This form is an Assumption Agreement. The form provides that the grantee will assume a lien on property described in the agreement. The assumption will become effective on the date provided in the agreement.

South Carolina Assumption Agreement of Loan Payments

Category:

State:

Multi-State

Control #:

US-00424

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Assumption Agreement Of Loan Payments?

If you need to finalize, obtain, or print sanctioned document templates, utilize US Legal Forms, the most significant compilation of legal forms available online.

Take advantage of the site's straightforward and user-friendly search feature to locate the documents you require.

Numerous templates for commercial and personal purposes are categorized by type and state, or keywords. Use US Legal Forms to locate the South Carolina Assumption Agreement of Loan Payments with just a few clicks.

Step 5. Process the transaction. You can use your credit card or PayPal account to complete the purchase.

Step 6. Choose the format of your legal form and download it to your device. Step 7. Complete, modify, and print or sign the South Carolina Assumption Agreement of Loan Payments. Each legal document template you obtain is yours permanently. You have access to every form you downloaded in your account. Click on the My documents section and select a form to print or download again. Compete and acquire, and print the South Carolina Assumption Agreement of Loan Payments with US Legal Forms. There are millions of professional and state-specific forms you can utilize for your business or personal needs.

- If you are already a US Legal Forms customer, Log In to your account and click the Download button to acquire the South Carolina Assumption Agreement of Loan Payments.

- You can also access forms you previously downloaded in the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Utilize the Review option to examine the form's content. Always remember to read the details.

- Step 3. If you are not satisfied with the form, use the Search box at the top of the screen to find alternative types of your legal form design.

- Step 4. Once you have found the form you desire, select the Acquire now button. Choose the pricing plan you prefer and enter your information to register for an account.

Form popularity

FAQ

A loan assumption agreement template is a pre-formatted document that helps you outline the terms of a South Carolina Assumption Agreement of Loan Payments. This template typically includes sections for borrower information, loan details, and conditions of the assumption. Using a template simplifies the process, making it easier for you to ensure that all necessary elements are included. Platforms like uslegalforms offer user-friendly templates that can save you time and ensure all legal requirements are met.

Documenting a loan assumption in South Carolina involves creating a South Carolina Assumption Agreement of Loan Payments. This legal document outlines the terms of the assumption, including the responsibilities of both the original borrower and the new borrower. It's important to have the agreement signed by all parties and possibly notarized to ensure its validity. Utilizing a reliable platform like uslegalforms can provide you with templates and guidance to create a comprehensive and legally sound agreement.

To facilitate a South Carolina Assumption Agreement of Loan Payments, you typically need several key documents. These include the original loan agreement, a formal request for assumption, and any necessary disclosures from the lender. Additionally, you may need proof of income and creditworthiness to ensure you meet the lender's requirements. Gathering these documents helps streamline the assumption process and ensures compliance with state regulations.

Loan assumption, however, allows a buyer to take over the current owner's mortgage while the loan's terms ? including the repayment period and interest rate ? remain the same. Ultimately, it can help people get into a home at a lower interest rate even as the housing market around them becomes more expensive.

