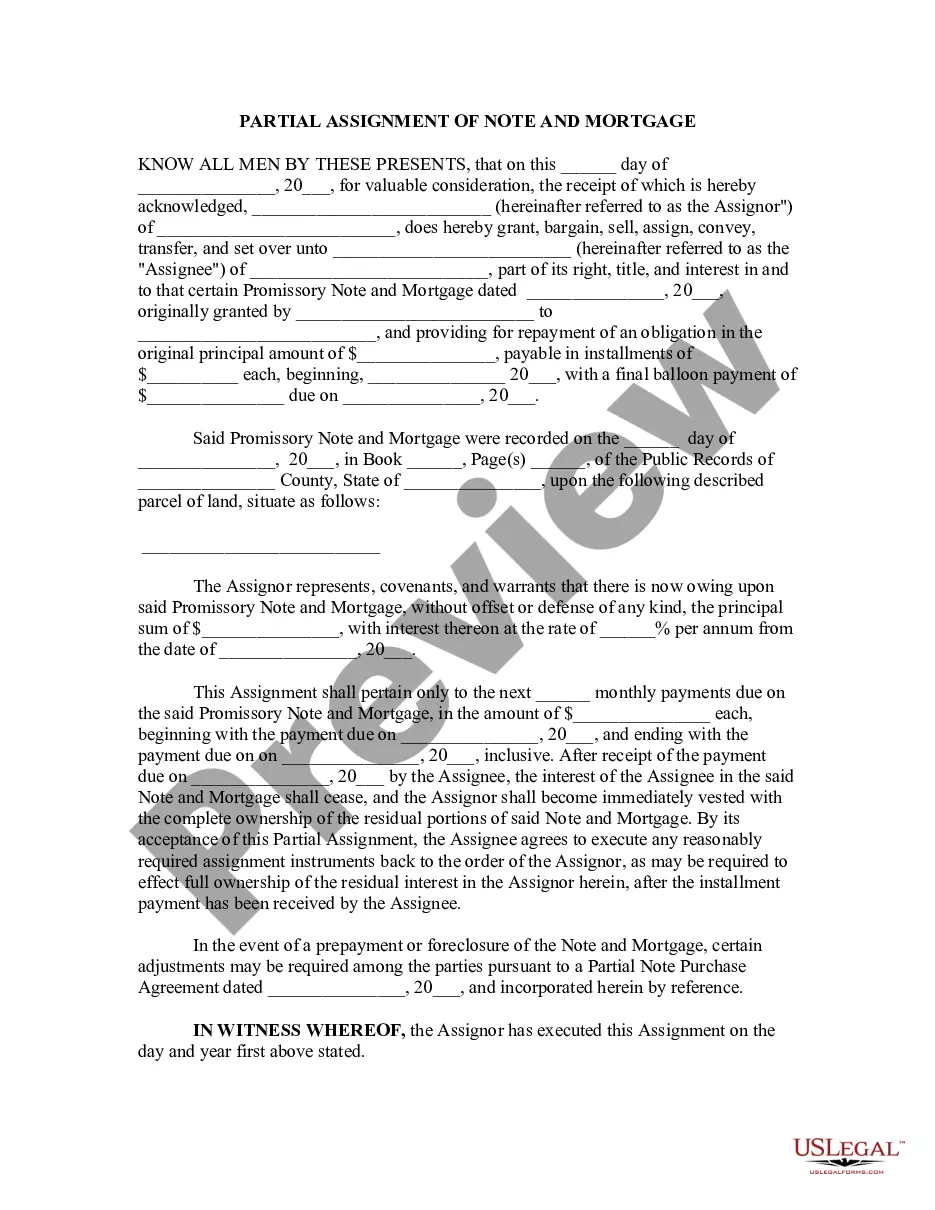

Tennessee Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Partial Assignment Of Life Insurance Policy As Collateral?

You can devote hrs online trying to find the legal document template which fits the federal and state needs you want. US Legal Forms gives thousands of legal forms that are examined by professionals. You can easily down load or print out the Tennessee Partial Assignment of Life Insurance Policy as Collateral from our assistance.

If you currently have a US Legal Forms bank account, you may log in and click on the Obtain switch. Next, you may total, revise, print out, or indication the Tennessee Partial Assignment of Life Insurance Policy as Collateral. Each and every legal document template you get is yours for a long time. To acquire another copy of any obtained form, visit the My Forms tab and click on the related switch.

If you use the US Legal Forms web site the first time, follow the simple instructions below:

- Initially, ensure that you have selected the right document template for your area/town of your liking. Browse the form outline to make sure you have chosen the appropriate form. If accessible, take advantage of the Review switch to search through the document template too.

- If you want to find another model from the form, take advantage of the Research area to discover the template that meets your requirements and needs.

- Once you have identified the template you desire, click Buy now to continue.

- Find the prices strategy you desire, enter your credentials, and sign up for a free account on US Legal Forms.

- Complete the financial transaction. You can utilize your credit card or PayPal bank account to cover the legal form.

- Find the format from the document and down load it to the device.

- Make changes to the document if required. You can total, revise and indication and print out Tennessee Partial Assignment of Life Insurance Policy as Collateral.

Obtain and print out thousands of document web templates using the US Legal Forms Internet site, that provides the largest variety of legal forms. Use skilled and state-particular web templates to deal with your business or individual requirements.

Form popularity

FAQ

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

A life insurance policy can be assigned when rights of one person are transferred to another. The rights to your insurance policy can be transferred to someone else for various reasons. The process is known as assignment.

Collateral assignment, on the other hand, is a temporary and often revocable arrangement. The policyholder retains ownership and control over the policy but agrees that the lender has a claim to a part of the death benefit if the loan is not repaid.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.