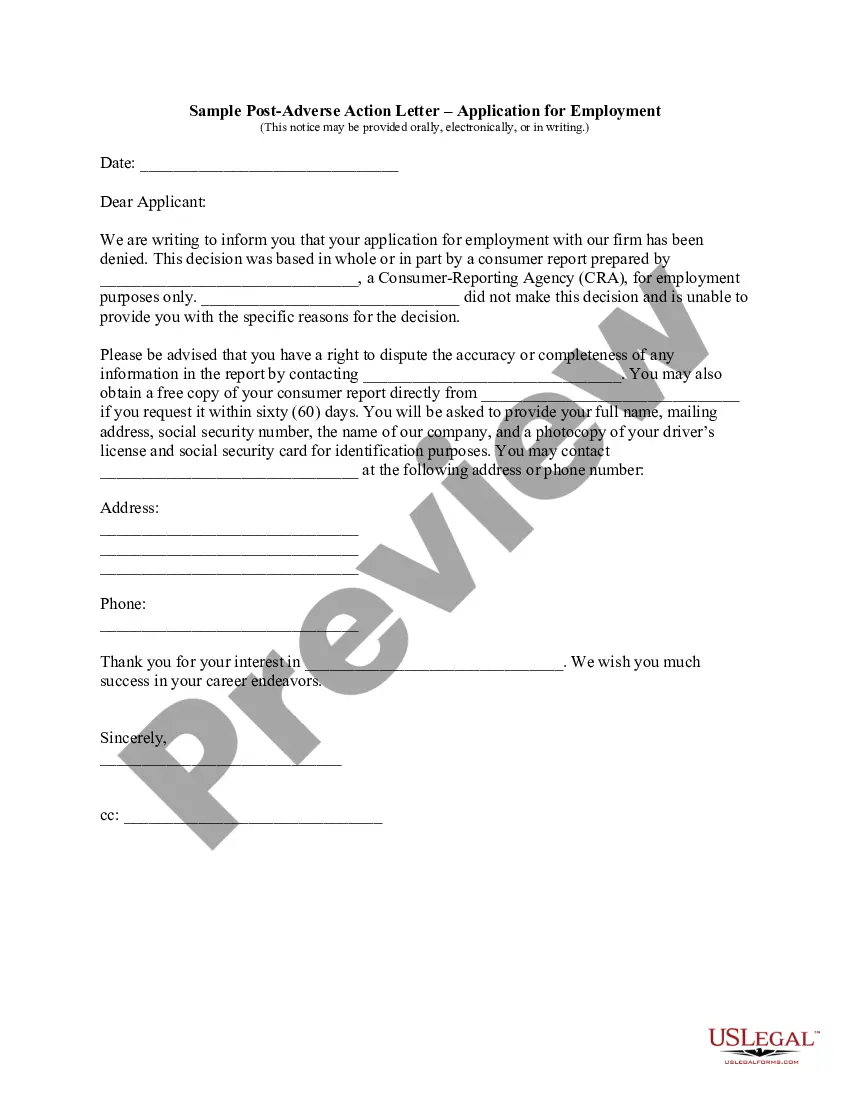

If you're an organization that processes credit applications, it is your duty to provide an Adverse Action Notice if a consumer is denied credit. And you've got to provide it within 30 days of receiving a credit application.

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.

Employers should be aware that California law generally limits an investigative consumer report inquiry regarding public records to the past seven years (10 years for bankruptcy filings).

An investigative consumer report offers insight employers use to gain a better understanding of a person's character through interviews. These are often in the form of personal and/or professional references. When deciding which might be best, ask what information are you trying to gain.

A consumer report is a collection of documents that may include credit reports, criminal and other public records such as bankruptcy filings, and records of civil court procedures and judgments. Increasingly, these records also include your activity on social media, such as Twitter and Facebook.

The following are examples of adverse actions employers might take: discharging the worker; demoting the worker; reprimanding the worker; committing harassment; creating a hostile work environment; laying the worker off; failing to hire or promote a worker; blacklisting the worker; transferring the worker to another

As a rule of thumb, the distinction between the two types of investigations can be thought of as simply verifying the specific facts about education, employment or other information the applicant has provided to the employer ("consumer report") versus obtaining more general character or personal information through

Essentially, personal or professional reference verification, and employment verification that stray beyond the realm of facts and into personal character assessments and opinions are considered Investigative Consumer Reports.