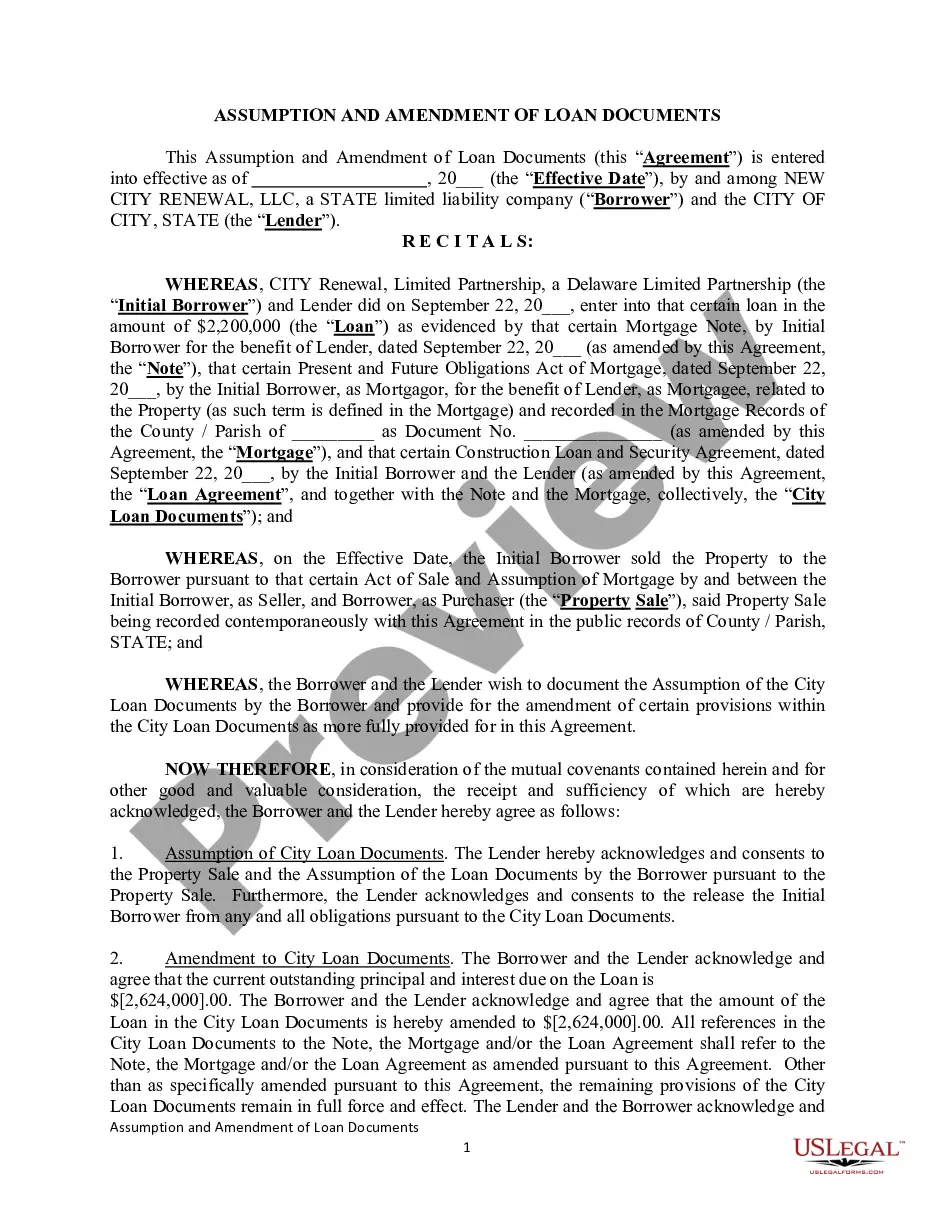

Assumption of Obligations. New Borrower covenants, promises, and agrees that New Borrower, jointly and severally if more than one, will unconditionally assume and be bound by all terms, provisions, and covenants of the Assumed Loan Documents as if New Borrower had been the original maker of the Assumed Loan Documents.

SECTION 37-23-70. Prohibited acts; complaints; penalties; statute of limitations; enforcement; costs. (A) A lender may not engage knowingly or intentionally in the unfair act or practice of "flipping" a consumer home loan.

An assumable mortgage is a home loan that can be transferred from the original borrower to the next homeowner. The interest rate and payment period stay the same. For example, if a 30-year mortgage is three years old, the person assuming the loan has 27 years to pay it off.

Most conventional mortgages are not assumable, but many government-backed loans (FHA, VA, USDA) are. The lender must approve you assuming the mortgage, and at the closing, you must compensate the old borrower for the amount they've paid off.

When a buyer buys property and assumes a mortgage, the buyer becomes primarily liable for the debt and the seller becomes secondarily liable for the debt. "Assume" means the buyer takes on liability, and the seller is no longer primarily liable. "Subject to" means the seller is not released from responsibility.

Updated March 7, 2022. In real estate transactions, an assumption agreement allows a third party to ?assume? or take over the loan of the property's seller. Mortgages may be assumed when the house is sold, a divorcing spouse is awarded the property in a settlement or when someone inherits property.