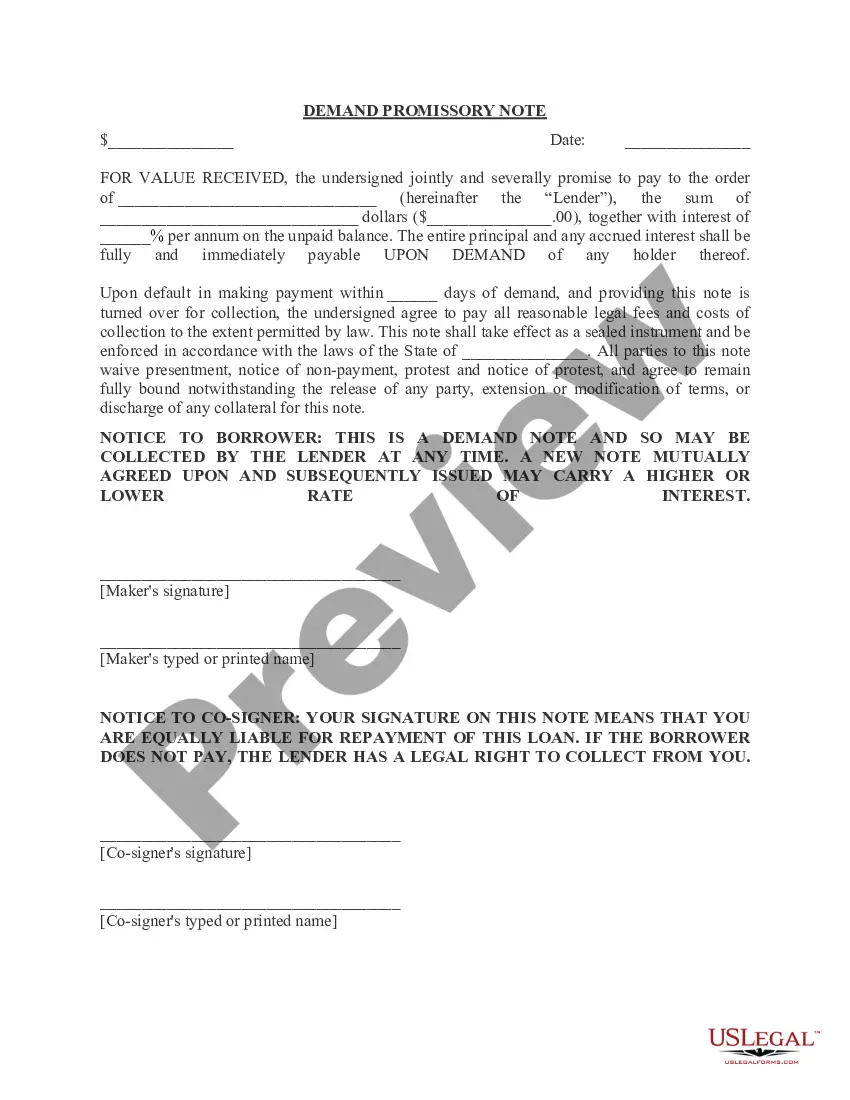

This form is a Promissory Note in connection with the sale of a vehicle where the Buyer is to pay a portion of the purchase price over time.

Ohio Promissory Note in Connection with Sale of Vehicle or Automobile

Instant download

Description

How to fill out Ohio Promissory Note In Connection With Sale Of Vehicle Or Automobile?

When it comes to submitting Ohio Promissory Note in Connection with Sale of Vehicle or Automobile, you almost certainly imagine an extensive process that involves choosing a appropriate form among a huge selection of very similar ones and then being forced to pay an attorney to fill it out to suit your needs. On the whole, that’s a slow and expensive option. Use US Legal Forms and pick out the state-specific template in a matter of clicks.

For those who have a subscription, just log in and click on Download button to get the Ohio Promissory Note in Connection with Sale of Vehicle or Automobile template.

In the event you don’t have an account yet but need one, stick to the step-by-step guideline below:

- Be sure the document you’re saving is valid in your state (or the state it’s needed in).

- Do this by reading the form’s description and also by clicking on the Preview option (if readily available) to view the form’s content.

- Click Buy Now.

- Pick the appropriate plan for your financial budget.

- Subscribe to an account and select how you would like to pay: by PayPal or by credit card.

- Save the file in .pdf or .docx format.

- Get the file on your device or in your My Forms folder.

Skilled lawyers work on creating our templates to ensure after downloading, you don't need to worry about editing and enhancing content outside of your individual info or your business’s info. Sign up for US Legal Forms and get your Ohio Promissory Note in Connection with Sale of Vehicle or Automobile sample now.

Form popularity

FAQ

The home (or business) serves as the collateral and an agreed upon down payment is the security for the note. As long as the buyer makes the agreed payments, they continue to be owners of the home. Should they default, the seller can take back, or foreclose on, the property.

An Ohio bill of sale is a document that acts as proof of ownership when an item is sold. A bill of sale in Ohio does not need to be notarized.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. In some cases, the note is endorsed in blank which makes it a bearer instrument under Article 3 of the Uniform Commercial Code. So, any party that possesses the note has the legal authority to enforce it.

200b200bThe promissory note should contain: The car's VIN number, model, make and year of manufacture. The statement that the borrower promises to pay the lender a specific amount, how much each payment will be, the annual interest rate and when the loan will be completely repaid.

Debt Classification A promissory note is a type of written contract a lender uses for secured debts where the lender has collateral to seize in the event of default. It is more likely your car loan is a promissory note if you have a schedule of payments and a fixed interest rate spelled out on your loan document.

Promissory notes are not attached to one person or business. If you have a customer's note, you can legally sell it or you can exchange it with someone else. That person is then entitled to collect on the debt. Whoever holds the note but it's only valid if certain conditions are met.

Secured and unsecured loansPromissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

A promissory note is usually held by the party owed money; once the debt has been fully discharged, it must be canceled by the payee and returned to the issuer.