South Dakota Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

Choosing the right legitimate document web template might be a battle. Naturally, there are tons of layouts available on the Internet, but how do you get the legitimate kind you want? Utilize the US Legal Forms internet site. The services delivers thousands of layouts, like the South Dakota Challenge to Credit Report of Experian, TransUnion, and/or Equifax, that can be used for organization and personal requirements. All of the types are examined by professionals and satisfy federal and state requirements.

Should you be presently listed, log in for your profile and then click the Acquire option to get the South Dakota Challenge to Credit Report of Experian, TransUnion, and/or Equifax. Use your profile to search throughout the legitimate types you have acquired formerly. Proceed to the My Forms tab of your profile and get one more version of your document you want.

Should you be a brand new customer of US Legal Forms, listed here are basic instructions so that you can stick to:

- Initial, make sure you have selected the correct kind for your personal metropolis/area. It is possible to look through the form using the Preview option and look at the form explanation to ensure this is the best for you.

- In the event the kind will not satisfy your requirements, make use of the Seach industry to discover the proper kind.

- When you are certain the form is acceptable, click on the Acquire now option to get the kind.

- Opt for the rates program you need and type in the needed information. Create your profile and pay for an order making use of your PayPal profile or Visa or Mastercard.

- Opt for the submit structure and down load the legitimate document web template for your product.

- Complete, revise and print and indicator the received South Dakota Challenge to Credit Report of Experian, TransUnion, and/or Equifax.

US Legal Forms is the biggest catalogue of legitimate types that you can find numerous document layouts. Utilize the service to down load skillfully-created paperwork that stick to status requirements.

Form popularity

FAQ

You can only have one dispute investigation open at a time, but it can contain as many items as you need to dispute.

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

Contact each of the three major credit bureaus ? Equifax, Experian and TransUnion ? individually to freeze your credit: Equifax: Call 800-349-9960 or go online. ... Experian: Go online to initiate, or for information call 888?397?3742. ... TransUnion: Call 888-909-8872 or go online.

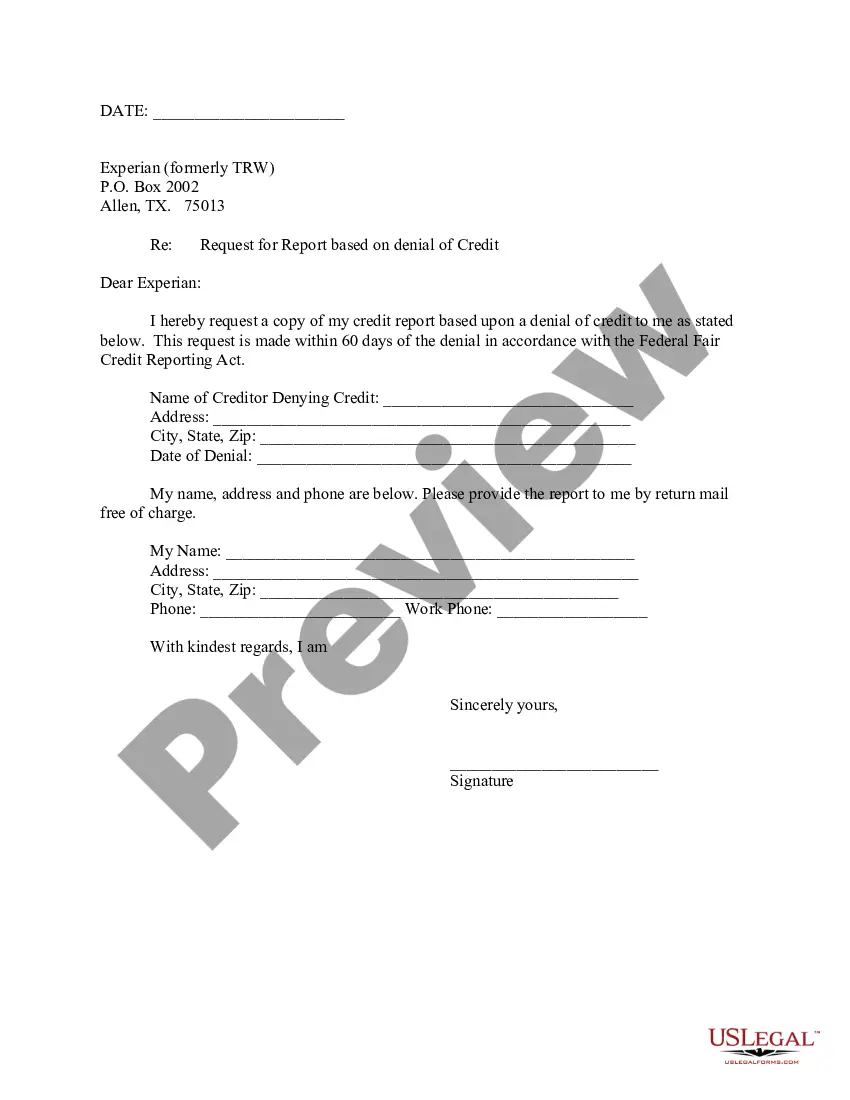

A dispute with additional relevant information can also be submitted by mail to Experian at P.O. Box 4500, Allen, TX 75013.

If a credit bureau has made a mistake on your report ? if you don't recognize the account or a paid account shows as unpaid, for example ? gather documentation supporting your case. Then, file a dispute by using the credit bureau's online process, by phone or by mail. The bureau has 30 days to respond.

You submit an investigation request (dispute). If you believe that an item contained in your TransUnion credit report is inaccurate or needs updating, send TransUnion a request for investigation or request to change information. You can start your investigation online. You can also submit a dispute by phone or mail.

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

You submit an investigation request (dispute). If you believe that an item contained in your TransUnion credit report is inaccurate or needs updating, send TransUnion a request for investigation or request to change information. You can start your investigation online. You can also submit a dispute by phone or mail.