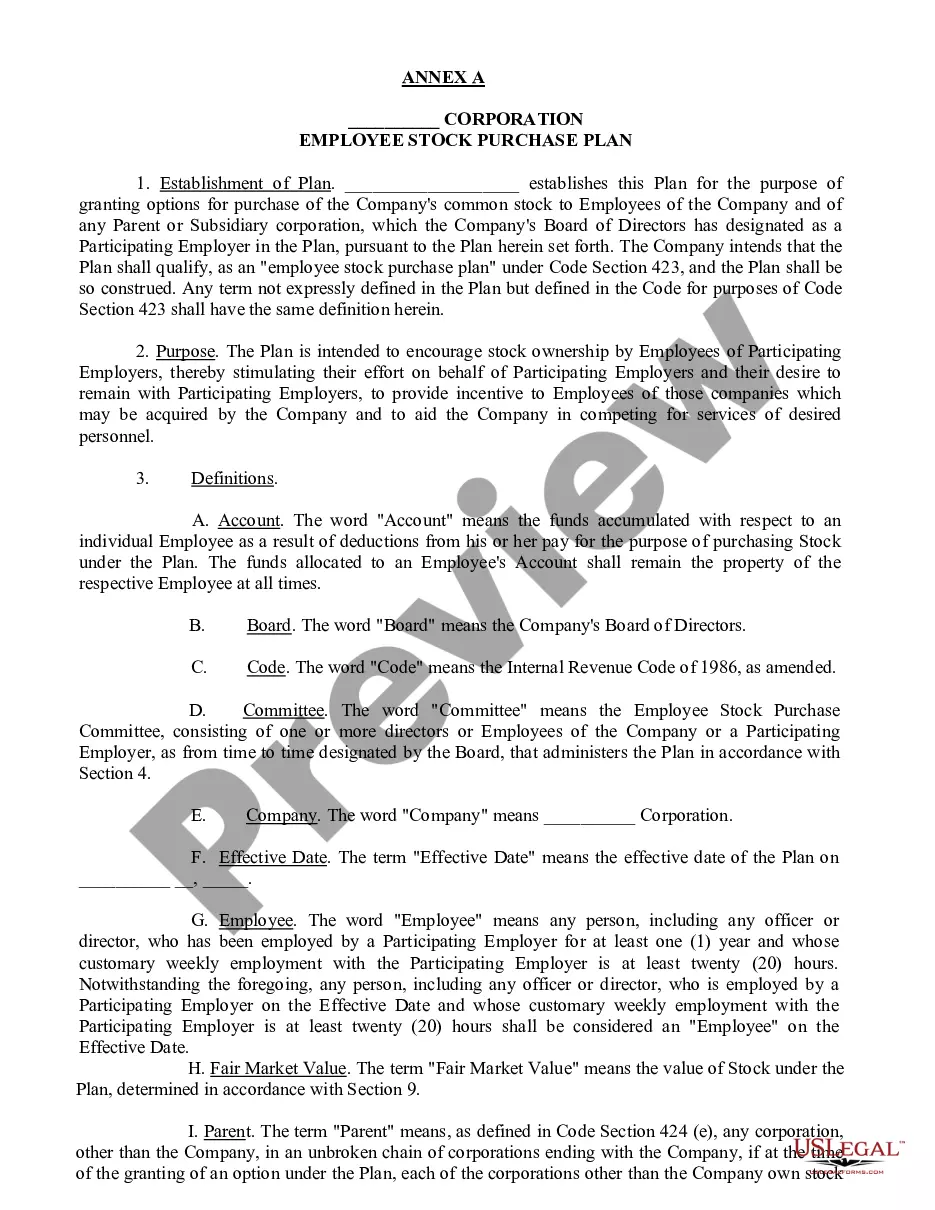

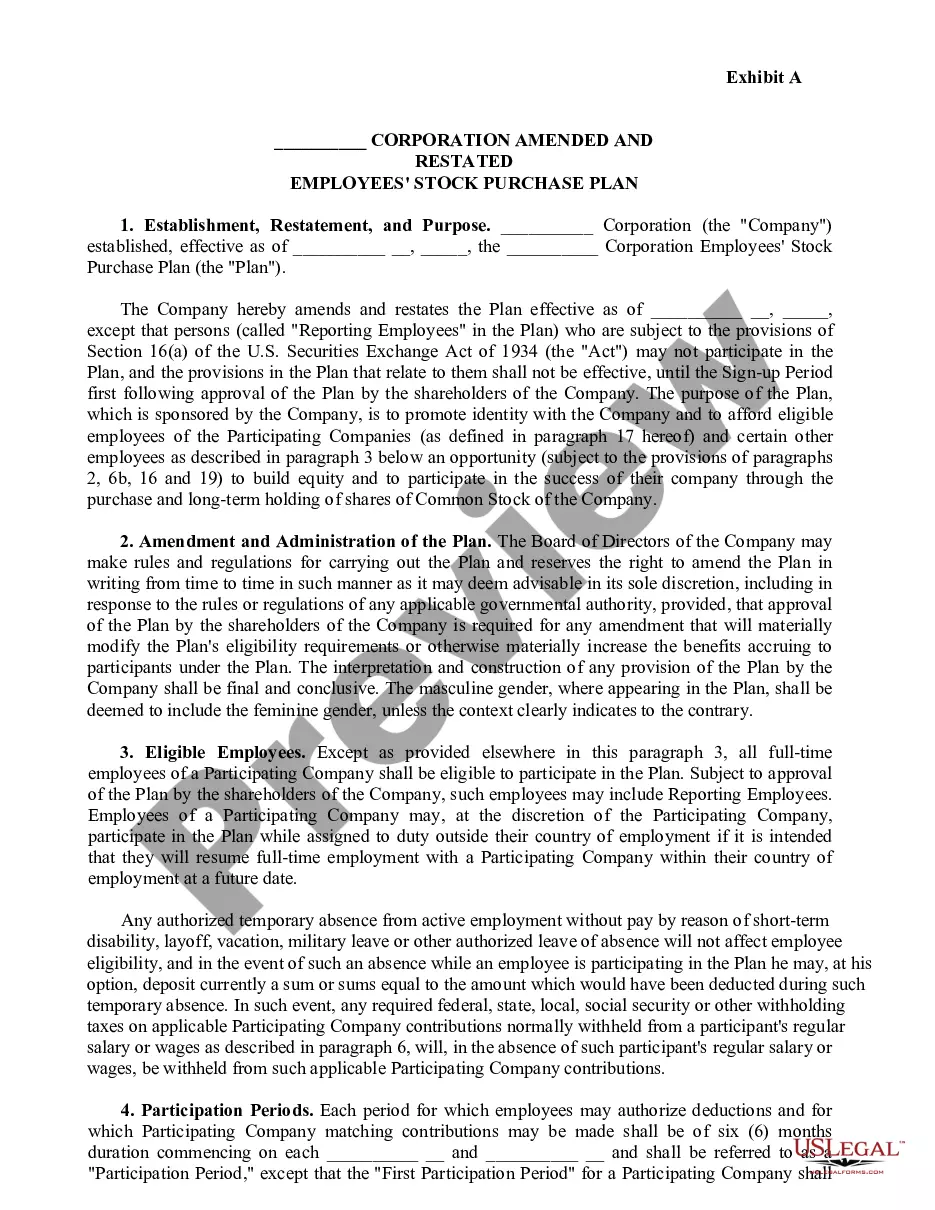

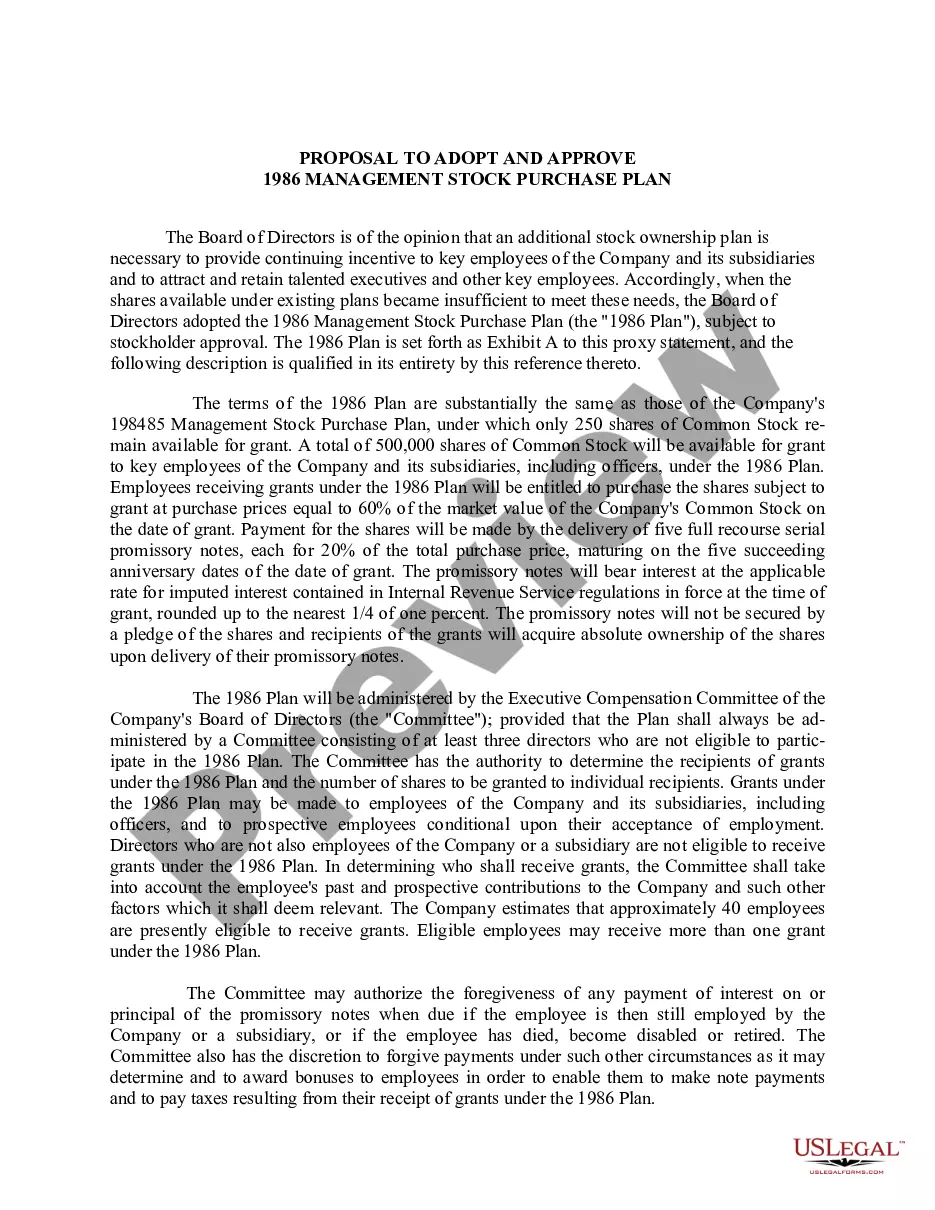

19-223D 19-223D . . . Management Stock Purchase Plan under which Executive Compensation Committee can grant options to key employees (including officers) at prices equal to 60% of market value. Payment is made by delivery of five full recourse interest-bearing serial promissory notes, each for 20% of total purchase price, which mature on five succeeding anniversary dates of date of grant. Committee may forgive any payment of interest or principal on promissory notes if employee is then still employed by Company, has died, or become disabled or retired

Oregon Management Stock Purchase Plan

Category:

State:

Multi-State

Control #:

US-CC-19-223D

Format:

Word;

