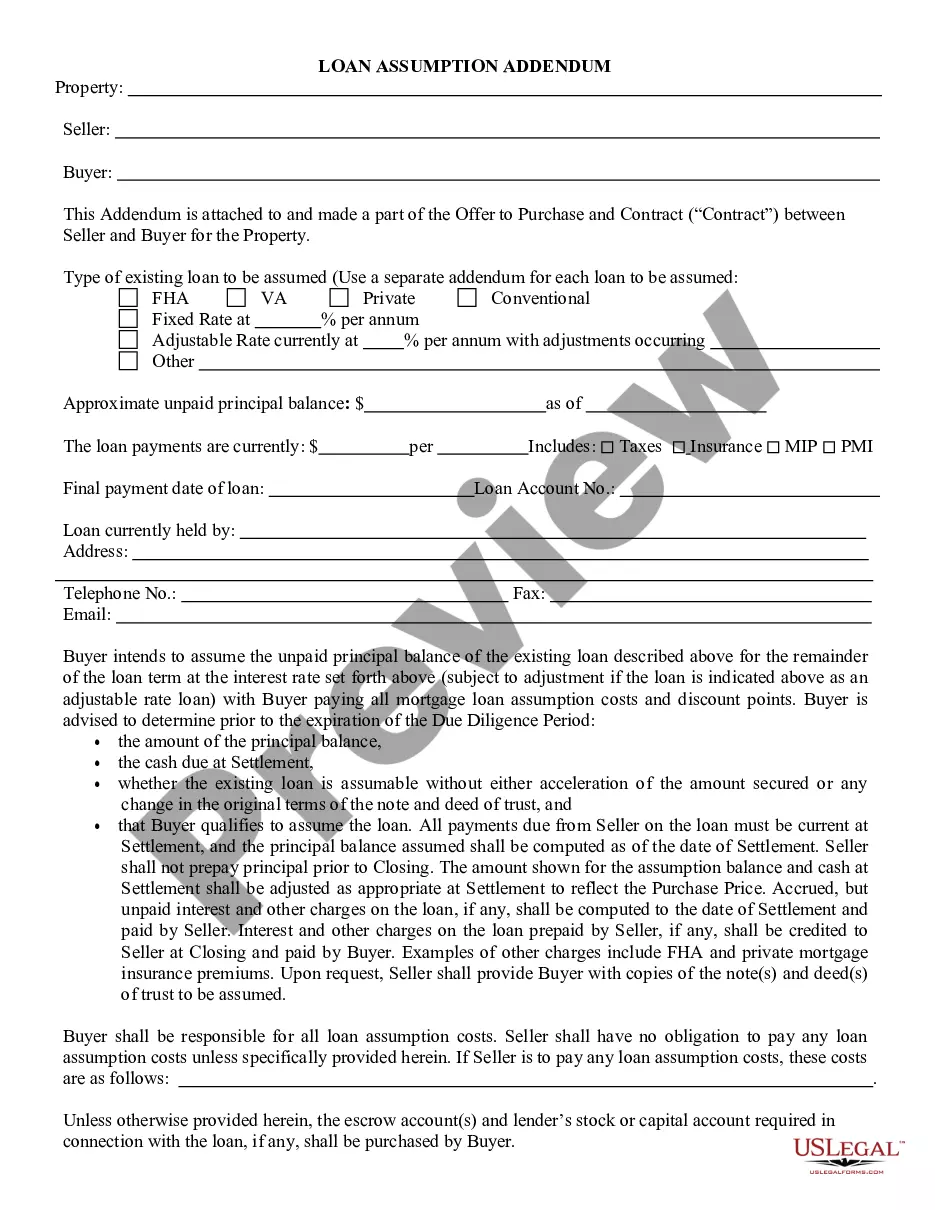

This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

Ohio Loan Assumption Agreement

Category:

State:

Multi-State

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Assumption Agreement?

It is feasible to spend hours online searching for the proper legal document template that meets the national and state regulations you require.

US Legal Forms provides a vast array of legal documents that are assessed by experts.

You can download or print the Ohio Loan Assumption Agreement from this service.

If available, utilize the Preview button to view the document template as well. If you wish to obtain an additional version of the form, use the Search field to find the template that meets your specifications and requirements. Once you have found the template you need, click Buy now to proceed. Choose the pricing plan you prefer, enter your details, and create a free account with US Legal Forms. Complete the transaction. You can use your credit card or PayPal account to pay for the legal document. Select the format of the document and download it to your device. Make modifications to your document if necessary. You can complete, alter, endorse, and print the Ohio Loan Assumption Agreement. Obtain and print numerous document templates using the US Legal Forms website, which offers the largest collection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you possess a US Legal Forms account, you may sign in and select the Obtain button.

- Then, you can complete, modify, print, or endorse the Ohio Loan Assumption Agreement.

- Every legal document template you purchase is yours forever.

- To acquire an additional copy of any purchased form, navigate to the My documents section and click the relevant button.

- If this is your first time using the US Legal Forms website, follow the simple instructions below.

- First, ensure you have chosen the correct document template for the state/region of your choice.

- Review the form description to confirm you have selected the right template.

