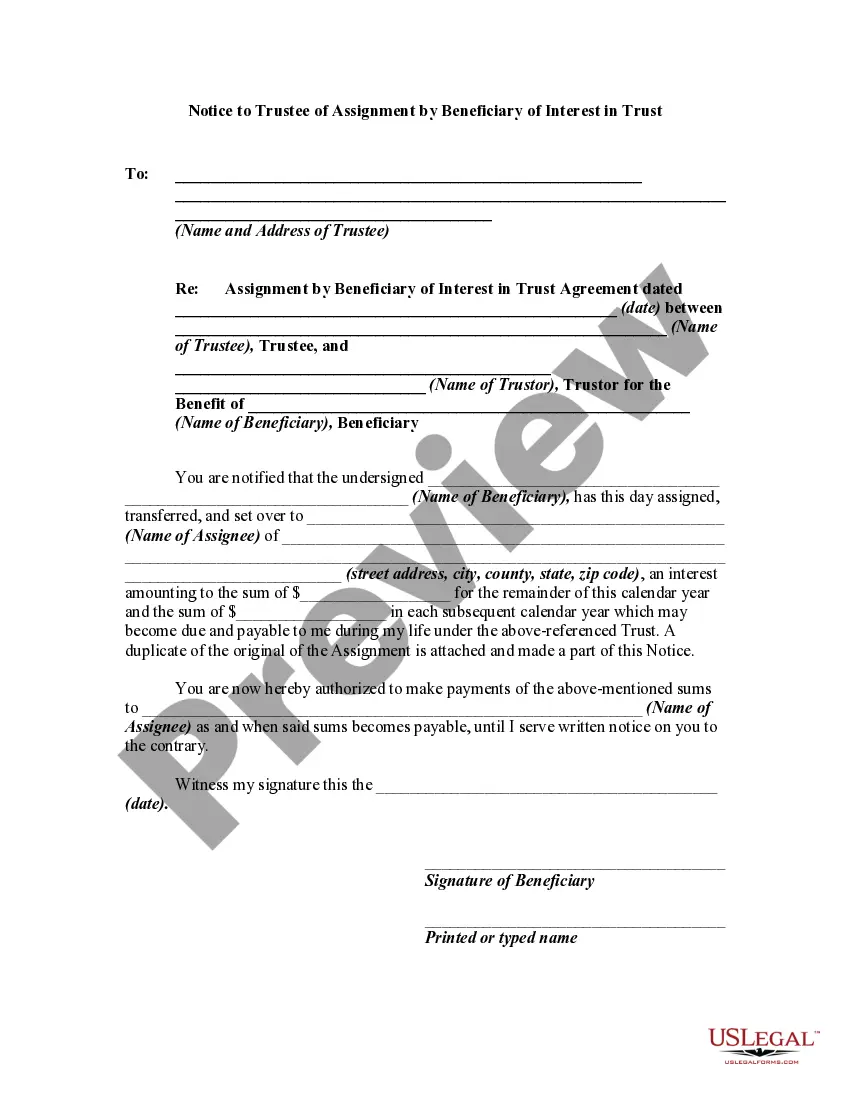

A discretionary trust is a trust where the beneficiaries and/or their entitlements to the trust fund are not fixed, but are determined by the criteria set out in the trust instrument by trustor. Discretionary trusts can be discretionary in two respects. First, the trustees usually have the power to determine which beneficiaries (from within the class) will receive payments from the trust. Second, trustees can select the amount of trust property that the beneficiary receives. Although most discretionary trusts allow both types of discretion, either can be allowed on its own. It is permissible in most legal systems for a trust to have a fixed number of beneficiaries and for the trustees to have discretion as to how much each beneficiary receives.

New York Discretionary Distribution Trust for the Benefit of Trust or's Children with Discretionary Powers over Accumulation and Distribution of Principal and Income Separate Trust for each Beneficiary is a legal entity established in accordance with the laws of New York. This type of trust provides a powerful and flexible tool for parents or granters who wish to ensure that their children are financially secure while still maintaining control over the distribution and management of wealth. The key feature of this trust is the discretionary power given to the trustees over the accumulation and distribution of both the trust's principal and income. This means that the trustees have the authority to decide when and how much to distribute to each beneficiary, taking into account their individual needs, circumstances, and best interests. The New York Discretionary Distribution Trust for the Benefit of Trust or's Children can be further categorized into different types based on the specific provisions and terms outlined in the trust document. Some common types include: 1. Education Trust: This type of trust focuses on funding the education expenses of the beneficiaries. Trustees have the discretion to allocate funds for tuition, books, accommodation, and other educational needs. 2. Maintenance Trust: A maintenance trust aims to provide regular income to the beneficiaries, supporting their everyday living expenses, healthcare, and general well-being. 3. Special Needs Trust: This trust is designed specifically for beneficiaries with disabilities or special needs. It allows the trustees to manage and disburse funds to meet the unique requirements of these individuals, without jeopardizing their eligibility for government assistance programs. 4. Trust with Spendthrift Provision: A trust with a spendthrift provision provides protection against the beneficiaries' creditors and ensures that the trust's assets are not subject to attachment or seizure in case of financial difficulties. Each of these specific types of New York Discretionary Distribution Trust for the Benefit of Trust or's Children aims to address different goals and priorities of the granter. By tailoring the trust to the specific needs of the beneficiaries and their circumstances, the granter can have peace of mind knowing that their children's financial well-being is being taken care of in the most appropriate manner. Overall, the New York Discretionary Distribution Trust for the Benefit of Trust or's Children with Discretionary Powers over Accumulation and Distribution of Principal and Income Separate Trust for each Beneficiary provides a robust and flexible framework for parents to protect and manage their children's wealth while allowing for adaptability to changing circumstances.