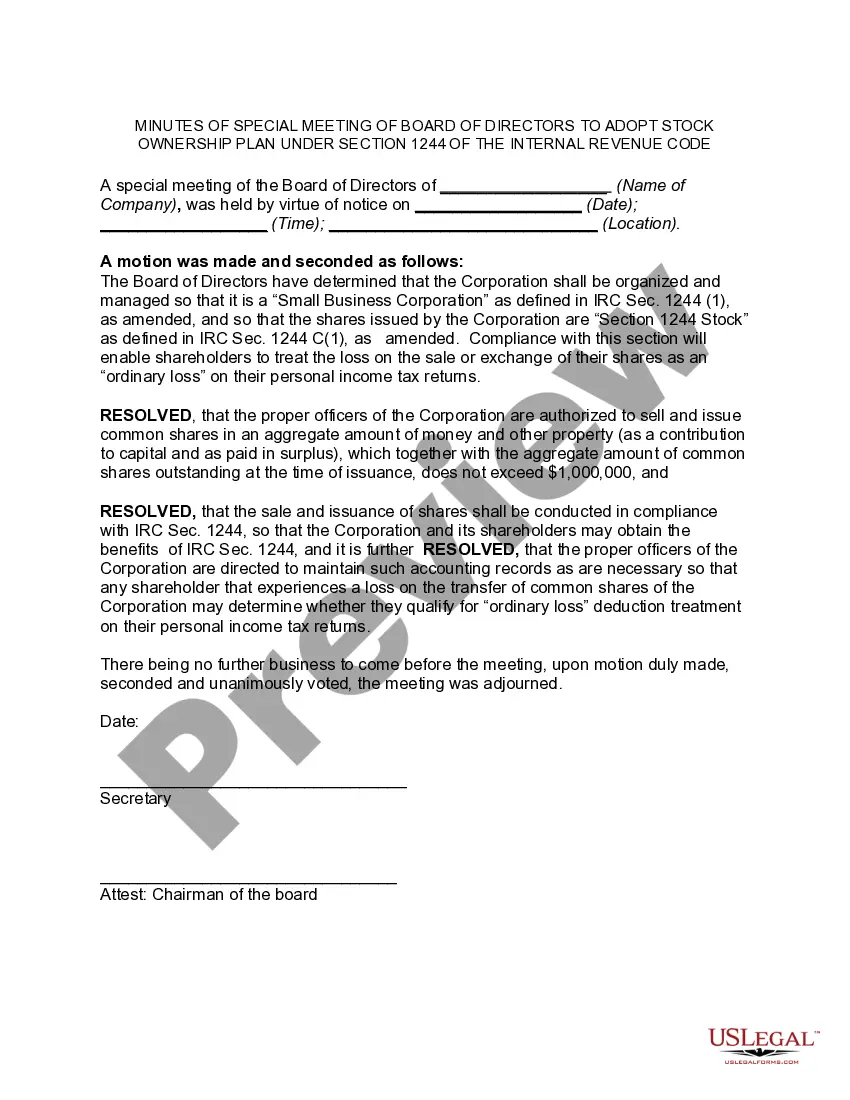

Oregon Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code

Description

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

How to fill out Minutes Of Special Meeting Of The Board Of Directors Of (Name Of Corporation) To Adopt Stock Ownership Plan Under Section 1244 Of The Internal Revenue Code?

Are you currently in a location where you need documentation for either business or personal purposes almost daily? There are numerous legal document templates available online, but locating reliable ones can be challenging. US Legal Forms provides thousands of form templates, such as the Oregon Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code, that are designed to comply with both state and federal regulations.

If you are already acquainted with the US Legal Forms website and possess an account, simply Log In. After that, you can download the Oregon Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code template.

If you do not have an account and wish to start using US Legal Forms, follow these steps.

You can view all the document templates you have purchased in the My documents menu. You can obtain an additional copy of the Oregon Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code at any time if needed. Just click the desired document to download or print the template.

Utilize US Legal Forms, the most extensive collection of legal forms, to save time and avoid mistakes. The service offers professionally crafted legal document templates that can be used for a variety of purposes. Create your account on US Legal Forms and start simplifying your life.

- Find the document you require and verify it is for the correct city/state.

- Utilize the Review option to examine the document.

- Read the description to ensure you have chosen the correct document.

- If the document is not what you are looking for, use the Search field to locate the document that meets your needs and requirements.

- When you find the correct document, click on Buy now.

- Select the pricing plan you desire, fill out the necessary information to create your account, and place an order using your PayPal or credit card.

- Choose a suitable paper format and download your copy.

Form popularity

FAQ

Qualifying for Section 1244 StockThe stock must be issued by U.S. corporations and can be either a common or preferred stock.The corporation's aggregate capital must not have exceeded $1 million when the stock was issued and the corporation cannot derive more than 50% of its income from passive investments.More items...

Section 1244 stock refers to the tax treatment of qualified restricted shares. Section 1244 stock allows firms to report certain capital losses as ordinary losses for tax purposes. This lets new or smaller companies take advantage of lower effective tax rates and increased deductions.

1244 losses are allowed for NOL purposes without being limited by nonbusiness income. An annual limitation is imposed on the amount of Sec. 1244 ordinary loss that is deductible. The maximum deductible loss is $50,000 per year ($100,000 if a joint return is filed) (Sec.

The determination of whether stock qualifies as Section 1244 stock is made at the time of issuance. Section 1244 stock is common or preferred stock issued for money or other property by a domestic small business corporation (which can be a C or S corporation) that meets a gross receipts test.

Under the current 2020 tax tables, a long-term capital gain that results from the sale of this Section 1244 stock will be taxed at the regular preferential rate of 15% for most individuals or 20% for high-income individuals with taxable income over $441,450. The 3.8% Net Investment Income Tax (NIIT) may also be due.

Section 1244 of the Internal Revenue Code allows eligible shareholders of domestic small business corporations to deduct a loss on the disposal of such stock as an ordinary loss rather than a capital loss. Eligible investors include individuals, partnerships and LLCs taxed as partnerships.

Section 1244 stock is a stock transaction pursuant to the Internal Revenue Code provision that allows shareholders of an eligible small business corporation to treat up to $50,000 of losses (or, in the case of a husband and wife filing a joint return, $100,000) from the sale of stock as ordinary losses instead of

All C and S corporations must have a board of directors. The number of directors depends on the business' size and is usually noted in the bylaws and articles of incorporation. No matter what state the business is formed in, all corporations must have a board of directors that is elected by shareholders.

Under Section 1244, an individual stockholder of a corporation can claim an ordinary (rather than capital) loss of up to $50,000 per year (or $100,000 for on a joint return) from the sale or worthlessness of Section 1244 stock. For most stockholders, an ordinary loss is much more beneficial than a capital loss.

Section 1244 stock is a stock transaction pursuant to the Internal Revenue Code provision that allows shareholders of an eligible small business corporation to treat up to $50,000 of losses (or, in the case of a husband and wife filing a joint return, $100,000) from the sale of stock as ordinary losses instead of