Form popularity

FAQ

Assuming a mortgage may not be as common, but they are still a viable option for Canadian buyers and sellers. If you've done your research, asked all the important questions, and the benefits outweigh the risks, it could be the perfect fit for you!

How does the loan assumption process work? Getting approved to assume a loan is similar to getting approved for a new mortgage. You will need to complete an application, provide documents, and meet the lender's credit, income, and financial requirements to get the loan assumption approved.

To apply for an assumable Freddie Mac Small Balance Loan, you will need to contact a lender that offers the program. You can find a list of approved lenders here. The application process is streamlined and the loan is assumable with lender approval and a 1% fee.

However, loans that are insured by the Federal Housing Administration (FHA) or backed by the Department of Veterans Affairs (VA) or United States Department of Agriculture (USDA) are assumable as long as specific requirements are satisfied.

An assumption clause is a provision in a mortgage contract that allows the seller of a home to pass responsibility for the existing mortgage to the buyer of the property. In other words, the new homeowner assumes the existing mortgage and?along with it?ownership of the property that secures the loan.

The sort of mortgages that can be assumed nowadays are generally government-backed or -insured loans. FHA loans. If you want to assume an FHA loan, you'll need to meet standard FHA loan requirements. ... USDA loans. To assume a USDA loan, you typically need a minimum credit score of 620. ... VA loans.

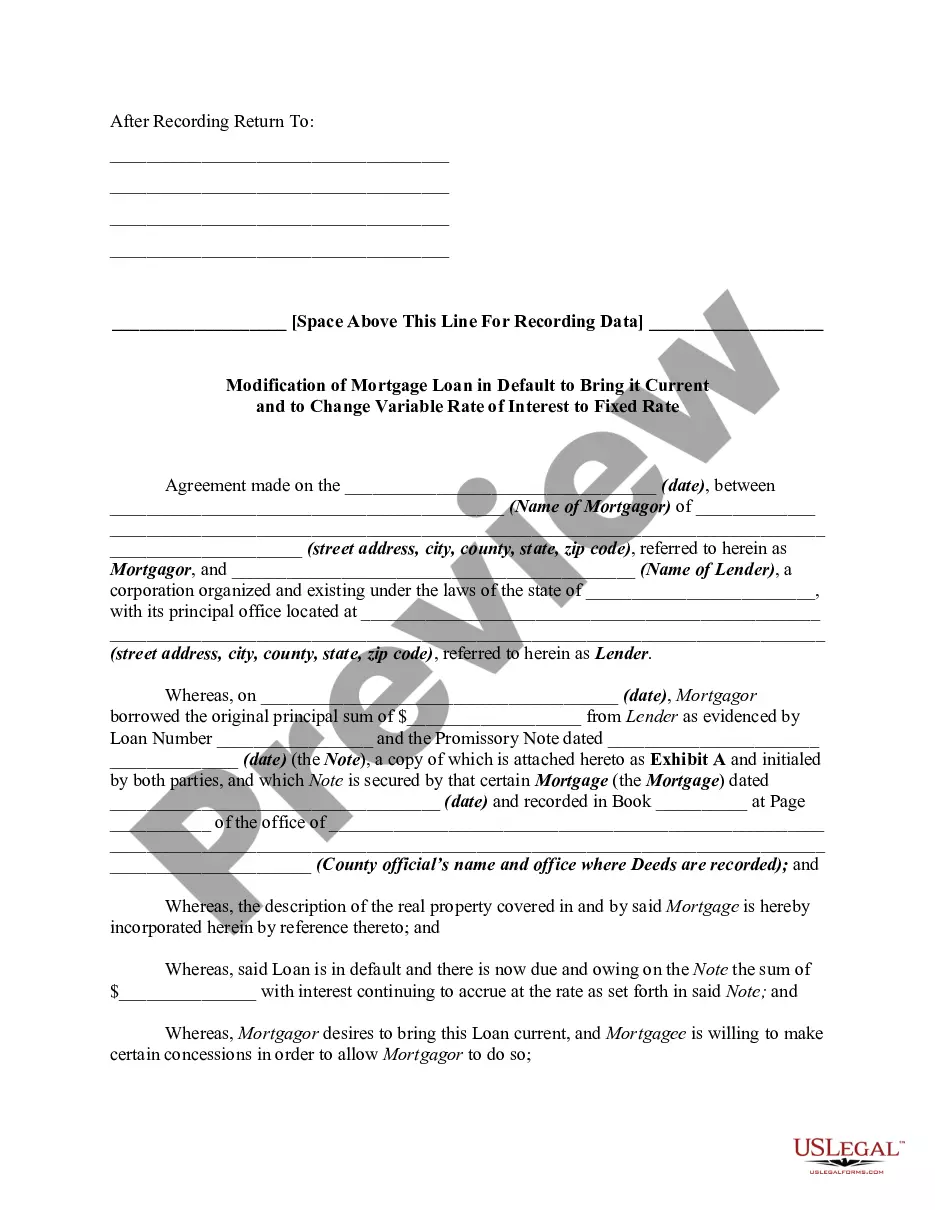

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

Keep in mind that the average loan assumption takes anywhere from 45-90 days to complete. The more issues there are with underwriting, the longer you'll have to wait to finalize your agreement.