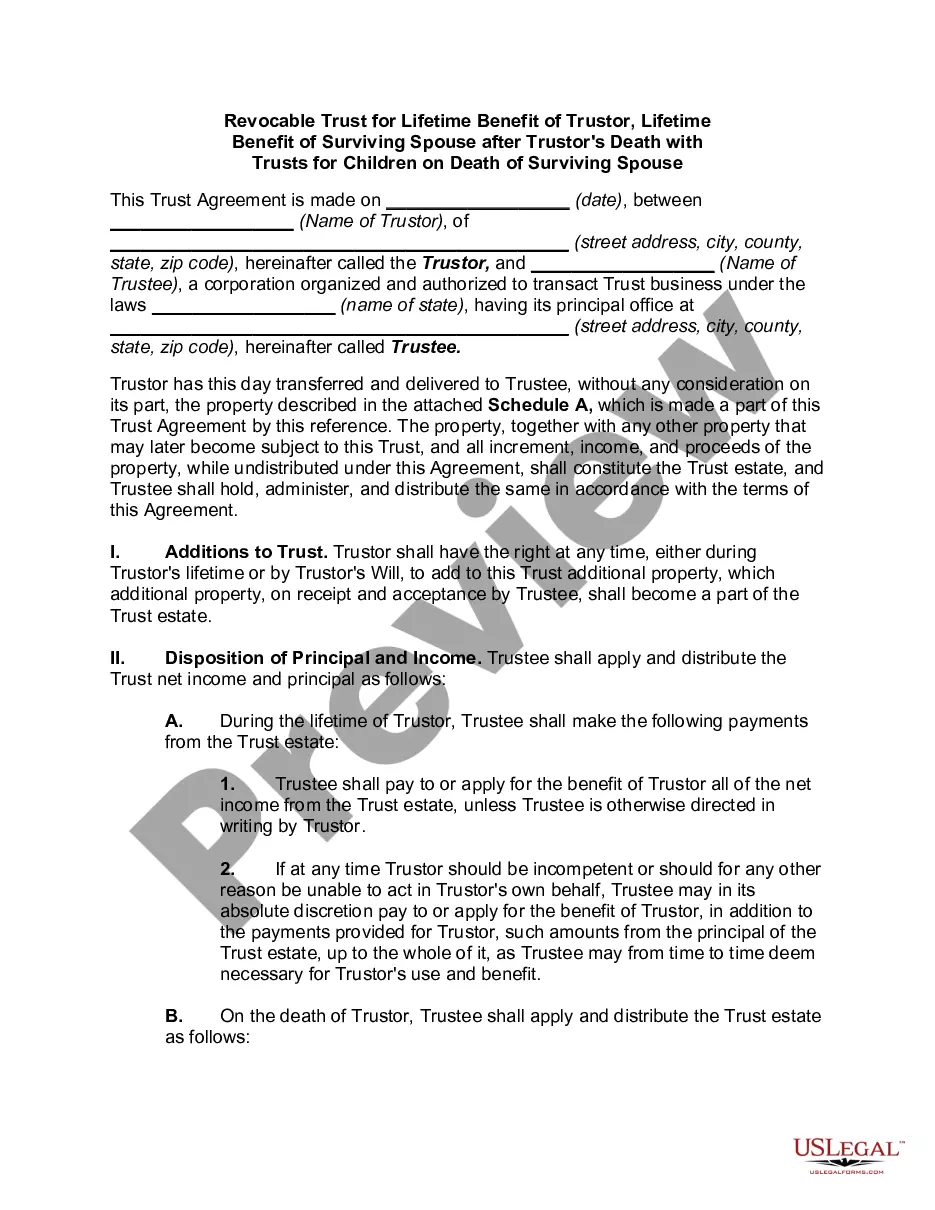

A trust is a fiduciary relationship in which one party holds legal title to another's property for the benefit of a party who holds equitable title to the property. An inter vivos trust is a trust that becomes effective during the lifetime of the person creating the trust (the settler or trustor).

A qualified terminable interest property trust, often referred to as a "QTIP" trust, allows a bequest to a spouse in trust that, after a proper election by the beneficiary spouse, qualifies for the unlimited marital deduction:

" if the beneficiary spouse is entitled to all of the income from the trust property,

" if the income is payable annually or at more frequent intervals, and

" if no person, including the beneficiary spouse, has the power to appoint any part of the qualifying property to any person other than the beneficiary spouse during the beneficiary spouse's lifetime.

In order that the property transferred to a surviving spouse by means of an inter vivos marital deduction trust qualify for the marital deduction, the property must be includible in the trustor's gross estate for federal estate tax purpose.