Rich Text

Instant download

Description

Free preview

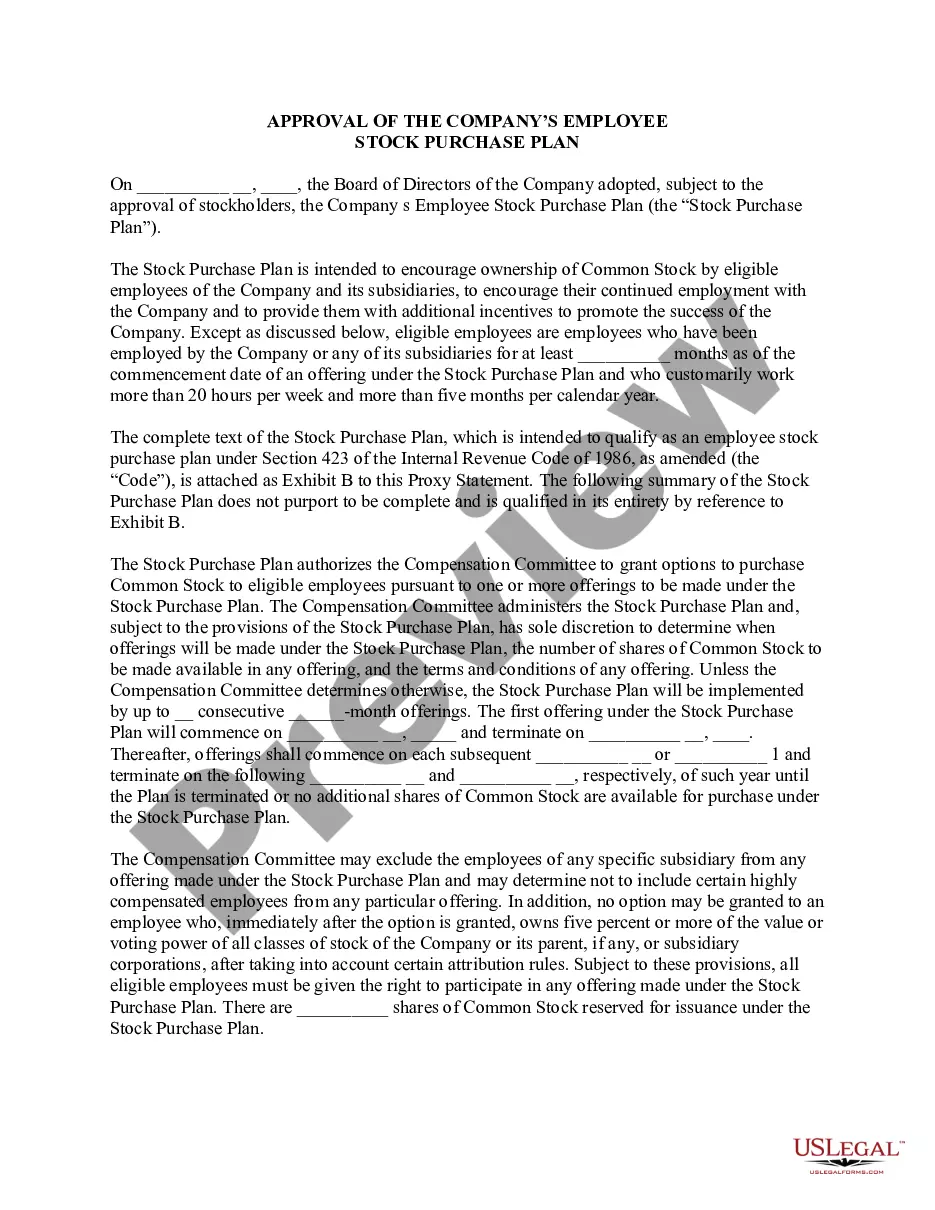

How to fill out Management Stock Purchase Plan?

Choosing the best lawful file design might be a have difficulties. Of course, there are a lot of web templates available on the Internet, but how would you find the lawful form you require? Use the US Legal Forms website. The service provides thousands of web templates, including the Oregon Management Stock Purchase Plan, that can be used for enterprise and private requirements. Every one of the varieties are checked out by pros and fulfill federal and state needs.

In case you are currently listed, log in in your account and click on the Download key to obtain the Oregon Management Stock Purchase Plan. Make use of account to search with the lawful varieties you have bought in the past. Proceed to the My Forms tab of the account and obtain one more version of the file you require.

In case you are a fresh user of US Legal Forms, listed here are basic instructions so that you can follow:

- Initial, make certain you have selected the appropriate form for your metropolis/region. You are able to check out the shape utilizing the Review key and read the shape outline to guarantee this is basically the right one for you.

- If the form is not going to fulfill your requirements, use the Seach industry to obtain the appropriate form.

- When you are certain that the shape would work, click on the Buy now key to obtain the form.

- Choose the pricing strategy you would like and enter in the required details. Design your account and pay for the transaction utilizing your PayPal account or credit card.

- Opt for the submit file format and obtain the lawful file design in your product.

- Comprehensive, revise and print and sign the obtained Oregon Management Stock Purchase Plan.

US Legal Forms will be the greatest catalogue of lawful varieties where you will find various file web templates. Use the service to obtain appropriately-created documents that follow status needs.

Form popularity

FAQ

Yes. By keeping all your retirement assets in your OSGP account, you benefit from low cost investments overseen by the Oregon Investment Council and, when you wish to take payments, you have the same flexible payout options that are available with an IRA.

ESPP eligibility and limits Most plans allow employees to elect a payroll deduction between 1% and 15%.

How does a withdrawal work in an ESPP? With most employee stock purchase plans, you can withdraw from your plan at any time before the purchase. Withdrawals are made on Fidelity.com or through a representative. However, you should refer to your plan documents to determine your plan's rules governing withdrawals.

Disadvantages of Employee Stock Purchase Plans Ensuring the ESPP follows security and tax law guidelines can be challenging. A large amount of HR functions goes into administering the stock purchase plan. There are legal, tax, and administrative issues that go into setting up the plan.

Employees who elect to participate in a qualified ESPP are typically able to take advantage of some tax benefits, as the discount is not recognized as taxable income until the stock is sold. When you sell the stock, the discount you received when you bought it may be taxable as income.

In this situation, you sell your ESPP shares more than one year after purchasing them, but less than two years after the offering date. This is a disqualifying disposition because you sold the stock less than two years after the offering (grant) date.

The ESOP vs 401K Plan With a 401(k), the employer's contributions are tax-deferred, meaning that the money is taken out of each paycheck before taxes, and those wages are not taxed until withdrawal. Whereas with an ESOP, employees also do not pay taxes on the shares in their account until distribution.

An employee stock purchase plan (or ESPP) can be a very valuable benefit. In general, if your employer offers an ESPP, we think you should participate at the level you can comfortably afford and then sell the shares as soon as you can.